Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Introduction: When Software Starts Paying for Itself

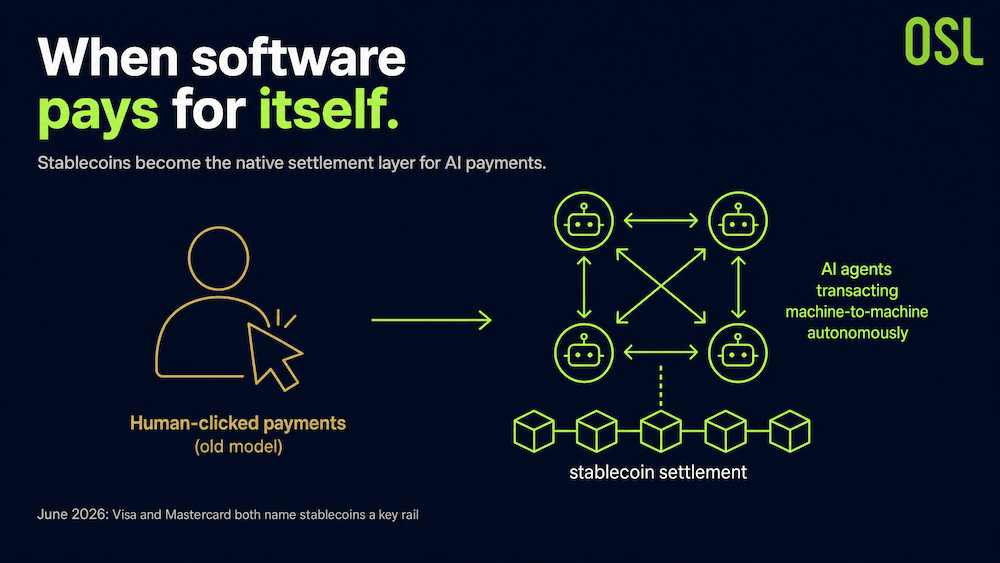

Payments are evolving. In the past, every transaction involved a person clicking “Confirm”; but as AI agents begin to make purchases, reconcile accounts, and call upon services on demand independently, payments have become the immediate output of software logic rather than the downstream execution of human commands.

In June 2026, this trend moved from the conceptual stage to the infrastructure layer of payment networks. On the same day, Visa and Mastercard each announced payment solutions for AI agents, and both listed stablecoins as one of their key settlement channels. This was no coincidence—it confirmed the assessment that stablecoins are becoming the native settlement layer for AI payments.

Chart 1:AI-Powered Autonomous Payments

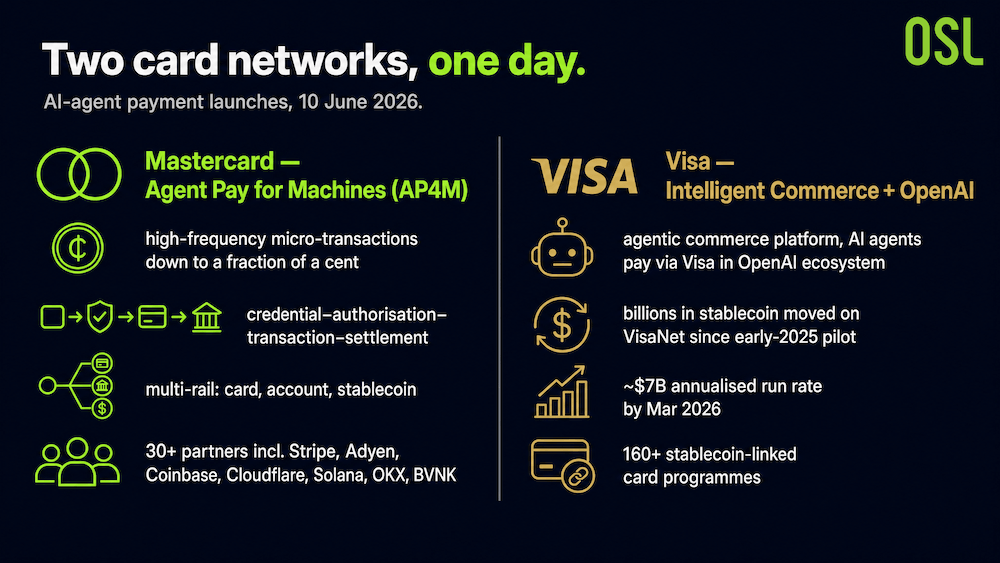

June 2026: Two Major Card Networks Launch on the Same Day

Mastercard Launches “Agent Pay for Machines” (AP4M)

According to an official Mastercard press release (June 10, 2026), Agent Pay for Machines (AP4M) is designed for high-frequency, low-latency microtransactions—as small as a fraction of a cent—between AI agents. It provides four core capabilities—“tokenization, authorization, transaction, and settlement”—and explicitly supports multi-track settlement via cards, accounts, and stablecoins.

Jorn Lambert, Mastercard’s Chief Product Officer, stated that AP4M will create the conditions for a “superbloom” in AI business models—“Machine payments enable services to be bought and sold between agents on a scale fundamentally different from today’s: extremely high frequency, extremely small amounts, extremely fast, and with extremely low latency.”

The initial group of more than 30 partners includes Stripe, Adyen, Coinbase, Cloudflare, Solana, OKX, and stablecoin payment infrastructure provider BVNK. Chris Harmse, co-founder and Chief Commercial Officer of BVNK, said, “We believe stablecoins will play a powerful role in this transformation, bringing greater speed, programmability, and efficiency to the flow of value.”

Visa Partners with OpenAI to Launch Intelligent Commerce

On the same day, according to an official Visa press release (June 10, 2026), Visa launched Visa Intelligent Commerce, an agent-based commerce platform, at Payments Forum 2026, and announced a strategic partnership with OpenAI to enable AI agents to process Visa payments within the OpenAI ecosystem.

Jack Forestell, Visa’s Chief Product and Strategy Officer, put it succinctly: “AI is reshaping the front end of commerce, and stablecoins are reshaping the back end.” Regarding stablecoin settlements, Visa revealed that since the pilot began in early 2025, it has processed tens of billions of dollars in stablecoins on VisaNet. As of March 2026, the annualized run rate stood at approximately $7 billion, with more than 160 stablecoin-linked card programs worldwide.

Chart 2:Visa and Mastercard Announce AI-Powered Payment Solutions on the Same Day

Source: an official Mastercard press release (June 10, 2026), an official Visa press release (June 10, 2026)

Why Does the AI Agent Economy Need a New Payment Layer?

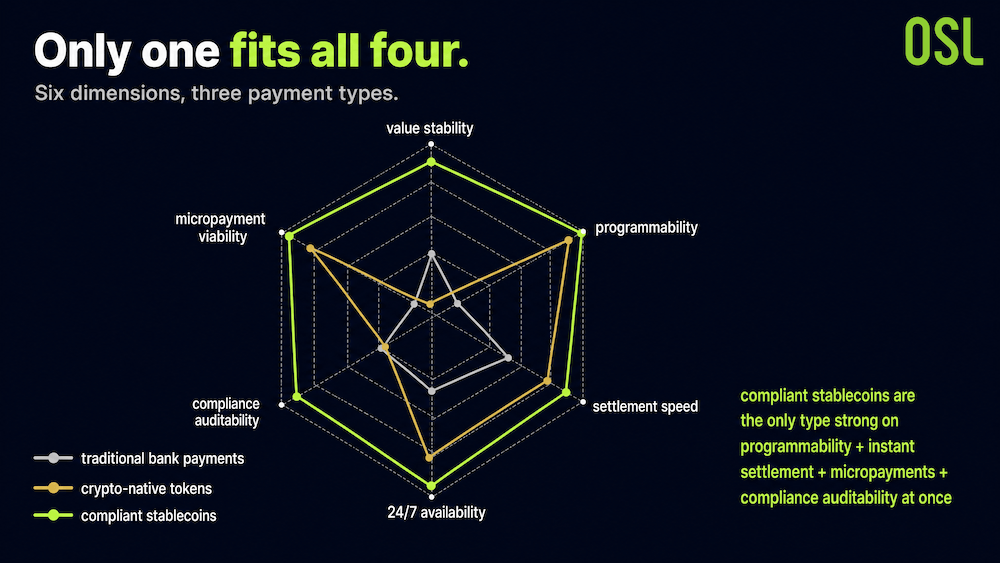

AI agents are software programs capable of autonomously executing complex business tasks: procurement agents automatically compare prices and place orders; financial agents monitor invoices in real time and trigger payments; and logistics agents dynamically settle payments based on shipping cost fluctuations. In these scenarios, traditional payment infrastructure faces structural obstacles—bank accounts require human signatures for authorization, cross-border wire transfers have fixed processing windows, and anti-money laundering (AML) reviews introduce unavoidable delays. These designs are all centered around “manual operations.”

AI agents, however, require four key elements: programmable triggers that do not require human approval; 24/7 instant settlement; integration with smart contracts that execute automatically according to predefined rules; and traceable on-chain audit trails. Stablecoins happen to outperform traditional payment channels in all four of these areas.

Chart 3:A Comparison of the Suitability of Three Types of Payment Infrastructure for the AI Agent Economy

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

Compliant stablecoins are the only payment method that meets all four criteria: “programmability, instant settlement, micropayments, and compliance and auditability.”

Card Track vs. Stablecoin Track: An Ongoing Divergence

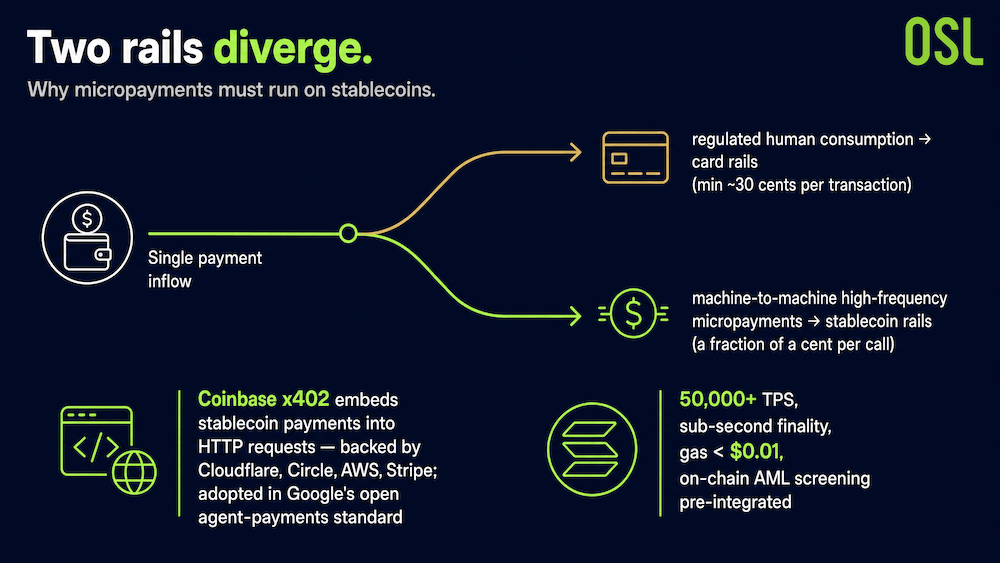

Why can micropayments only operate on stablecoins? The answer lies in economics. The minimum fee per transaction on traditional card networks is about 30 cents, while a single call to an AI agent—purchasing computing power, retrieving data, and hiring sub-agents—may be worth only a fraction of a cent; the card network model simply cannot be viable at this scale.

This has given rise to a potential division of labor: regulated human consumer transactions remain on the card network, while high-frequency machine-to-machine micropayments migrate to the stablecoin network. Coinbase’s x402 protocol—which embeds stablecoin payments directly into HTTP requests—is already supported by Cloudflare, Circle, AWS, and Stripe, and Google’s Open Proxy Payment Standard also incorporates x402 into its settlement layer. (Source: CoinDesk, March 15, 2026; American Banker, June 12, 2026)

Chart 4:Conceptual Diagram of the Split Between Card Track and Stablecoin Track

Source: CoinDesk, March 15, 2026; American Banker, June 12, 2026

Technical Compatibility of Stablecoins: The Case of Solana

The report notes that when compliant stablecoins are deployed on high-throughput public blockchains, their technical suitability is particularly evident. Take Solana as an example: over 50,000 TPS supports large-scale concurrent payment batch processing; sub-second finality eliminates the waiting costs associated with AI agent state machines; and gas fees of less than $0.01 per transaction make “per-task execution fees” economically viable. At the same time, on-chain address screening tools (such as Chainalysis) can be integrated upfront into the agent’s smart contract logic to complete AML screening before funds are transferred—thereby achieving compliance automation rather than compliance friction.

From Payment Tools to Programmable Money: Obstacles Are Being Systematically Overcome

The long-term value of stablecoins lies not only in payment efficiency, but also in their role as a programmable monetary foundation connecting DeFi and the real economy. However, there are still obstacles to widespread adoption—the good news is that these obstacles are being systematically addressed.

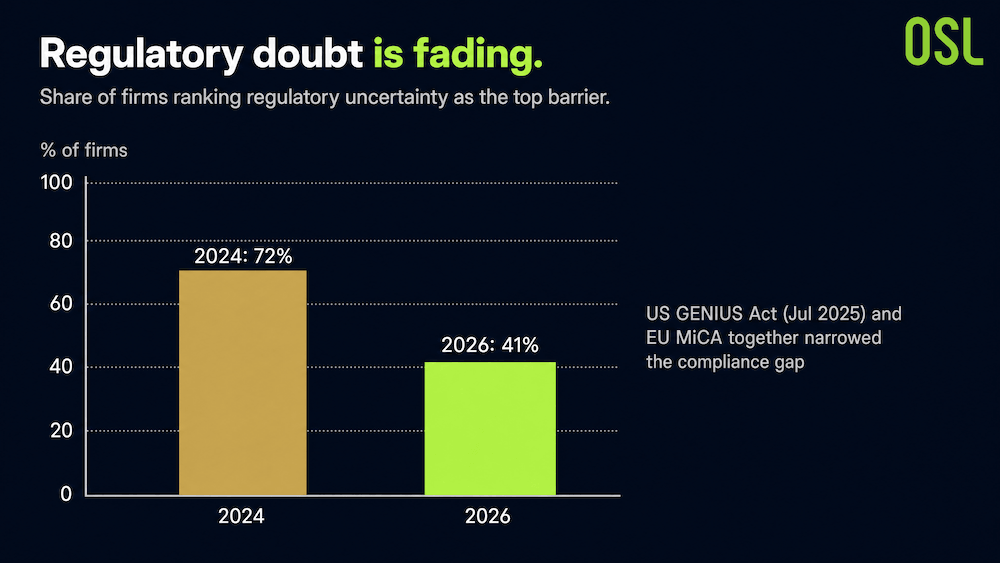

Chart 5:A Comparison of Barriers to Adoption of Corporate Stablecoins

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

The percentage of companies citing “regulatory uncertainty” as their top obstacle fell from 72% in 2024 to 41% in 2026—as the U.S. GENIUS Act (July 2025) and the EU’s MiCA jointly narrowed the scope of compliance requirements.

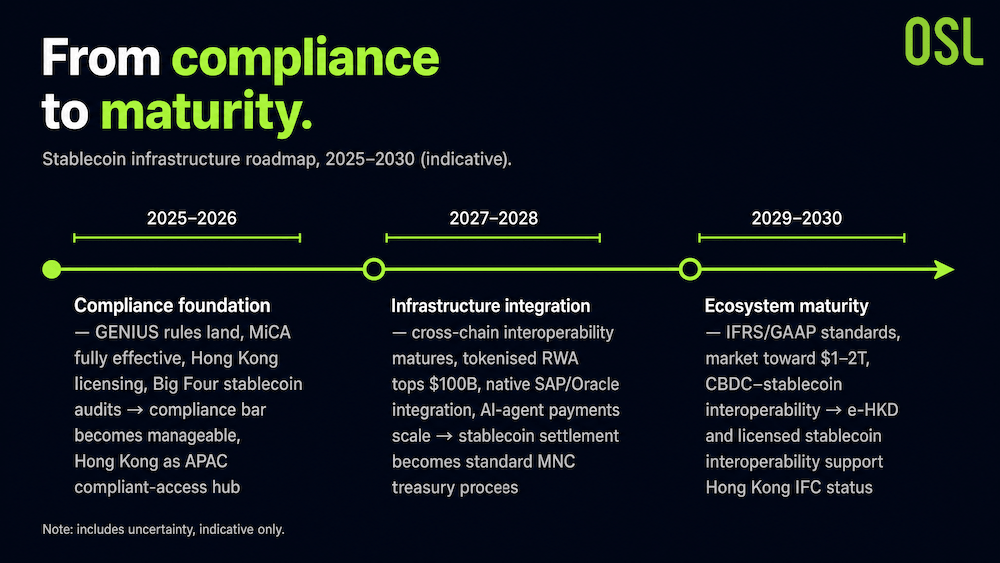

Chart 6:Roadmap for the Evolution of Stablecoin Infrastructure, 2025–2030

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

Market Scale: Stablecoins Have Become Infrastructure on Par with Mainstream Payment Networks

Underpinning all of this is the scale that stablecoins have already reached. According to the report’s data:

In 2025, the nominal on-chain settlement volume of stablecoins exceeded 33 trillion U.S. dollars, surpassing the combined volume of Visa (approximately 15.7 trillion) and Mastercard (approximately 9.8 trillion) on a nominal basis.

The tokenized RWA market is projected to surpass $30 billion by May 2026, with BlackRock’s BUIDL fund alone holding approximately $2.5 billion in AUM.

According to a 2026 estimate by the McKinsey Global Institute, the volume of autonomous transactions conducted by AI agents in the global business services sector could reach the trillions of dollars by 2030.

This means that stablecoins are no longer merely a pricing tool within the crypto market, but rather a settlement infrastructure comparable to mainstream global payment networks.

Conclusion: Infrastructure Determines Who Will Win in AI Payments

Visa’s statement that “AI reshapes the front end, while stablecoins reshape the back end” accurately summarizes the division of labor in this transformation. AI agents are responsible for understanding intent and making decisions; but when they need to pay for those decisions, they require a settlement pathway capable of handling “fractions of a cent, tens of thousands of transactions per second, 24/7 operation, programmability, and auditability”—and this is precisely where stablecoins excel.

The simultaneous launch of the two major card networks in June 2026 marks the beginning of the infrastructure race for AI payments. Whoever can best combine the programmable settlement capabilities of stablecoins with the trust and compliance of global networks will hold the ticket to the next generation of commerce.

FAQ

Q1: What is agentic commerce? A: It refers to a payment model in which an AI agent (software) independently initiates and completes transactions on behalf of users or businesses. It is commonly seen in machine-to-machine scenarios involving high-frequency, small-value, and automated transactions.

Q2: Why are stablecoins suitable for agentic commerce? A: Stablecoins offer programmability (triggered by smart contracts), instant settlement, 24/7 availability, extremely low per-transaction costs (gas < $0.01), and on-chain auditability—all of which align with the requirements of automated payments by AI agents.

Q3: What did Visa and Mastercard do in June 2026? A: On June 10, 2026, Visa launched Intelligent Commerce in partnership with OpenAI, while Mastercard introduced Agent Pay for Machines; both support multi-track settlement using stablecoins.

Q4: Why can’t traditional card networks handle micropayments from AI agents? A: The minimum per-transaction fee on card networks is approximately 30 cents, whereas a single call from an AI agent may be worth only a fraction of a cent. This is not economically viable, so micropayments are better suited for stablecoin channels.

References

Note: This article is an industry analysis compiled from publicly available information and reports and does not constitute investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

USDGO, a compliance-first enterprise stablecoin, hit $500M in four months. How its dual-licence design and payment stack solve cross-border B2B costs.

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Stablecoin transfers are fast and cheap on-chain, but the real costs hide at the on-ramp and off-ramp. Where stablecoin payments actually win, and don't.

Stablecoins Aren't Instant or Free: Where the Real Costs Hide

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

Stablecoins come in three types, but only fiat-backed ones survived. How a $50B collapse and global regulation turned compliance into the real moat.

Why Compliance Won: The Quiet Death of Algorithmic Stablecoins

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

USDT and USDC control over 82% of the stablecoin market. Here's how the two coins differ and why new entrants keep failing to break the duopoly.

USDT vs USDC: Inside the Stablecoin Duopoly That Controls 82% of the Market

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Analyze SPCX stock's 50% surge and reversal. Learn why its low float, high FDV structure mirrors crypto tokens and what future unlocks mean for price.

From $135 to $225 and Back in a Week: Is SPCX a Classic Case of "Low Float, High FDV"?

Recommended for you

More topics

More topics