SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

The Misconception at the Heart of Cross-Border Payments

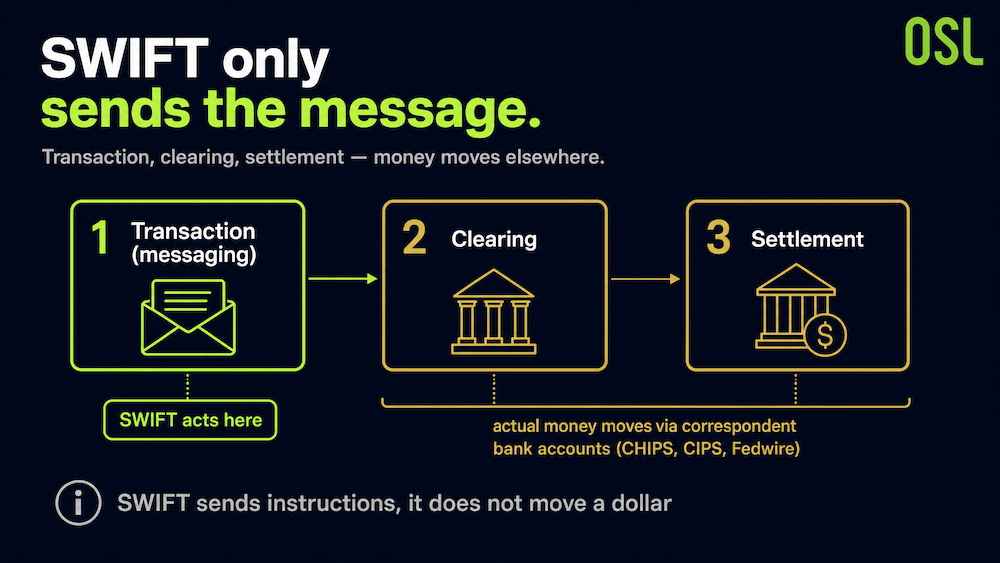

One fact reframes the whole debate: a cross-border payment has three stages—transaction, clearing, and settlement—and SWIFT only touches the first one.

SWIFT is a financial messaging network. It sends payment instructions between banks. It does not calculate who owes what, and it does not move a single dollar. The actual clearing and settlement happen elsewhere, in systems like CHIPS, CIPS, and Fedwire, and the money itself moves by being debited and credited along a chain of correspondent bank accounts.

That distinction matters enormously. It means the cost and delay in cross-border payments do not come from slow messaging. They come from the funds flow—money inching through layers of intermediary banks, each taking a fee and adding a delay point.

Chart 1: The Three Stages of Cross-Border Payments

The $27 Trillion Hiding in the Plumbing

To make this chain work, banks pre-fund accounts with each other, called Nostro and Vostro accounts, in multiple currencies and jurisdictions. No money actually crosses borders; ledger entries do. But to guarantee settlement is always possible, banks must park enormous sums in these accounts.

According to BIS estimates cited in the report, roughly $27 trillion sits in these pre-funded accounts as "trapped liquidity"—capital that earns little and exists only to keep the rails moving. At a 5% rate, every $1 billion parked carries an annual opportunity cost of about $50 million. That cost ultimately flows back to businesses through spreads and fees.

Chart 2: Cross-Border Payments Stuck in a Liquidity Bind

Why SWIFT gpi Didn't Fix the Speed Problem

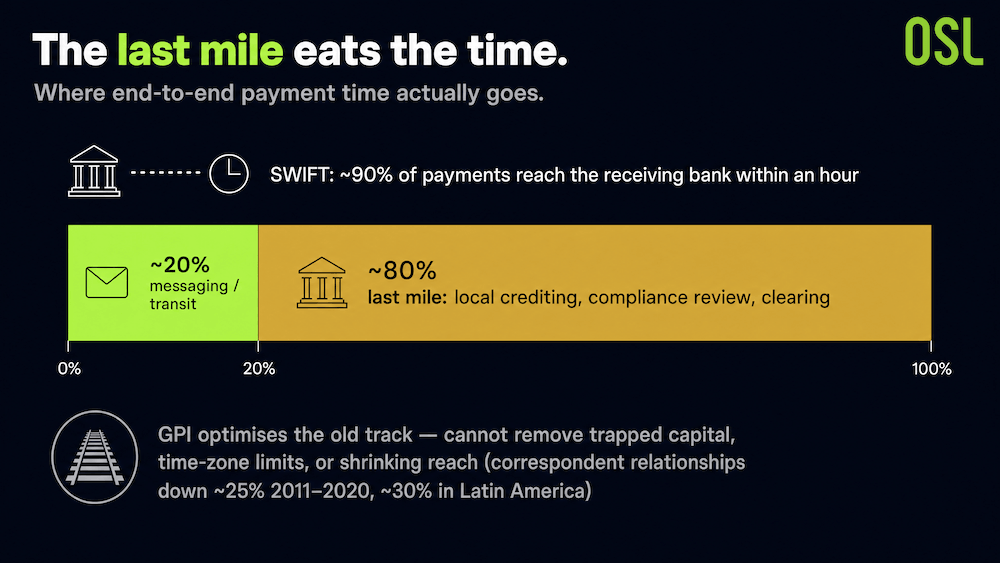

The usual counterargument is that SWIFT gpi already made things fast. The data tells a more revealing story.

SWIFT's own figures show about 90% of cross-border payments reach the receiving bank within an hour. Impressive, until you read the next line: research shows roughly 80% of the end-to-end time is spent in the "last mile"—local crediting, compliance review, and clearing at the receiving end. gpi still runs entirely on the correspondent bank network, with the same fee variability and cut-off constraints.

In other words, gpi is an optimisation of the old track. It improves messaging efficiency and transparency, but it cannot remove the trapped capital, time-zone constraints, and shrinking reach baked into the "multi-level credit agent" architecture. And that reach really is shrinking: active correspondent banking relationships fell about 25% between 2011 and 2020 (nearly 30% in Latin America).

Chart 3: Breakdown of End-to-End Processing Times for SWIFT gpi

The Honest Framing: A Parallel Rail, Not a Replacement

Declaring SWIFT dead would be a mistake.

As the US Federal Reserve noted in March 2026, stablecoins can shorten the payment chain and cut costs at each node, including compliance, but the correspondent banking model may persist thanks to scale economies and multi-jurisdiction compliance advantages. Banks still control fiat access, credit, custody, local payout, and liquidity, and SWIFT itself is building distributed-ledger infrastructure.

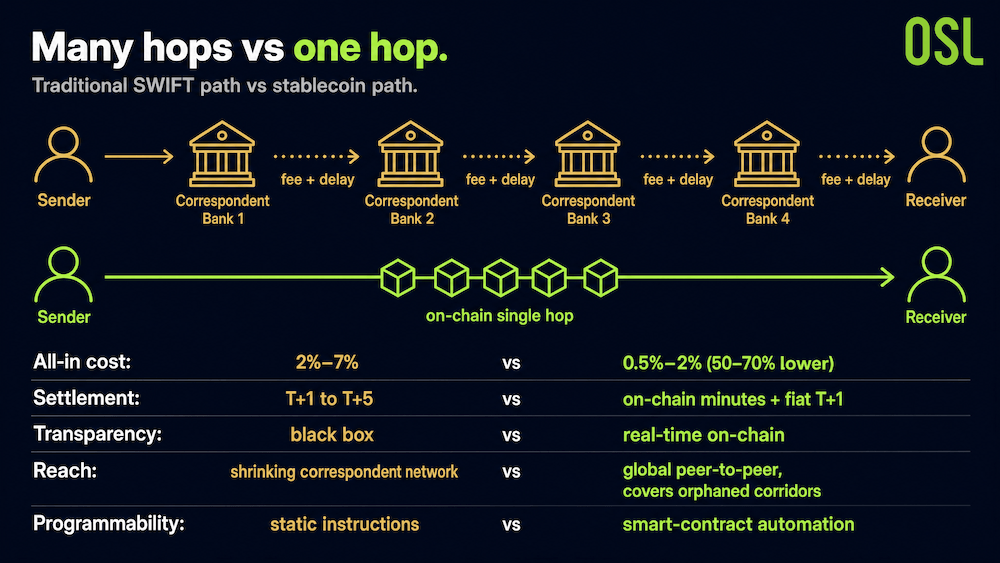

The realistic 2026 picture is two rails running in parallel, with treasury teams choosing per corridor rather than switching wholesale. Stablecoins win where the existing route is slow, expensive, opaque, or dependent on many intermediaries. Where they do win, the gap is large: the report puts all-in costs at 0.5%–2% on the stablecoin path versus 2%–7% on traditional rails, a 50–70% reduction, with settlement compressed from T+1–T+5 to on-chain minutes plus T+1 fiat.

Chart 4: Comparison of Dual-Track Processes: SWIFT Path vs. Stablecoin Path

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

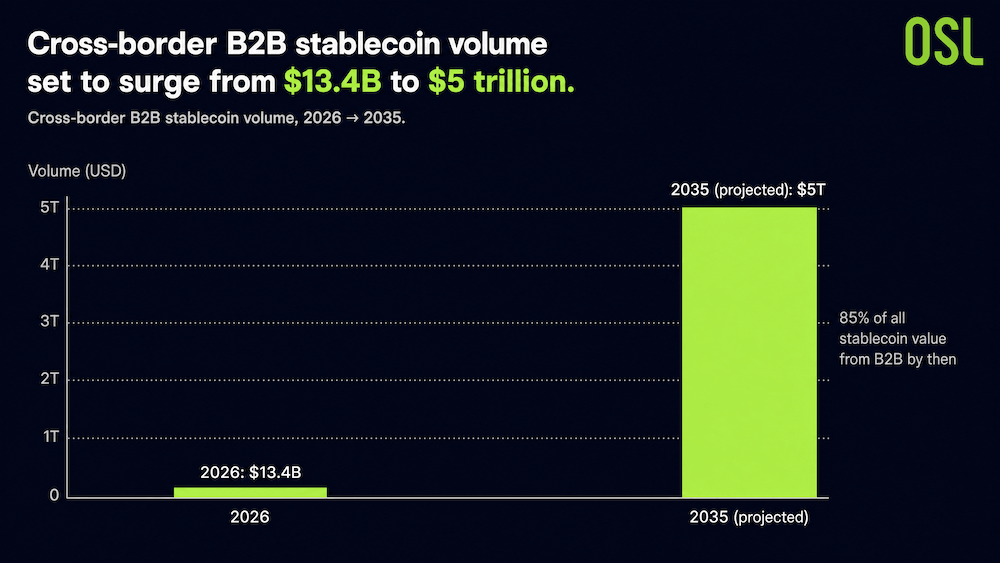

The trajectory, though, is clear. Juniper Research projects cross-border B2B stablecoin volume rising from $13.4 billion in 2026 to $5 trillion by 2035, with 85% of all stablecoin value coming from B2B by then. As Juniper's analyst put it, stablecoins "are not replacing payments infrastructure; they are being adopted where the advantages are most pronounced." For cross-border B2B, those advantages are hard to ignore.

Chart 5: Cross-border B2B stablecoin volume (2026 → 2035)

Source: Juniper Research projects

FAQ

Q1: Does SWIFT move money across borders? A: No. SWIFT is a messaging network that sends payment instructions. The actual money moves through correspondent bank accounts; clearing and settlement happen in systems like CHIPS, CIPS, and Fedwire.

Q2: What is trapped liquidity in cross-border payments? A: Banks pre-fund Nostro/Vostro accounts to enable settlement. BIS estimates roughly $27 trillion sits in these low-yield accounts, a cost ultimately passed to businesses.

Q3: How much cheaper is stablecoin settlement for B2B? A: The report puts all-in costs at 0.5%–2% versus 2%–7% for traditional rails, a 50–70% reduction, with settlement in minutes rather than days.

Q4: Will stablecoins replace SWIFT? A: Not wholesale. The realistic 2026 view is two parallel rails, with treasury teams choosing per corridor. Stablecoins win where legacy routes are slow, costly, or opaque.

References

Note: Industry analysis based on public sources and the cited report. Not investment advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

Explore if stablecoins can lower global remittance costs (currently 6%) and their role in solving financial exclusion in orphaned corridors.

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

Discover how stablecoins restructure B2B payments, reduce costs by 70%, and solve the $27T trapped liquidity issue in the SWIFT network.

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

Explore the three stages of stablecoin evolution: from exchange trading chips and DeFi liquidity to becoming global compliant payment infrastructure.

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Discover how stablecoins address trapped cash, FX risk, and visibility gaps in corporate treasury through quiet pilots and institutional adoption.

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Discover the significance of Bitcoin's 200-week SMA, historical returns, and how to use technical indicators for long-term crypto investing.

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Analyze Bitcoin market structure using on-chain data. Learn why the recent sell-off's realized loss is half of the previous round.

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Recommended for you

More topics

More topics