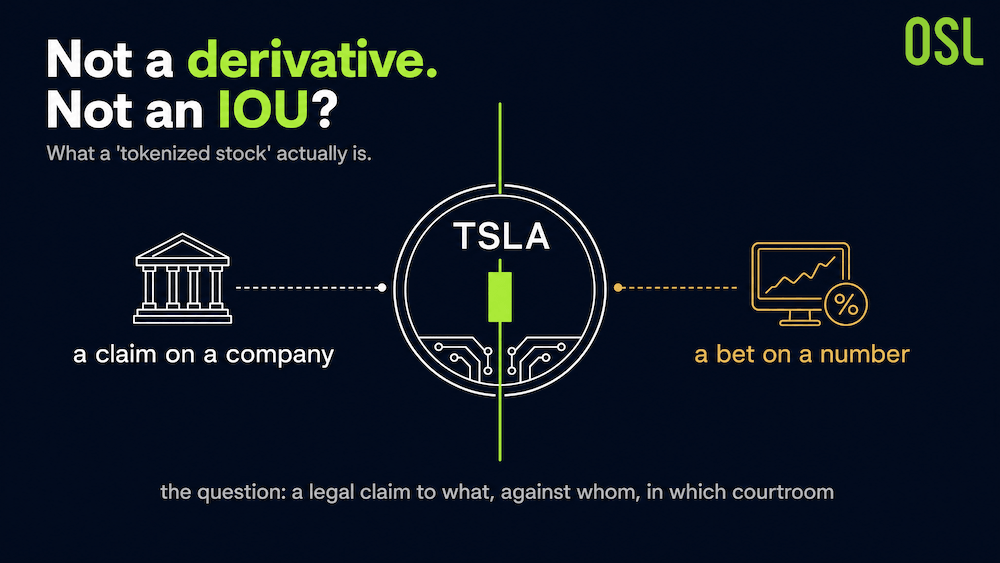

"Not a Derivative. Not an IOU." Why a CEO Had to Say the Quiet Part Out Loud

When Brian Armstrong went on CNBC in mid-June to unveil Coinbase's tokenized US stocks, the striking part wasn't the product. It was the disclaimer he led with. Each token, he said, is backed one-to-one by a real share, with automatic dividends and on-chain redemption, and then, pointedly: "Not a derivative. Not an IOU."

Chart 1: Tokenized Stocks

Stop and ask why a chief executive needs to promise you that what he's selling is what it appears to be. You don't hear a brokerage insisting that the Apple shares in your account are "not a derivative." The reassurance is necessary only because, across the rest of this booming market, the opposite is often true. Armstrong was saying the quiet part out loud: a great many things currently marketed as "tokenized stocks" are not stocks at all.

That gap, between what you control on screen and what you actually own in law, is the whole story of tokenized equities in 2026. And it's about to get harder to see, not easier.

The interface converges; the rights don't

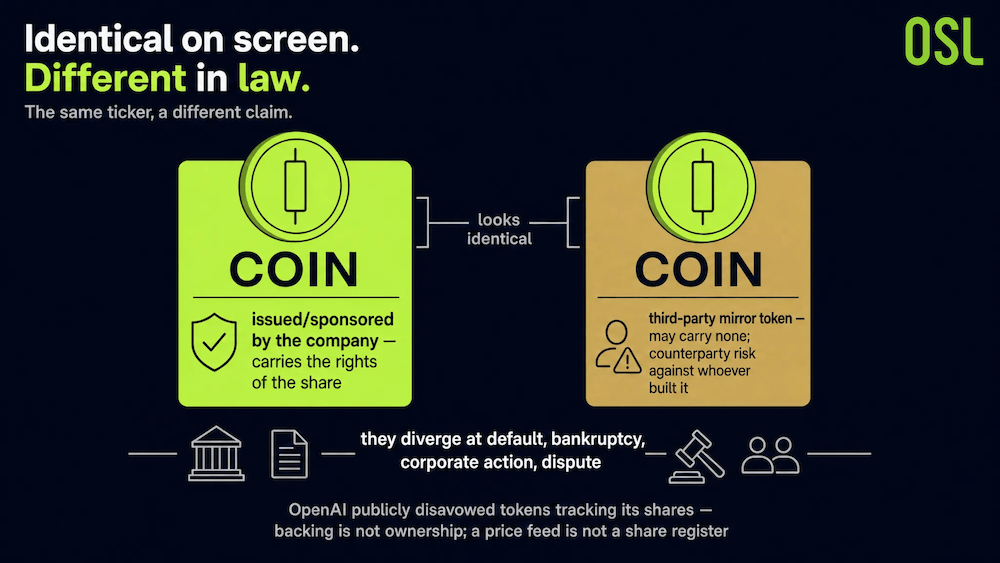

A token that tracks Tesla and a token that is a claim on Tesla can look identical. Same ticker, same price chart, same one-tap purchase with a stablecoin. They diverge only at the moment you need them to hold: a default, a bankruptcy, a corporate action, a dispute. One is a claim on a company. The other is a bet on a number.

US regulators have been unusually clear about this. In a January statement on tokenized securities, the SEC's staff said the format doesn't change the law: a security is a security whether its ownership is recorded on a corporate ledger or on a blockchain. But the same statement drew a line that most marketing blurs. A token issued or sponsored by the company carries the rights of the share. A token minted by an unaffiliated third party to mirror a share may carry none of them, and leaves you holding counterparty risk against whoever built it, not the company on the label.

The cleanest illustration came a year earlier, when OpenAI publicly disavowed tokenized "equity" tied to its shares after the tokens appeared on a European retail app. The company never issued them, never recognized them, and said so. The token could track OpenAI tick for tick and still owe its holder nothing OpenAI acknowledged. Backing is not ownership; a price feed is not a share register.

Chart 2: Comparison of Tokenized Stocks

The regulator is stuck on the same line

Here's where the timing gets interesting. Even as the SEC insists the rules already cover these products, it is reportedly preparing to loosen them. According to Reuters reporting summarized in industry coverage, Chair Paul Atkins is expected to roll out an "innovation exemption" that would let firms offer blockchain-based stocks without full compliance with existing disclosure and investor-protection rules.

Read that against the ownership problem and the contradiction is obvious. An exemption that permits economic exposure without full shareholder rights would mass-produce exactly the two-look-alike-tokens situation: one a claim, one a tracker, trading side by side and resolving completely differently when stressed. Commissioner Hester Peirce, no enemy of crypto, reportedly wants the carve-out to cover only tokens that confer the same rights as the underlying share. That caveat is the entire ballgame. Whether it survives into the final rule decides whether the exemption clarifies the market or industrializes its central confusion.

A market built offshore, by design

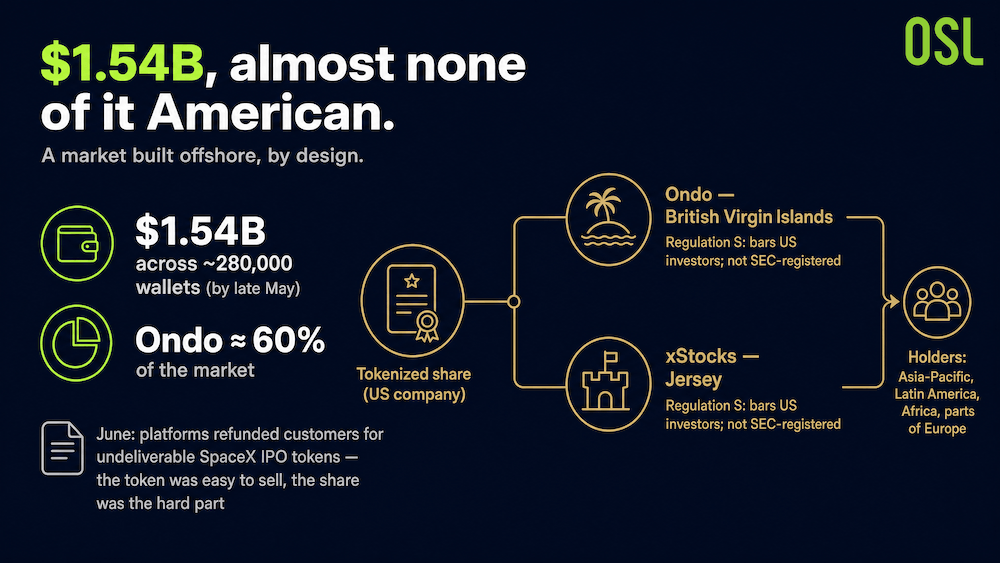

The confusion isn't a fringe problem. Tokenized stocks passed $1.54 billion across nearly 280,000 wallets by late May, with Ondo alone making up roughly 60%. And almost none of those holders are American. The two largest issuers operate under Regulation S, a US exemption that bars US investors outright; their customers sit in Asia-Pacific, Latin America, Africa, and parts of Europe. Effectively every tokenized US stock today is owned by someone outside the US.

That offshore structure isn't incidental; it's load-bearing, and it compounds the rights question. The big issuers are registered far from the company whose name is on the token: Ondo in the British Virgin Islands, xStocks in Jersey, neither registered with the SEC. So your counterparty is an offshore entity, and if the relationship breaks, you're left working out whose creditor you are and in which jurisdiction. The market got a small preview of that earlier in June, when a wave of crypto platforms had to refund customers for SpaceX IPO tokens they couldn't actually deliver. The token was easy to sell. The share behind it was the hard part.

Chart 3: Offshore Structures for Tokenized U.S. Stocks

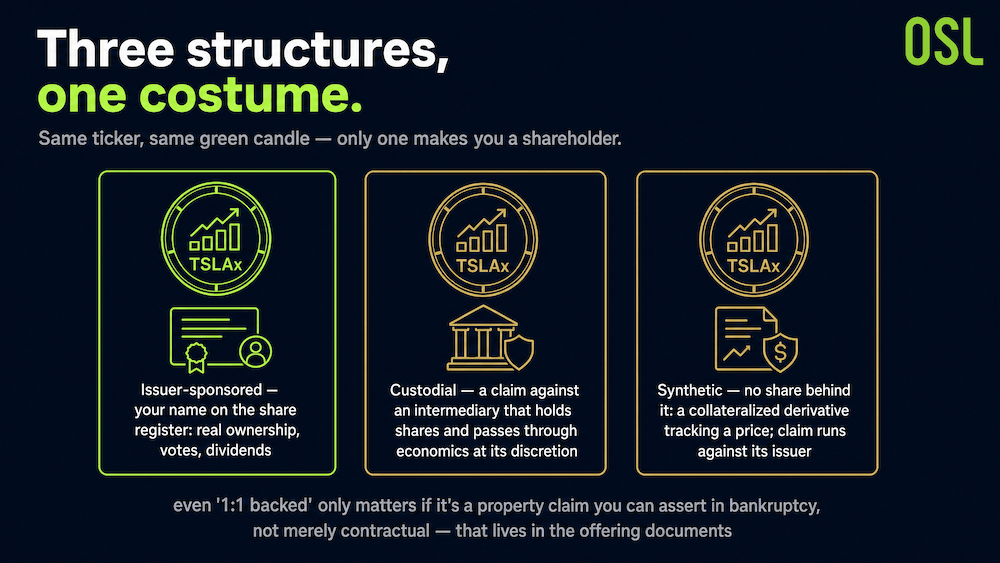

Three structures wearing the same costume

Strip away the branding and almost everything sold as a "tokenized stock" is one of three things. An issuer-sponsored token puts your name, in effect, on the company's share register: real ownership, real votes, real dividends. A custodial token is a claim against an intermediary that holds shares on your behalf and passes through economics at its discretion. A synthetic token has no share behind it at all; it's a collateralized derivative engineered to track a price, and your claim runs against its issuer.

All three can display the same ticker and the same green candle. Only the first makes you a shareholder. This is why Armstrong's four blunt words were a marketing weapon: in a field crowded with custodial and synthetic products, "not a derivative, not an IOU" is a direct shot at competitors whose tokens are exactly that. Even then, the promise is only as good as the custody arrangement underneath it: whether "1:1 backed" means a property claim you can assert in a bankruptcy or merely a contractual one. That detail lives in the offering documents, not the press release.

Chart 4: A Comparison of Three Structures for Tokenized Stocks

The question that survives every upgrade

Tokenization is genuinely useful infrastructure, and it isn't going away; access to US equities is drifting on-chain the way dollars already did. The interfaces will keep getting smoother: faster settlement, lower minimums, stablecoin rails, wallet withdrawal, collateral and lending stacked on top.

None of that changes the only question that has ever mattered here. Not what the screen shows, not what the token tracks, but what you have a legal claim to, against whom, and in which courtroom. When a CEO has to promise you it's "not an IOU," treat it as a reminder that, for much of this market, an IOU is precisely what's on offer.

FAQ

Q1: Does buying a tokenized stock mean I own the actual share? A: Not necessarily. It depends on the structure. Only an issuer-sponsored token puts you on the company's share register with real ownership, votes, and dividends. Custodial and synthetic tokens give you a claim against an intermediary or issuer, not against the company on the label.

Q2: What are the three types of tokenized stocks? A: Issuer-sponsored (real ownership backed by the company), custodial (a claim against an intermediary that holds shares and passes through economics at its discretion), and synthetic (a collateralized derivative with no share behind it, engineered to track a price).

Q3: Why are tokenized US stocks mostly owned outside the US? A: The two largest issuers operate under Regulation S, a US exemption that bars US investors. Issuers like Ondo (British Virgin Islands) and xStocks (Jersey) are registered offshore and not with the SEC, so holders sit in Asia-Pacific, Latin America, Africa, and parts of Europe.

Q4: What should I check before buying a tokenized stock? A: Find out which of the three structures it is, who your counterparty is and where they are registered, and whether "1:1 backed" means a property claim you can assert in a bankruptcy or merely a contractual one. That detail lives in the offering documents, not the press release.

The views and opinions expressed in this article are solely those of the author and do not constitute professional financial advice.

Sources

RWA Bible: Coinbase Announces 1:1 Real-Share-Backed Tokenized US Stocks (June 16, 2026)

One Asset (summarizing Reuters): The Exemption That Splits the Token From the Right (June 22, 2026)

SEC: Statement on Tokenized Securities (Jan 28, 2026)

American Banker: Tokenized stocks are coming, whether US regulators like them or not (June 26, 2026)

Kodex Academy: Are Tokenized Stocks Legal? Yes, but What Do You Own (June 8, 2026)

TT3Labs: A Digital Nomad's View on Tokenized US Stocks (June 25, 2026)

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

The Crypto Exchange Wants to Be Your Only Account

Crypto exchanges are adding stocks, options and AI advisors to become super apps. They're not after your next trade, but your whole account, and its risks.

The Crypto Exchange Wants to Be Your Only Account

"Not a Derivative. Not an IOU." Why a CEO Had to Say the Quiet Part Out Loud

A token can carry a stock's ticker and price yet grant none of a shareholder's rights. The three structures behind tokenized stocks, and what you really own.

"Not a Derivative. Not an IOU." Why a CEO Had to Say the Quiet Part Out Loud

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

USDGO, a compliance-first enterprise stablecoin, hit $500M in four months. How its dual-licence design and payment stack solve cross-border B2B costs.

Zero to $500 Million in Four Months: Inside the USDGO Enterprise Stablecoin

Recommended for you

More topics

More topics