Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

A Growth Curve Worth Reading

Most stablecoin launches fade. USDGO did the opposite. Issued by Anchorage Digital Bank N.A. (the first federally chartered crypto bank in the US, OCC-regulated) and distributed by OSL across Asia-Pacific, it launched on 10 February 2026 with $50 million in initial liquidity.

What happened next is the interesting part.

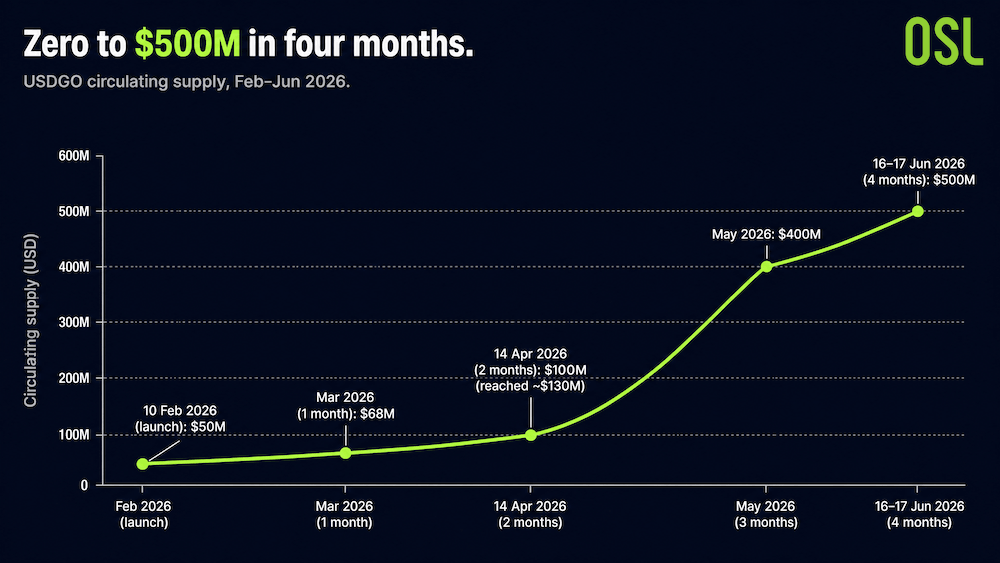

According to OSL's announcement via The Block, USDGO surpassed $500 million in circulation in mid-June 2026, four months after launch. The trajectory, $50M at launch, $68M after one month, $100M (reaching ~$130M) by 14 April, $400M in May, and $500M by mid-June, validates something the report argued in theory: there is genuine, unmet demand from Asia-Pacific institutions for a compliant US-dollar stablecoin built for business.

Chart 1: USDGO circulating supply (Feb–Jun 2026)

Source: OSL's announcement via The Block

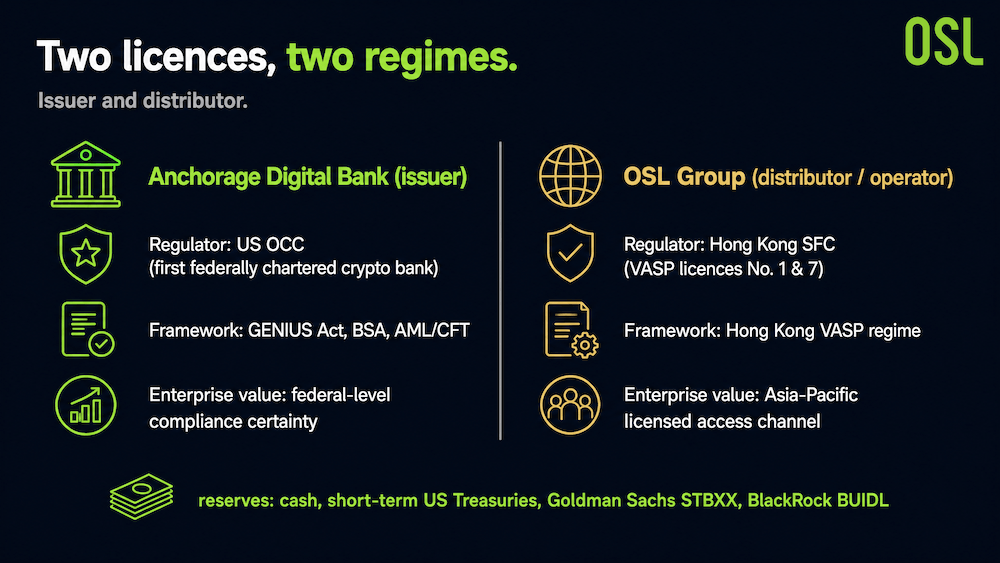

Why CFOs Are Willing to Use It: The Dual Licence

A treasury team cannot wire company money through an instrument its risk committee won't approve. USDGO's core design answer is a dual-licence structure that covers both major regulatory regimes: the issuer Anchorage operates under US OCC oversight and the GENIUS Act framework (alongside Bank Secrecy Act and AML/CFT obligations), while distributor OSL holds Hong Kong SFC VASP licences (No. 1 and No. 7) under the city's VASP regime.

Chart 2: USDGO's dual-licence architecture

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

The reserves reinforce that posture: cash, short-term US Treasuries, Goldman Sachs' STBXX fund, and BlackRock's BUIDL fund. For a CFO, holding USDGO is closer to holding an institutional money-market instrument than a crypto token, which is precisely the point.

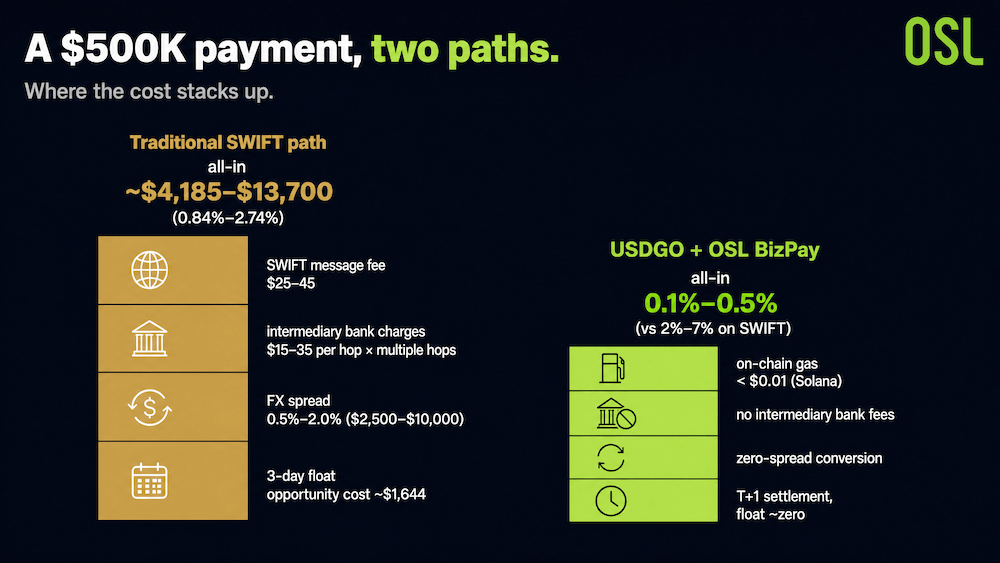

The $500K Payment Test

Theory is one thing. The report runs a concrete example: settling a $500,000 cross-border supplier payment.

On the traditional SWIFT path, the all-in cost stacks up across SWIFT message fees ($25–45), intermediary bank charges ($15–35 per hop, multiple hops), an FX spread of 0.5%–2.0% ($2,500–$10,000), and the opportunity cost of a 3-day float (~$1,644). Total: roughly $4,185–$13,700, or 0.84%–2.74%.

The USDGO + OSL BizPay path collapses most of that. On-chain gas runs under $0.01 on Solana, there are no intermediary bank fees, conversion is zero-spread, and T+1 settlement brings the float opportunity cost close to zero. Across the report's corridor analysis, all-in costs drop to 0.1%–0.5% versus 2%–7% on SWIFT.

Chart 3: Comparison of Cross-Border Payment Costs for $500,000

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

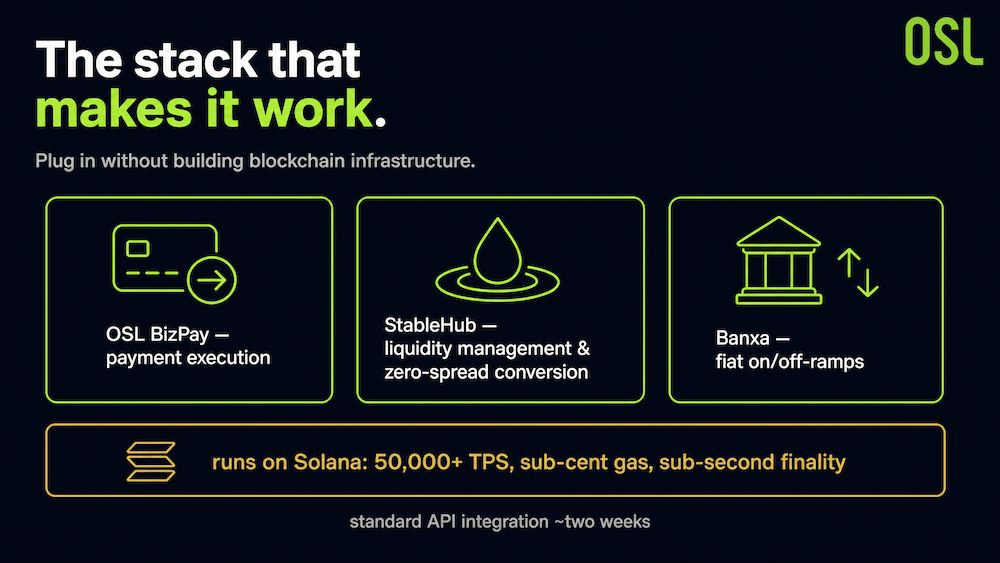

The Operating Stack Behind It

The cost numbers only matter if a business can actually plug in without building blockchain infrastructure. USDGO's ecosystem is designed around that: OSL BizPay handles payment execution, StableHub handles liquidity management and zero-spread stablecoin conversion, and Banxa handles fiat on/off-ramps. Standard API integration takes about two weeks, and USDGO runs on Solana (50,000+ TPS, sub-cent gas, sub-second finality), chosen for enterprise-grade throughput and predictable cost.

Chart 4: USDGO Operations Stack Architecture

The takeaway is not that USDGO has won anything yet. It's that a compliant, dual-licensed enterprise stablecoin, wired into a working payment stack, can scale to half a billion dollars in four months when it solves a real corridor problem. That is the signal worth watching.

FAQ

Q1: What is USDGO? A: A compliant enterprise stablecoin pegged 1:1 to the US dollar, issued by Anchorage Digital Bank (OCC-regulated) and distributed by OSL across Asia-Pacific, launched February 2026.

Q2: How fast did USDGO grow? A: From $50M at launch (Feb 2026) to $100M (April), $400M (May), and over $500M by mid-June 2026, about four months.

Q3: Why is USDGO considered compliant? A: It runs a dual-licence structure, US OCC (via issuer Anchorage) and Hong Kong SFC (via distributor OSL), under the GENIUS Act framework, with reserves in cash, Treasuries, Goldman Sachs STBXX, and BlackRock BUIDL.

Q4: How much does USDGO save on a cross-border payment? A: The report puts all-in costs at 0.1%–0.5% versus 2%–7% on SWIFT, with T+1 fiat settlement instead of 2–5 days.

References

Note: Industry analysis based on public sources and the cited report. Not investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

USDGO, a compliance-first enterprise stablecoin, hit $500M in four months. How its dual-licence design and payment stack solve cross-border B2B costs.

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Stablecoin transfers are fast and cheap on-chain, but the real costs hide at the on-ramp and off-ramp. Where stablecoin payments actually win, and don't.

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

Stablecoins come in three types, but only fiat-backed ones survived. How a $50B collapse and global regulation turned compliance into the real moat.

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

USDT and USDC control over 82% of the stablecoin market. Here's how the two coins differ and why new entrants keep failing to break the duopoly.

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Analyze SPCX stock's 50% surge and reversal. Learn why its low float, high FDV structure mirrors crypto tokens and what future unlocks mean for price.

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Recommended for you

More topics

More topics