Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

Three Designs, One Survivor

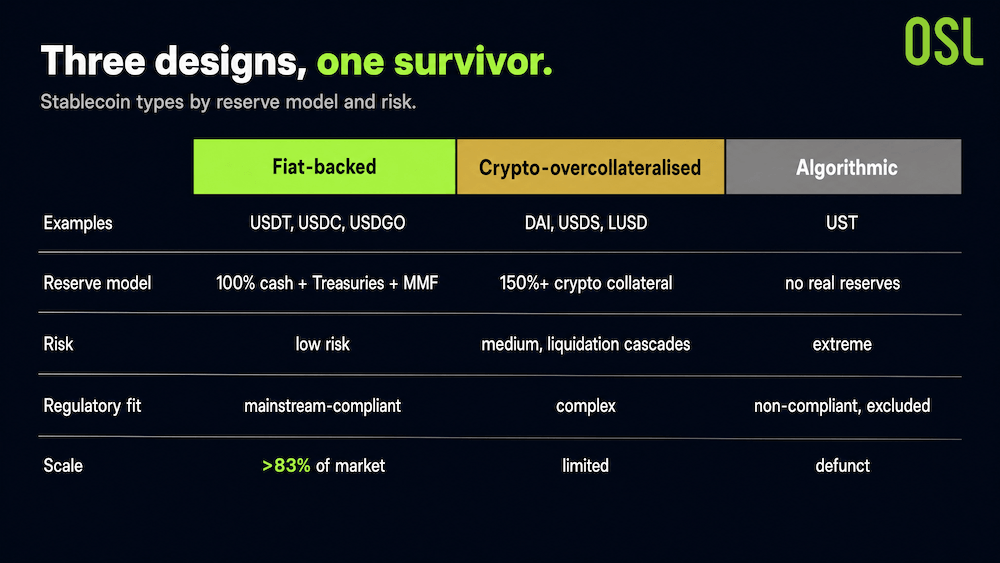

Not all stablecoins are built the same way. Academic and regulatory work (BIS, IMF) sorts them into three categories, and each carries a very different risk profile.

Chart 1: The Three Stablecoin Types

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

The fiat-backed model is simple to understand: every token is matched 1:1 by cash, short-term Treasuries, or money-market funds, a full 100% reserve. Reserves can be verified, redemption is clear, and the cost of plugging into traditional finance is low. That is why USDT and USDC alone hold over 83% of the market.

The crypto-overcollateralised model, led by MakerDAO's DAI (now USDS), backs each token with more than its value in crypto assets, typically 150% or more collateral. It is decentralised, but it carries liquidation-cascade risk and its growth is capped by overall crypto-market liquidity.

The algorithmic model is the one that broke.

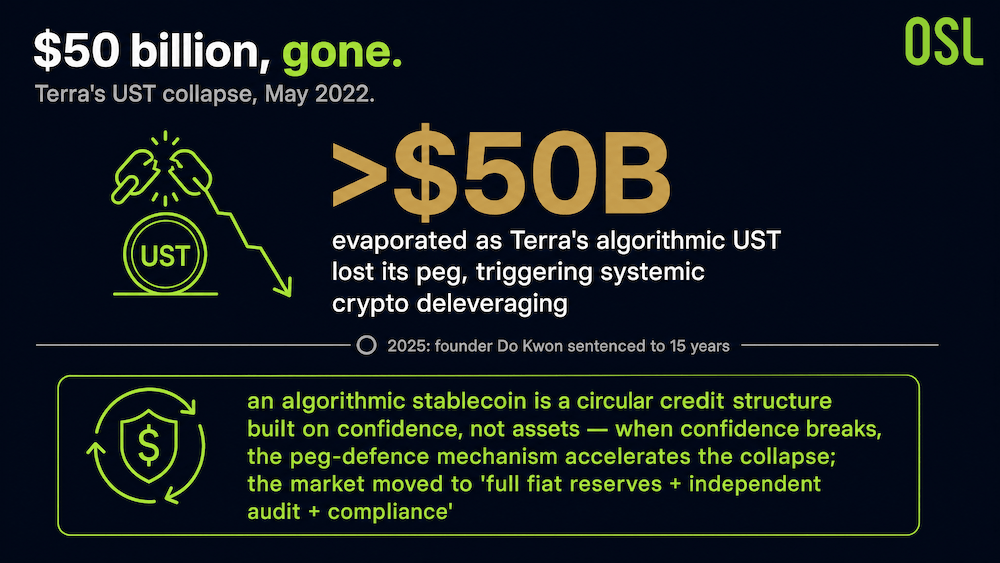

The $50 Billion Lesson

In May 2022, Terra's UST, an algorithmic stablecoin that maintained its peg through market incentives rather than real reserves, collapsed. More than $50 billion in value evaporated, and the event triggered a systemic deleveraging across crypto. In 2025, Terra founder Do Kwon was sentenced to 15 years, putting a legal full stop on the episode.

Chart 2: The Terra UST Collapse

The deeper lesson was structural. An algorithmic stablecoin is a circular credit structure built on confidence, not assets. When confidence breaks, the mechanism that is supposed to defend the peg accelerates its collapse instead. Markets absorbed that lesson and moved decisively toward "full fiat reserves + independent audit + compliance."

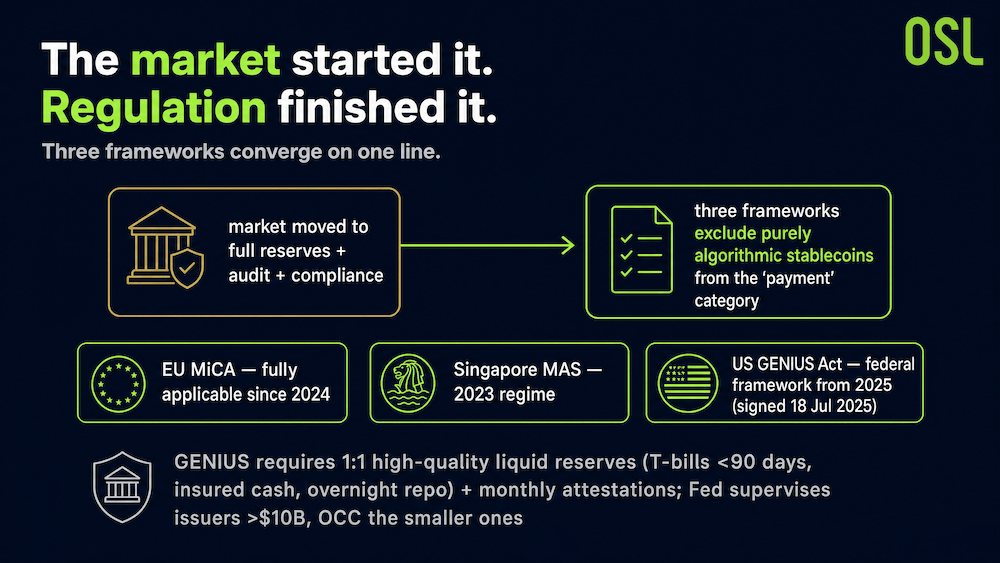

Regulators Made It Official

What the market started, regulation finished. By 2026, the three major frameworks had converged on the same line.

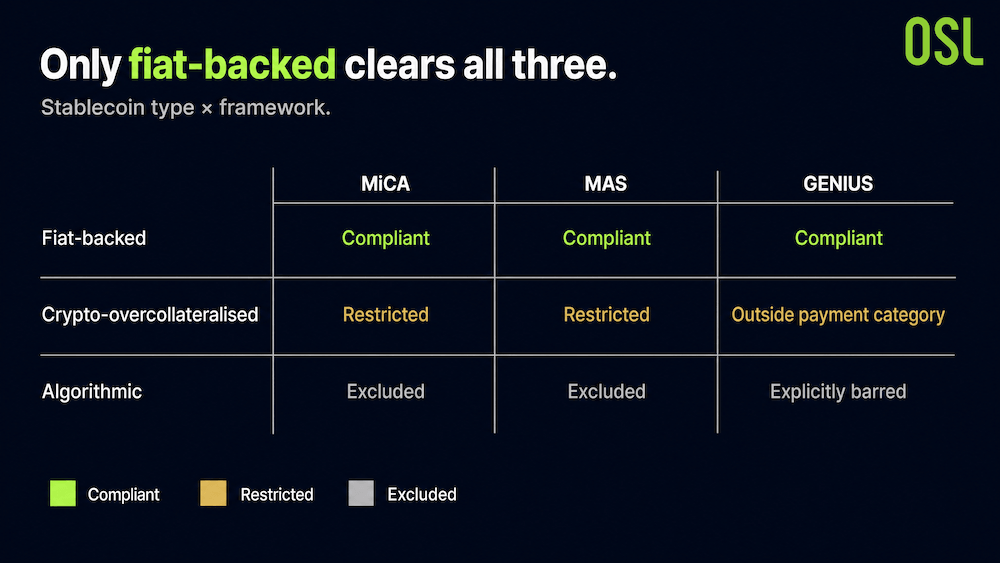

According to PaymentBrief's April 2026 comparison, the EU's MiCA (fully applicable since 2024), Singapore's MAS regime (2023), and the US GENIUS Act (federal framework from 2025) all explicitly exclude purely algorithmic stablecoins from the "payment stablecoin" category. They are not necessarily banned from existing, but they cannot be marketed or used as compliant payment instruments. Crypto-overcollateralised coins sit in between: restricted under MiCA and MAS, and outside the payment-stablecoin category under GENIUS. Only fiat-backed coins are treated as compliant across all three.

Chart 3: Convergence in Stablecoin Regulation

Source: PaymentBrief's April 2026 comparison, Regular.eu reported, OCC's rulemaking notice

The US framework is the sharpest example. As Regular.eu reported, the GENIUS Act, signed into law on 18 July 2025, explicitly bars algorithmic stablecoins like UST that rely on market mechanisms instead of real reserves. Only coins backed by verifiable, high-quality assets qualify. Per the OCC's rulemaking notice, GENIUS requires 1:1 reserves in high-quality liquid assets (Treasury bills under 90 days, insured cash, overnight repo) and monthly attestations, with the Federal Reserve supervising issuers above $10 billion and the OCC supervising smaller ones.

Chart 4: How Three Frameworks Treat Each Stablecoin Type

Source: PaymentBrief's April 2026 comparison, Regular.eu reported

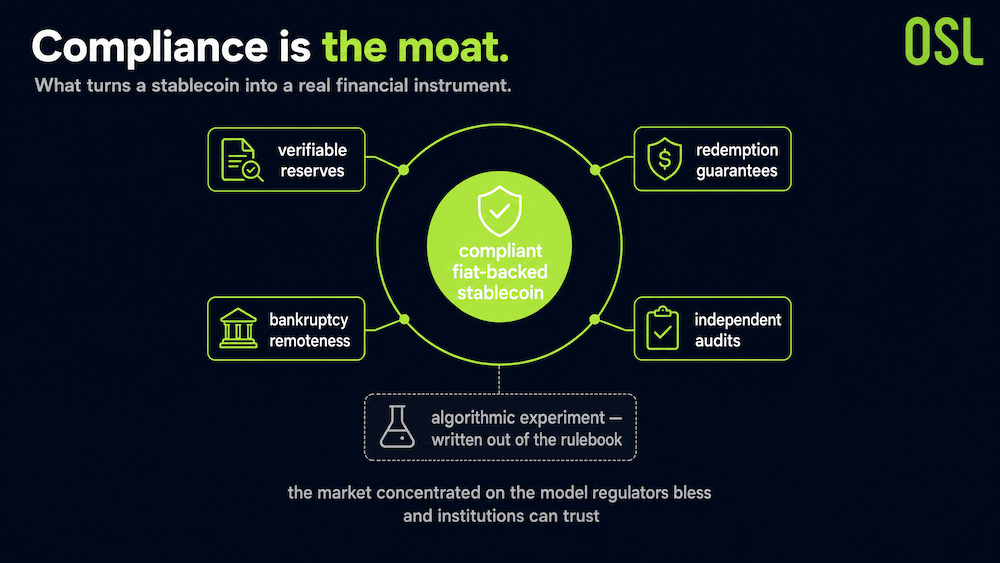

Compliance as a Moat, Not a Constraint

It is easy to read regulation as a burden. In stablecoins, it turned out to be the opposite. The compliance requirements, verifiable reserves, redemption guarantees, bankruptcy remoteness, independent audits, are exactly what let multinational corporates, treasury teams, and auditors treat a stablecoin as a real financial instrument rather than a crypto curiosity.

Chart 5: Compliance Is a Moat

That is the quiet story behind the duopoly. The market did not concentrate on USDT and USDC by chance. It concentrated on the model that regulators bless and institutions can trust. The algorithmic experiment did not just fail commercially; it was written out of the rulebook. In stablecoins, compliance is now the moat.

FAQ

Q1: What are the three types of stablecoins? A: Fiat-backed (e.g. USDT, USDC), crypto-overcollateralised (e.g. DAI), and algorithmic (e.g. UST). Only fiat-backed coins are treated as compliant payment instruments.

Q2: Are algorithmic stablecoins banned? A: Under GENIUS they are explicitly barred as payment stablecoins; MiCA and MAS exclude them from the payment category. They may still trade in some cases but cannot be marketed or used as compliant payment instruments.

Q3: Why did algorithmic stablecoins fail? A: They maintain their peg through market incentives rather than real reserves. When confidence breaks, as with Terra's UST in 2022, the mechanism accelerates the collapse. Around $50 billion evaporated in days.

Q4: Why do fiat-backed stablecoins dominate? A: Verifiable reserves, clear redemption, and regulatory fit make them trustworthy for institutions, which is why USDT and USDC together hold over 83% of the market.

References

Note: Industry analysis based on public sources and the cited report. Not investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

USDGO, a compliance-first enterprise stablecoin, hit $500M in four months. How its dual-licence design and payment stack solve cross-border B2B costs.

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Stablecoin transfers are fast and cheap on-chain, but the real costs hide at the on-ramp and off-ramp. Where stablecoin payments actually win, and don't.

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

Stablecoins come in three types, but only fiat-backed ones survived. How a $50B collapse and global regulation turned compliance into the real moat.

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

USDT and USDC control over 82% of the stablecoin market. Here's how the two coins differ and why new entrants keep failing to break the duopoly.

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Analyze SPCX stock's 50% surge and reversal. Learn why its low float, high FDV structure mirrors crypto tokens and what future unlocks mean for price.

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Recommended for you

More topics

More topics