The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

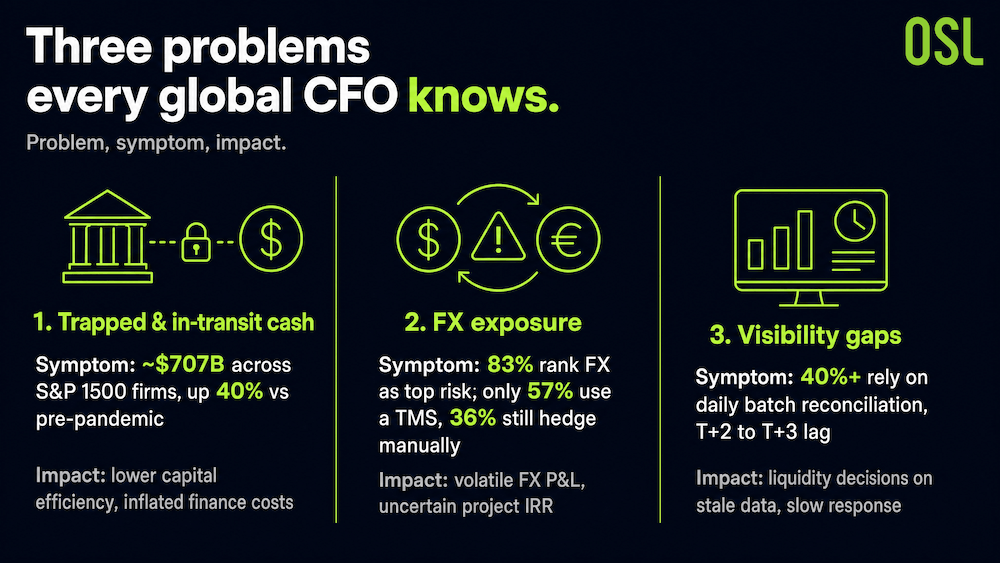

Three Problems Every Global CFO Knows

The problems stablecoins are meant to solve are worth naming first. The report, drawing on PwC's 2025 Global Treasury Survey and Nomentia's data, identifies three: roughly $707 billion in trapped and in-transit cash across S&P 1500 firms (up 40% versus pre-pandemic); FX exposure that 83% of CFOs rank as their top risk, even though only 57% use a treasury management system and 36% still hedge manually; and visibility gaps, with more than 40% of large multinationals relying on daily batch reconciliation that lags two to three days.

Chart 1: Three Major Structural Issues in Cross-Border Finance

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business), PwC

These are not edge cases. They are the daily reality of managing money across 50+ legal entities and a dozen time zones with infrastructure designed for a slower era.

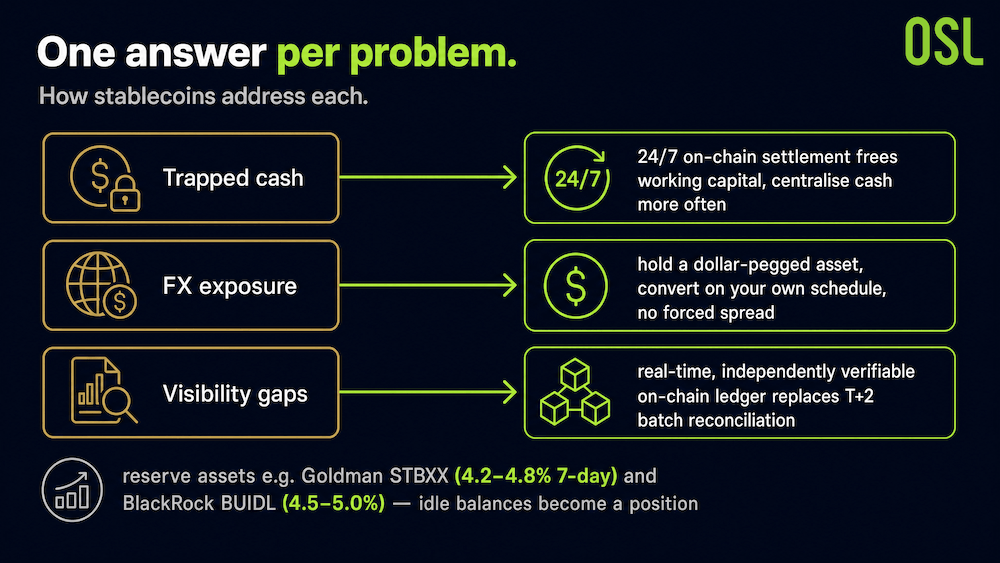

How Stablecoins Address Each One

Stablecoins map onto these three problems with unusual precision.

For trapped cash, 24/7 on-chain settlement means capital no longer sits idle waiting for banking windows. As PwC noted, with round-the-clock liquidity access, corporates can centralise cash more frequently, freeing working capital and putting excess balances to work.

For FX exposure, a dollar-pegged stablecoin lets a receiving entity hold value as a dollar-equivalent asset and convert on its own schedule, rather than eating a forced spread on every cross-border leg.

For visibility, an on-chain ledger gives real-time, independently verifiable transaction records, replacing T+2 batch reconciliation with live position data.

Chart 2: Mapping of Stablecoin Solutions to the Three Major Financial Challenges

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business), PwC

There's a yield angle too. In the report's example, reserve assets like Goldman Sachs' STBXX (4.2–4.8% 7-day yield) and BlackRock's BUIDL (4.5–5.0%) mean holding a compliant stablecoin can indirectly participate in institutional money-market returns, turning idle balances from a cost into a position.

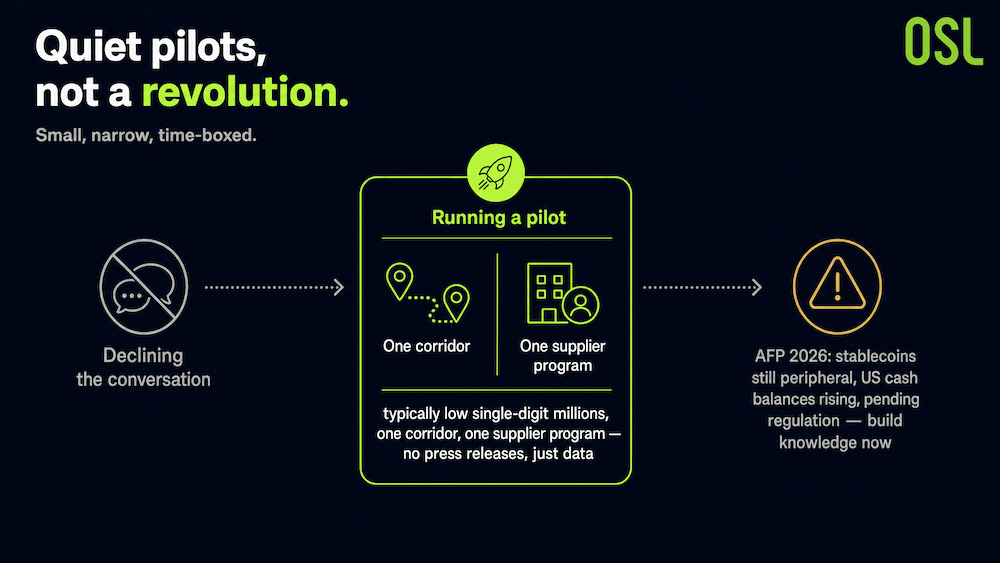

The Honest Picture: Quiet Pilots, Not a Revolution

Balance matters here, because the hype and the reality diverge.

Chart 3: Quiet Pilot Program for Financial Stablecoins

The hype says treasury is being transformed. The reality, as FintekCafe reported in May 2026, is quieter: treasury teams at multinational manufacturers, tech platforms, commodity traders, and retailers have moved from declining the conversation to running small, narrow, time-boxed pilots, typically low single-digit millions, one corridor, one supplier program. No press releases. Just data.

And plenty of caution remains. The AFP's 2026 Liquidity Survey, released in June 2026, found treasury teams increasing US cash balances and keeping stablecoins firmly on the periphery, citing pending regulation. As AFP's Tom Hunt put it, with the GENIUS Act passed and more rules in development, treasury teams "need to build their knowledge now, so they can make informed decisions once the rules are finalised."

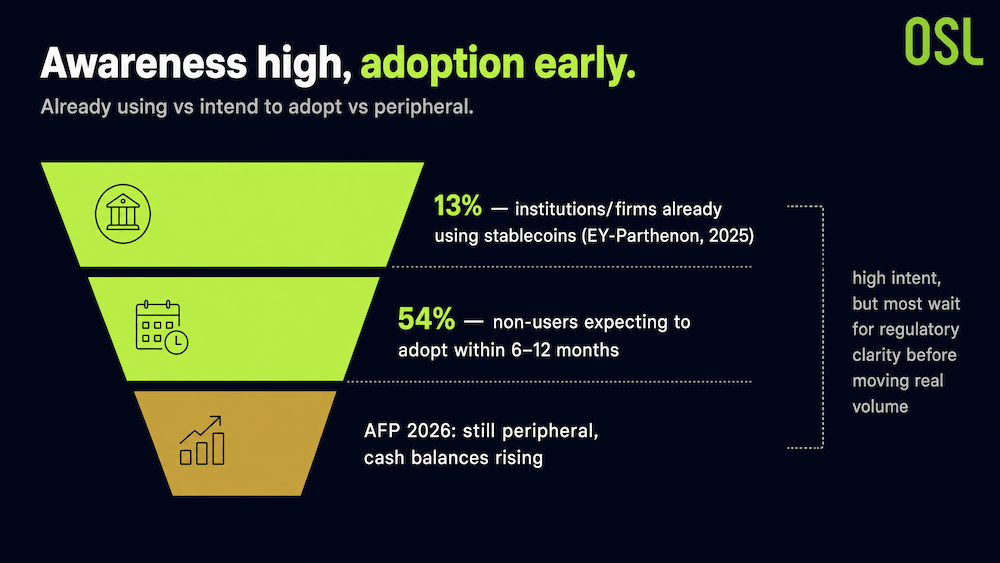

Chart 4: A Funnel Chart for Stablecoin Finance

Source:AFP's 2026 Liquidity Survey

The two findings are not contradictory. Awareness is high and intent is building, but most teams are waiting for regulatory clarity before moving real volume. That is exactly what a healthy, cautious adoption curve looks like.

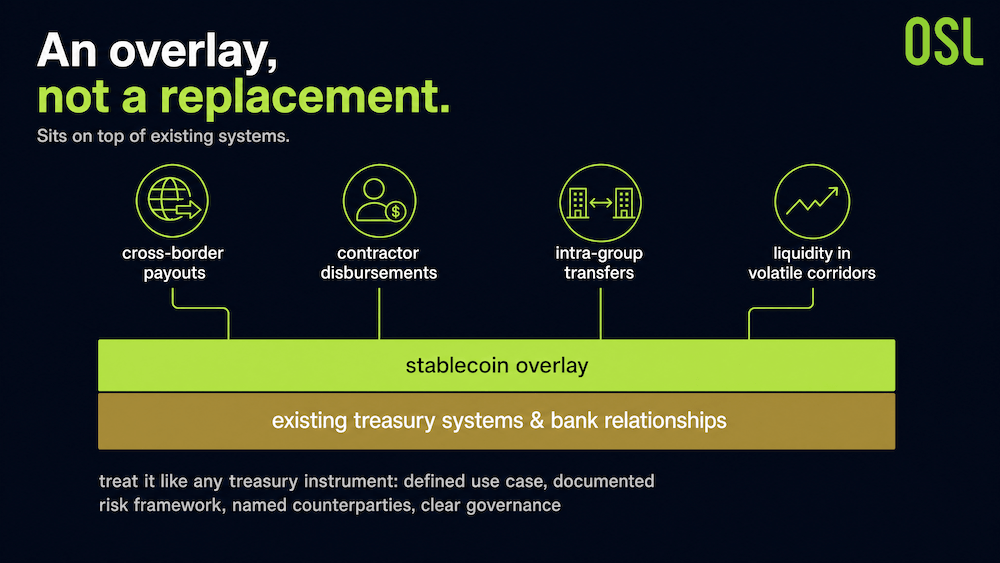

The Right Mental Model: Overlay, Not Replacement

Treating stablecoins as a wholesale replacement for the treasury stack is the wrong model. The report, PwC, and FintekCafe all land on the same framing: stablecoins are an overlay. They sit on top of existing systems and bank relationships, deployed for a defined set of problems—cross-border payouts, contractor disbursements, intra-group transfers, liquidity in volatile corridors—rather than ripping anything out.

The CFOs getting value from stablecoins in 2026 treat them like any other treasury instrument: a defined use case, a documented risk framework, named counterparties, and clear governance. It works as a new tool in the kit, used precisely where it beats the alternative.

Chart 5: Mental Model Diagram of a Stablecoin Overlay Layer

FAQ

Q1: What problems do stablecoins solve for corporate treasury? A: Three: trapped and in-transit cash (~$707B across S&P 1500 firms), FX exposure (the top risk for 83% of CFOs), and visibility gaps (40%+ still rely on T+2/T+3 batch reconciliation).

Q2: Are companies actually using stablecoins in treasury? A: Yes, but quietly. In 2026, adoption is mostly small, corridor-specific pilots. EY-Parthenon found 13% of firms already use stablecoins and 54% of non-users expect to within 6–12 months.

Q3: Should stablecoins replace a company's treasury systems? A: No. The consensus framing is an overlay; stablecoins sit on top of existing systems for specific use cases, not a wholesale replacement.

Q4: Why are some treasury teams still cautious? A: Pending regulation. The AFP's 2026 survey found teams keeping stablecoins peripheral and raising cash balances while rules finalise.

References

Note: Industry analysis based on public sources and the cited report. Not investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

Explore if stablecoins can lower global remittance costs (currently 6%) and their role in solving financial exclusion in orphaned corridors.

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

Discover how stablecoins restructure B2B payments, reduce costs by 70%, and solve the $27T trapped liquidity issue in the SWIFT network.

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

Explore the three stages of stablecoin evolution: from exchange trading chips and DeFi liquidity to becoming global compliant payment infrastructure.

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Discover how stablecoins address trapped cash, FX risk, and visibility gaps in corporate treasury through quiet pilots and institutional adoption.

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Discover the significance of Bitcoin's 200-week SMA, historical returns, and how to use technical indicators for long-term crypto investing.

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Analyze Bitcoin market structure using on-chain data. Learn why the recent sell-off's realized loss is half of the previous round.

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Recommended for you

More topics

More topics