USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

A Market Run by Two

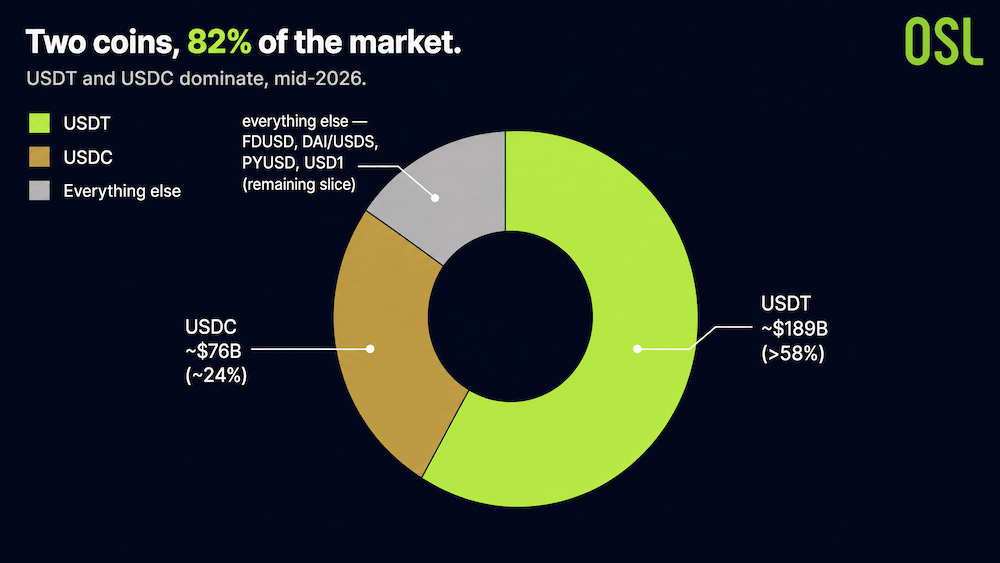

The stablecoin market looks crowded from a distance. Up close, it's a duopoly. According to DefiLlama and Gate's June 2026 data, USDT's supply sits around $189 billion (over 58% share) and USDC around $76 billion (about 24%). Together they control more than 82% of the market. Everything else, FDUSD, DAI/USDS, PYUSD, and Trump-affiliated USD1, splits the remaining slice.

Chart 1: Stablecoin Market Share

Source: DefiLlama, Gate's June 2026 data

That concentration is not an accident. It is the result of competition and risk-driven selection, and it has proven remarkably hard to break.

How They Actually Differ

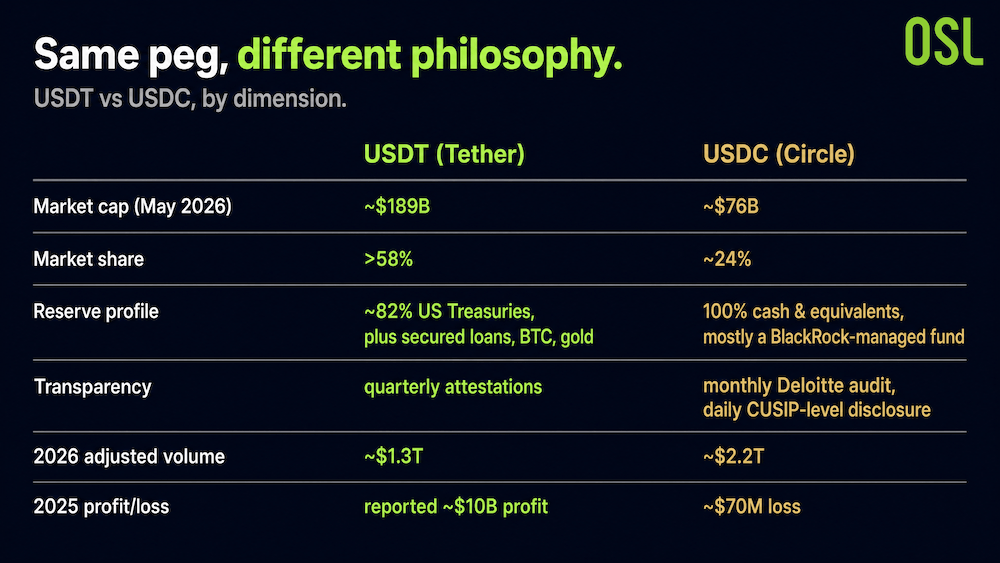

The two coins look identical on the surface, both pegged 1:1 to the dollar. Under the hood, they are built on different philosophies.

Chart 2: USDT vs USDC head to head

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

USDT is the deeper pool of liquidity. Its daily trading volume has long run more than 5x USDC's, and its US Treasury holdings reportedly exceed the national holdings of Germany, placing Tether among the world's top 20 holders of US government debt. Its reserves also include riskier assets, secured loans, Bitcoin, and gold, which help drive the profits Tether reported at around $10 billion for last year. On transparency, Tether publishes quarterly attestations rather than the more frequent disclosures Circle offers.

USDC takes the opposite bet. Its reserves are 100% cash and cash equivalents, with over 80% held in the Circle Reserve Fund (managed by BlackRock, custodied at BNY Mellon). Deloitte attests monthly and BlackRock publishes holdings daily. That transparency builds institutional trust, but it also caps yield, and Circle recorded a roughly $70 million loss in 2025.

Winning on Different Axes

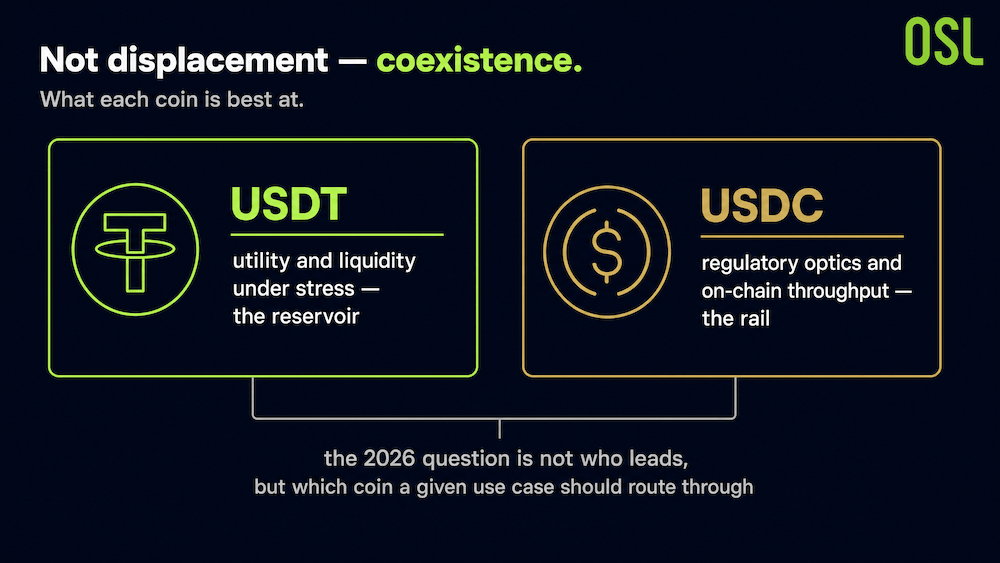

Here is the nuance most coverage misses: this is not a simple story of winner and loser.

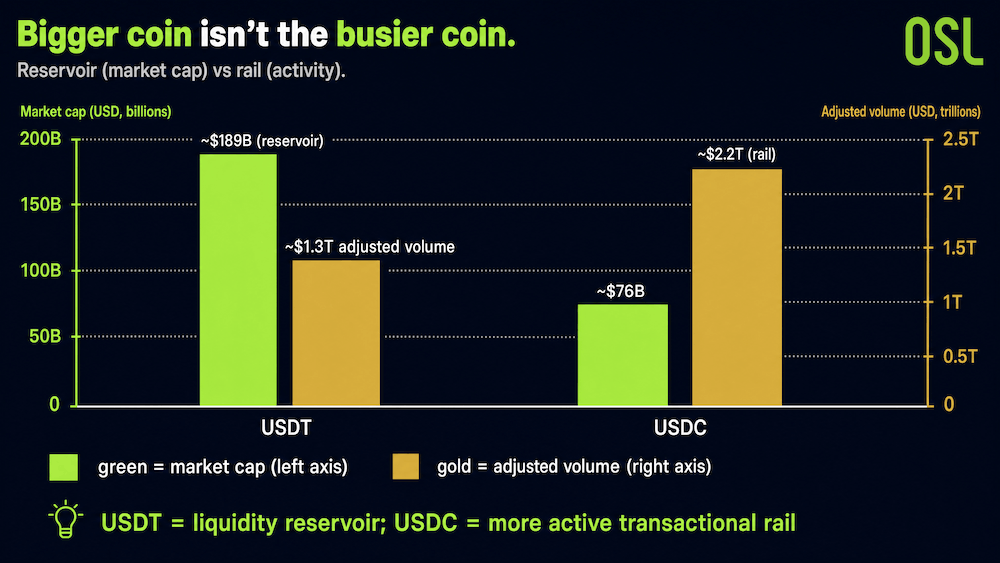

As The Chain Observer noted in April 2026, USDT is consolidating its lead as the market's preferred liquidity reservoir, now more than twice USDC's size. Yet USDC recorded about $2.2 trillion in adjusted transaction volume in 2026 against roughly $1.3 trillion for USDT, meaning Circle's coin is the more active transactional rail even as Tether holds the larger balance.

In other words, both are winning and losing at the same time, on different axes. Tether wins on utility and liquidity under stress. Circle wins on regulatory optics and on-chain throughput.

Chart 3: Reservoir vs rail

Source: The Chain Observer noted in April 2026

Why New Entrants Keep Bouncing Off

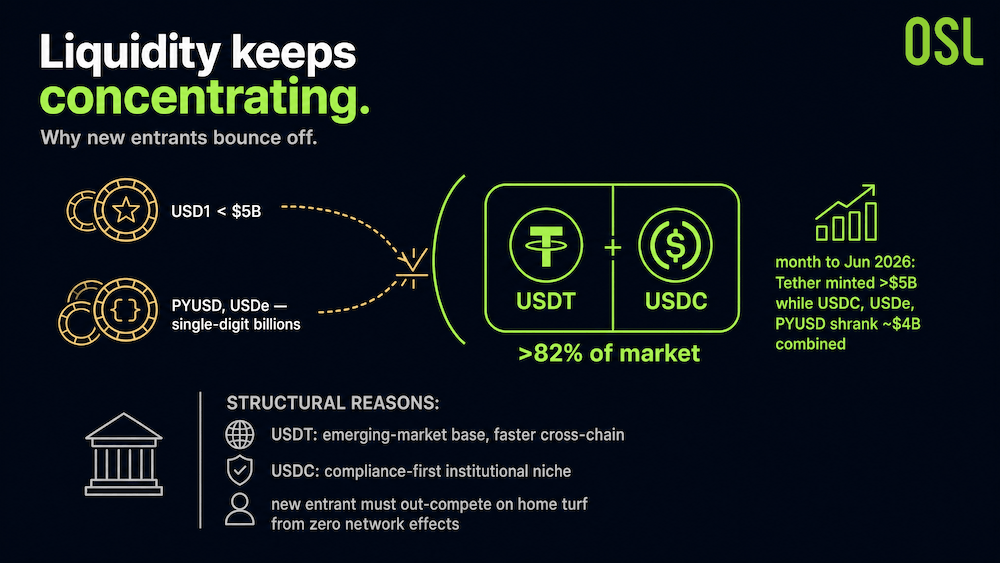

Plenty have tried. Trump-affiliated USD1 grew quickly but remains under $5 billion. PYUSD, USDe, and others hold single-digit-billion positions. None has meaningfully dented the duopoly.

The reasons are structural. USDT has a first-mover advantage in emerging-market user bases and scenario coverage, plus faster cross-chain deployment. USDC owns the compliance-first institutional niche. A new entrant has to out-compete one of them on its home turf, deeper liquidity or stronger compliance, while building network effects from zero. In the month to June 2026, Tether minted over $5 billion while USDC, USDe, and PYUSD collectively shrank by about $4 billion, a sign that liquidity is still concentrating toward the top, not dispersing.

Chart 4: New Stablecoin Entrants Struggle to Break the Duopoly

The likeliest outcome, as analysts across the board now frame it, is not displacement but long-term coexistence of the two. The interesting question for 2026 is no longer who leads, but what each coin is best at, and which one a given use case should route through.

Chart 5: The Long-Term Coexistence and Roles of USDT and USDC

FAQ

Q1: What share of the stablecoin market do USDT and USDC hold? A: Together more than 82% as of mid-2026, with USDT over 58% and USDC about 24%.

Q2: What is the main difference between USDT and USDC? A: USDT holds higher-yield, more varied reserves (including Treasuries, Bitcoin, and gold) and dominates liquidity; USDC holds 100% cash equivalents with monthly audits and prioritises compliance and transparency.

Q3: Is USDT or USDC more widely used for transactions? A: USDC recorded higher adjusted transaction volume in 2026 (~$2.2T vs ~$1.3T), while USDT holds the larger market cap.

Q4: Can a new stablecoin break the duopoly? A: Unlikely in the short term. New entrants like USD1 remain small, and liquidity continues concentrating toward USDT and USDC.

References

Note: Industry analysis based on public sources and the cited report. Not investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

USDGO, a compliance-first enterprise stablecoin, hit $500M in four months. How its dual-licence design and payment stack solve cross-border B2B costs.

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Stablecoin transfers are fast and cheap on-chain, but the real costs hide at the on-ramp and off-ramp. Where stablecoin payments actually win, and don't.

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

Stablecoins come in three types, but only fiat-backed ones survived. How a $50B collapse and global regulation turned compliance into the real moat.

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

USDT and USDC control over 82% of the stablecoin market. Here's how the two coins differ and why new entrants keep failing to break the duopoly.

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Analyze SPCX stock's 50% surge and reversal. Learn why its low float, high FDV structure mirrors crypto tokens and what future unlocks mean for price.

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Recommended for you

More topics

More topics