The Stablecoin Playbook: How Smart Businesses Are Moving Money Faster and Cheaper

By Mauricio Carrillo

Mauricio Carrillo is a fintech executive and crypto strategist with over 15 years of experience leading innovation in digital banking, cross-border payments, and alternative settlement infrastructure.

For fifteen years, the financial industry debated whether crypto would ever be useful in the real world. The noise was deliberate. Bitcoin would replace the dollar. DeFi would dismantle banking. NFTs would reinvent ownership. Most of it didn't happen the way anyone predicted.

What did happen was quieter. A category of digital assets that almost nobody considered revolutionary:

Stablecoins

They became the infrastructure that actually worked.

And they won for an embarrassingly simple reason. People don't care about the technology; they care whether their money arrives when it was supposed to, at the cost they expected.

Source: Chainalysis

Stablecoin Payments: How They Actually Work

"It is worse than tulip bulbs." Said JPMorgan CEO Jamie Dimon in 2017. He called Bitcoin a fraud. Said it was only useful for drug dealers and people in North Korea.

Eight years later, JPMorgan's blockchain division, Kinexys, processes billions in daily transaction volume, with cumulative activity exceeding $3 trillion since 2019. JPM Coin runs on Coinbase's Base network. Clients include Mastercard and BMW.

What changed? Not the technology, but the acknowledgment that it worked.

A stablecoin is a digital asset pegged to a stable reference value — almost always the US dollar. One USDT equals one dollar. One USDC equals one dollar. That peg separates stablecoins from speculative crypto, making them practical for commerce.

When a business sends a stablecoin payment, the wallet broadcasts directly to a blockchain network — Ethereum, Solana, TRON, or Polygon. Validators confirm it. Payment becomes final. No clearing house. No correspondent bank chain. No T+2 cycle.

Stripe explains it in its own documentation: "Stablecoin transactions cannot be cancelled, modified, or reversed once submitted."

For merchants, that finality is not a limitation. It is the entire point.

The technical stack — wallet connectivity, blockchain settlement, smart contract execution, compliance integration — is programmable at every layer. The architecture, called the stablecoin sandwich, converts fiat at the sending end, settles in seconds, and converts back to local currency at the destination. Stripe, Visa, and Mastercard are all building around it.

Sources: Bankrate, Stripe, Stripe legal

Solving the Pain Points Nobody Talks About Honestly

Zero Chargebacks

Chargeback management used to consume a disproportionate amount of operational attention. Dispute windows, evidence gathering, win rates, and financial disruptions. A whole workflow dedicated to recovering revenue that should never have been contested.

When the settlement stage becomes final by design, that entire category disappears. It is not about cutting a significant portion of the fraud; it disappears.

"Stablecoin Payments does not support Disputes," as every platform's legal department makes clear. For e-commerce platforms handling digital goods, subscriptions, and cross-border transactions — where friendly fraud is highest — this finality eliminates a cost center most operators simply accepted as inevitable.

Predictability Over Speed

It might sound obvious, but for a business, predictability is more important than quickness.

When businesses move corridors onto stablecoin rails, the first thing counterparties notice is not the speed. It is the consistency. Treasury teams managing international flows can plan, commit to suppliers, and price with certainty — because settlement arrives when it is supposed to, every time. They no longer depend on middlemen or independent parties operating on their own schedules.

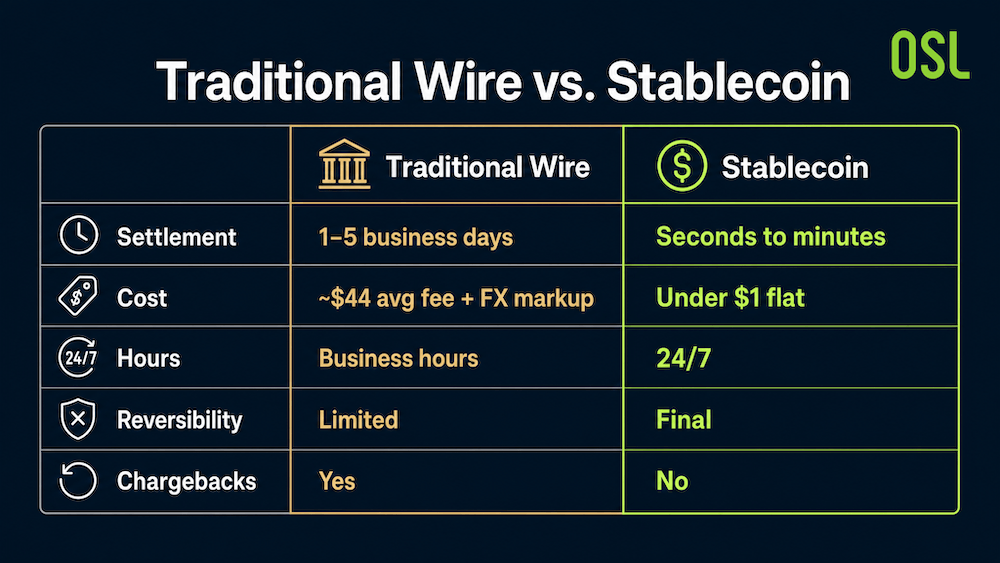

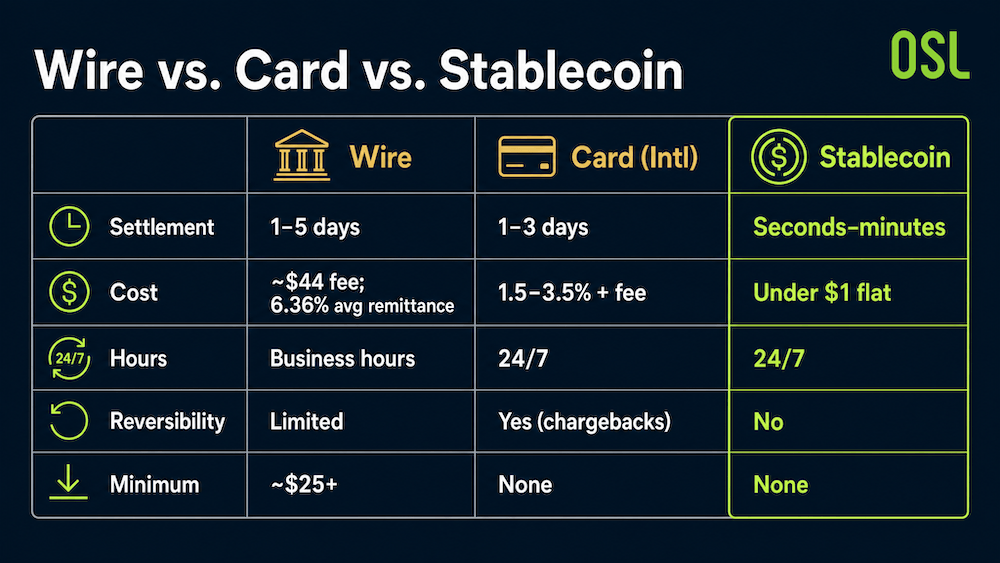

The EY-Parthenon survey of 350 executives found 41% of current stablecoin users report cost reductions of at least 10% in cross-border B2B payments. On a $50 million program, that is $5 million annually. Traditional remittance fees average above 6% globally. When Paxos settled $1.3 billion in stablecoin volume on Polygon, the total gas cost across all 82,000+ transactions was under $700, according to the Polygon enterprise guide.

The contrast is sharpest at the small end. On a $2 million cross-border payment, a wire can quietly lose $47 in fees plus an unitemized FX markup of around 3% — costs that compound on every transaction. For high-frequency, lower-value flows like contractor payroll, that math makes traditional rails almost unworkable, which is why platforms handling global gig and contractor payments like Deel are moving these flows onto stablecoin infrastructure.

Sources: World Bank, Bankrate, Stripe

Stablecoin Payments: Trust Is Earned Before It Is Scaled

The payment industry has a graveyard of companies that processed millions one quarter and were unreachable the next. The volume grows quickly on fragile infrastructure with compliance gaps nobody addressed until someone else forced the question. That’s a recipe for disaster, leaving clients’ transactions in limbo.

Trust is paramount in this industry, but it is not built on promises or on impressive partner lists with claims of global coverage.

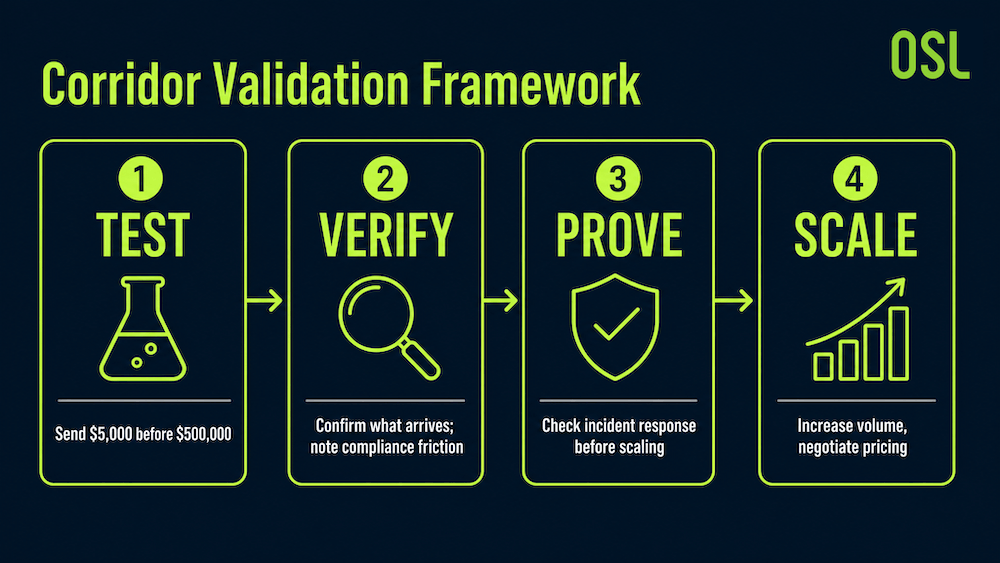

My recommendation is always the same: Start small on every project or operation.

Send $5,000 before $500,000. Verify what arrives and note the compliance friction at each step. Check whether an incident response was implemented, and scale only once the channel has proven itself.

Rushing that process is how companies end up with six-figure transactions in compliance holds that they could have identified with a small-dollar test.

Stablecoin infrastructure offers something correspondent banking never could: transparency by design. Reserve attestations are published. Smart contracts are audited, publicly verifiable, and traceable. In addition, transaction history is immutable.

The evidence needed to evaluate a partner is available before you move the first dollar — not after something goes wrong.

The questions worth asking are straightforward:

Who audits the reserves, and how often?

What licenses do you hold?

What is the regulatory standing in the jurisdictions where you operate?

What does the smart contract audit history look like?

What happens to client funds if the platform experiences a security event?

These questions have public and verifiable answers. That transparency is one of the most underappreciated advantages of stablecoins over legacy financial infrastructure.

The infrastructure worth building on demonstrates this openly. The infrastructure that resists these questions usually has a reason.

The Holy Grail: Global Rails, Local Understanding

Stablecoins solve the middle mile brilliantly. The challenge lies at the endpoints — and in the minds of the people using them.

A Mexican agricultural exporter paying suppliers in Hong Kong while collecting payments across Sub-Saharan Africa navigates three currency zones, three regulatory frameworks, and supply chain finance flowing in multiple directions simultaneously. The stablecoin layer makes this manageable. Without it, the correspondent banking costs make the business model challenging.

A real estate investor in Dubai who converts $150,000 monthly between stablecoins and AED — receiving rental income, disbursing salaries, paying suppliers, and managing treasury across currencies — does so today through VARA-licensed infrastructure. Not a risky pilot, but an operational channel.

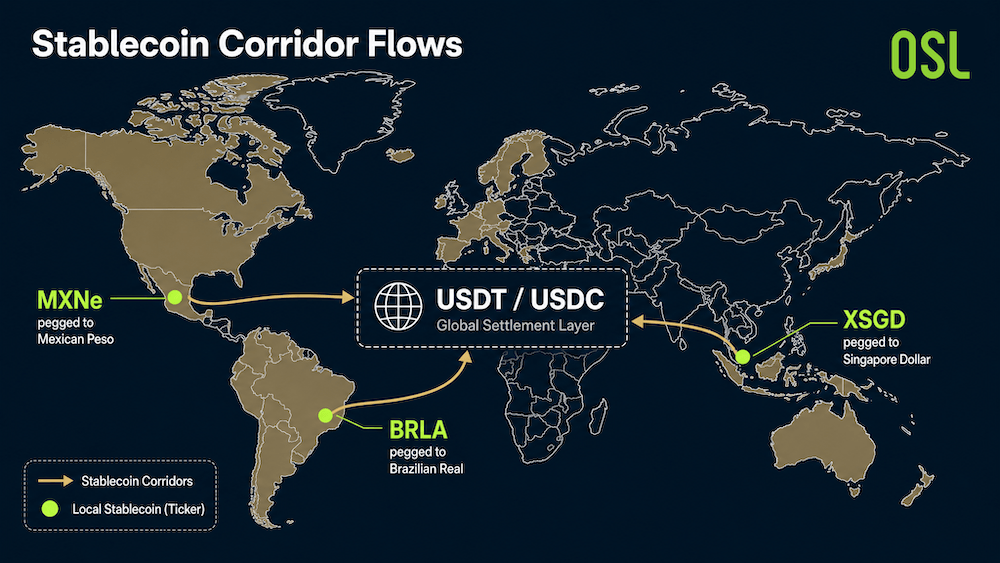

The most efficient corridor architecture uses local stablecoins to eliminate unnecessary conversion steps. Converting Mexican pesos to USD, then to USDT, then to Brazilian reais means paying the FX spread twice. BRLA for Brazil. MXNe for Mexico. XSGD for Singapore. Direct corridor. No double spread.

But local stablecoins solve more than just cost efficiency. They solve an adoption problem.

The fastest path to stablecoin adoption in emerging markets is not explaining what USDT is. It is giving a merchant in Nairobi a digital shilling — an instrument that behaves exactly like the currency they have used their entire life, but settles instantly and connects to the global network transparently. When the instrument feels familiar, the learning curve collapses.

That is when stablecoins stop being a crypto product and start being money.

Source: Polygon Technology

The Cash Problem Nobody Has Solved

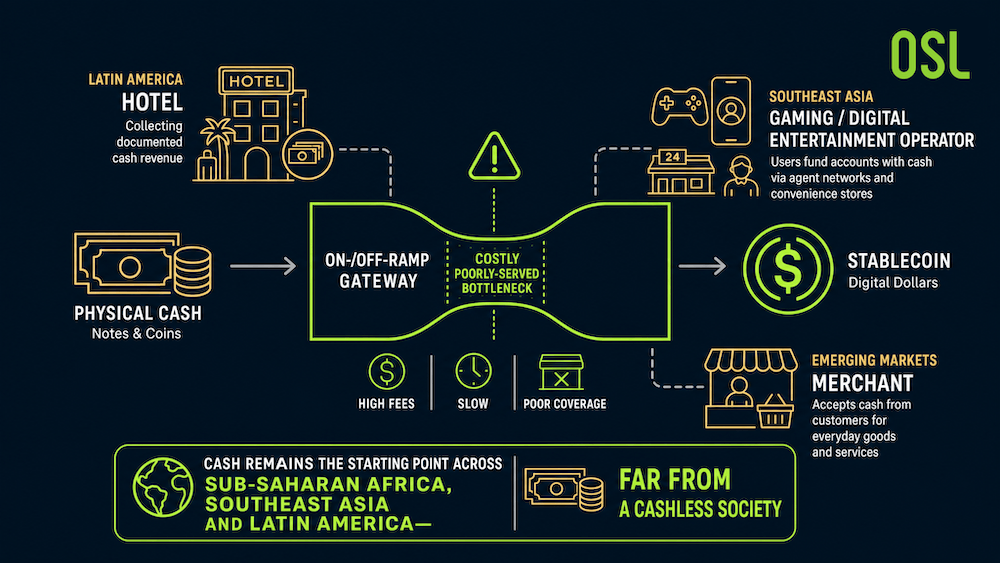

The stablecoin conversation almost always assumes a bank account at both ends, but we are still far from a cashless society.

For a significant share of global commerce — across Sub-Saharan Africa, Southeast Asia, and Latin America — the starting point is cash.

Hotels across Latin America collect legitimate operational revenues in cash — clean, documented, tax-compliant. Their challenge is that on- and off-ramp infrastructure for converting operational cash into stablecoins is expensive and poorly served. They are penalized simply for operating in cash-heavy economies.

Gaming and digital entertainment operators across Southeast Asia settle platform revenues in USDT and USDC through licensed VASPs — but their end users fund their accounts with cash via agent networks and convenience stores.

Solving cash-on- and off-ramps is arguably the most important unresolved challenge in stablecoin payments. The companies that solve this compliantly will not just win a payment contract. They will define a category.

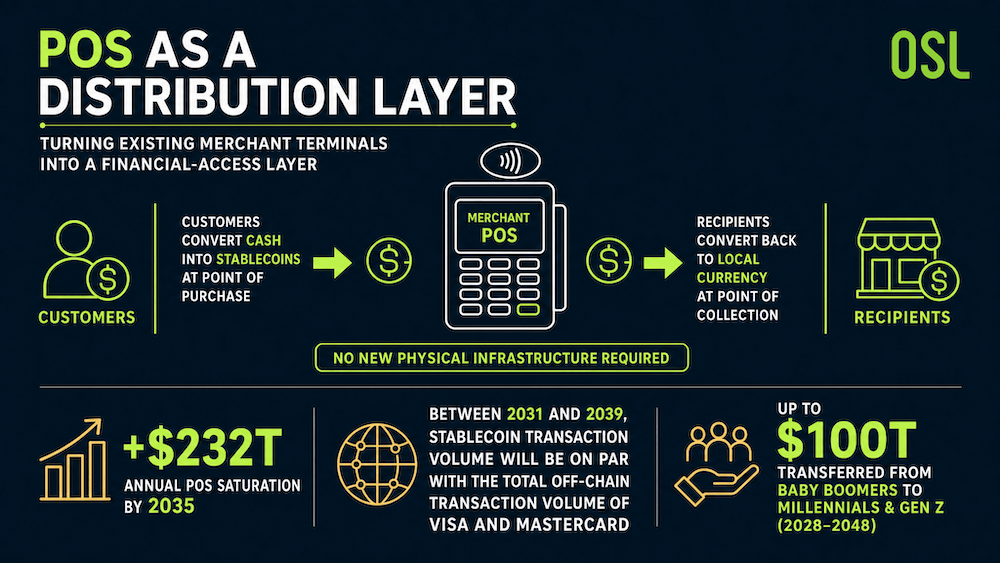

Point-of-Sale: Not Just Payments — Distribution

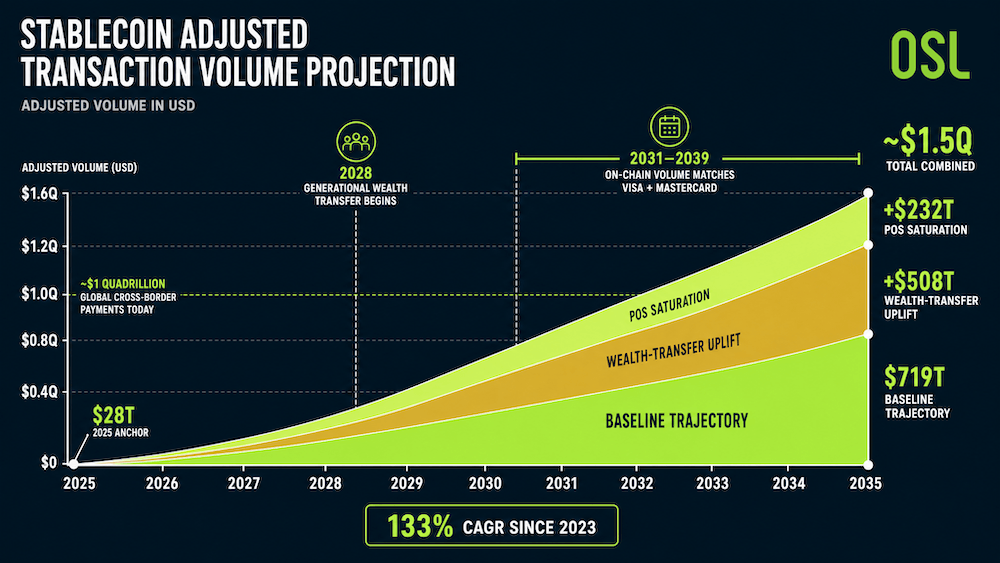

Chainalysis projects stablecoin volumes reaching parity with Visa and Mastercard's combined off-chain transactions between 2031 and 2039. Point-of-sale saturation alone could add $232 trillion annually to stablecoin volumes by 2035.

In markets where bank branches are scarce, but merchant terminals are ubiquitous, stablecoin-enabled POS transforms existing infrastructure into a distributed financial access layer — where customers convert cash into stablecoins at the point of purchase and recipients convert them back to local currency at the point of collection — no new physical infrastructure required.

This is not merely about payments. It is distribution.

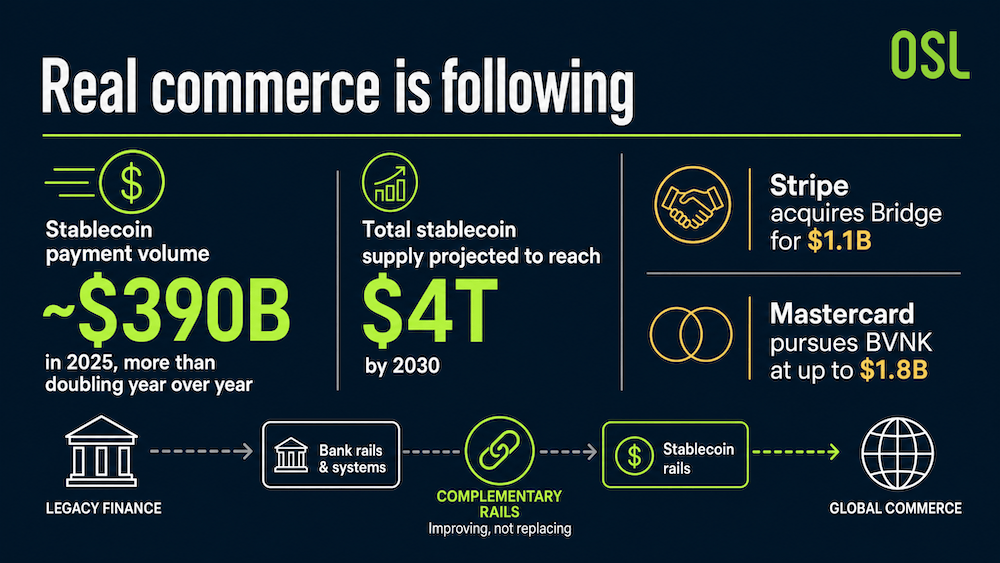

Between 2028 and 2048, Merrill Lynch estimates up to $100 trillion in transfers from Baby Boomers to Millennials and Gen Z — generations in which nearly half have held cryptocurrency. Stripe's acquisition of Bridge for $1.1 billion and Mastercard's pursuit of BVNK at up to $1.8 billion confirm institutional conviction.

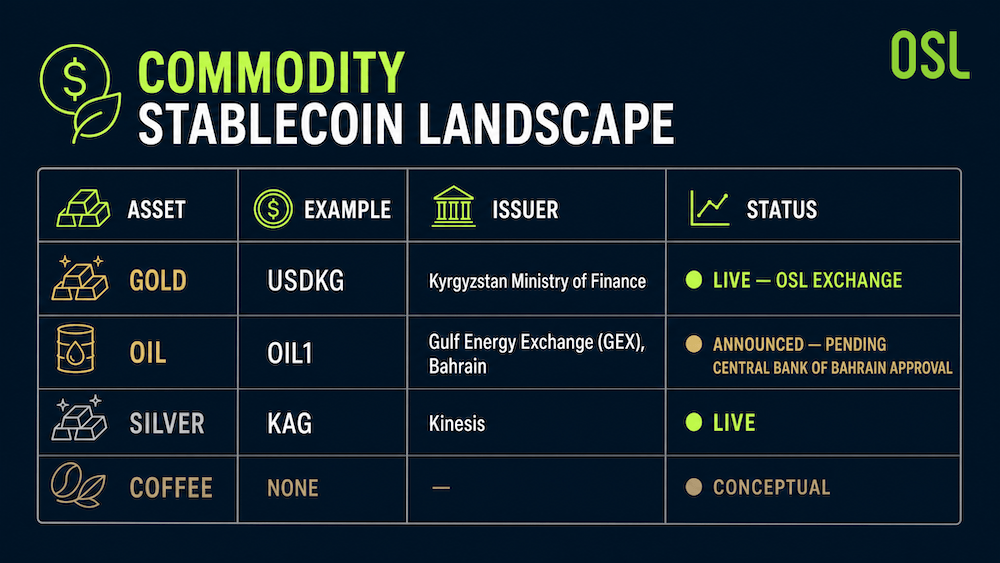

Beyond the Dollar: The Commodity Frontier

USDKG — gold-backed, issued by Kyrgyzstan's Ministry of Finance, audited by ConsenSys Diligence, listed on OSL's licensed Hong Kong exchange — is the opening chapter of a much larger story.

Gold is the obvious first commodity. The design principles extend further.

A coffee cooperative in Colombia faces a brutal combination: local currency depreciation erodes the value of future payments, while commodity price volatility creates revenue uncertainty.

A coffee-backed stablecoin turns that vulnerability into a hedge — payment and price protection in a single instrument, accessible to producers and investors who have never had access to derivatives markets.

Importers and exporters navigating markets with evolving regulatory frameworks — India being the most significant, where cross-border infrastructure is being actively redefined under RBI oversight — find dollar-pegged instruments carry additional conversion costs and regulatory friction. A commodity-backed instrument denominated in something they trade daily removes that layer.

The question is not whether commodity-backed stablecoins will exist at scale. It is which platforms will define the category.

Sources: FXStreet, GEX, Kinesis

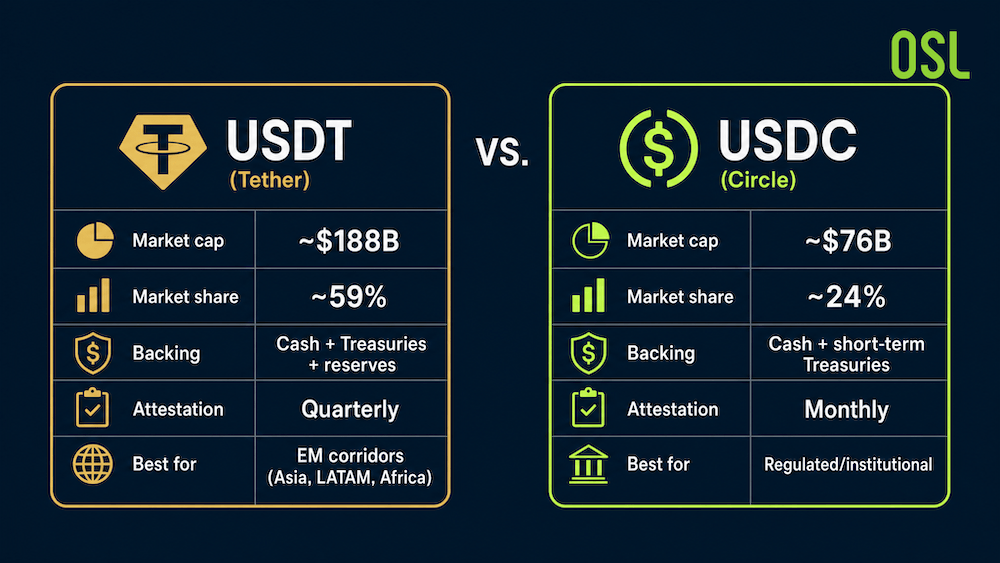

Choosing the Right Asset: USDC vs USDT

USDT and USDC hold approximately 83% of the total stablecoin market share. The choice is strategic rather than technical.

USDT — Tether: Largest by market cap and volume. Dominates emerging market corridors across Asia, Latin America, and Africa. Unmatched liquidity depth in high-growth markets.

USDC — Circle: Monthly attestations by Deloitte. Full backing by cash and short-term US Treasuries. GENIUS Act compliant. For regulated markets and institutional counterparties, USDC reduces counterparty risk and simplifies audit documentation.

The strategic question is not USDC or USDT. It is which instruments cover your specific corridors with the lowest friction and the highest compliance certainty — and whether dollar-pegged instruments are even the right starting point.

Every corridor has its own regulatory profile. Singapore's MAS, EU MiCA, US FinCEN, and the UAE's VARA — these don't harmonize neatly. The right question to ask any infrastructure partner is not how many countries they cover. It is whether they can show you compliance documentation for your specific corridor.

Sources: CoinMarketCap, Circle

The Infrastructure Is Already Here

There is a misconception worth addressing directly. Cryptocurrencies and stablecoins are not here to replace the legacy financial system. They are here to improve it.

Faster settlement, lower costs, greater transparency, and unmodifiable history are the added value, but they should come with the safety net that institutional infrastructure provides — regulatory oversight, reserve accountability, and client protection frameworks that legacy finance developed over decades for good reason.

The stablecoin platforms worth building on understand this. They operate within the traditional system — holding licenses where required, publishing reserve audits where expected, and maintaining standards that satisfy both a crypto-native operator and a traditional compliance officer.

Accountability in this industry attaches to institutions, to licenses, to published audit records — and to the people who sign off on them. The key players who will still be operating in ten years are those who answer questions openly, consistently maintain high standards, and protect both the structure and the clients who depend on it.

That combination is rare. When you find it, it is worth building on.

Real commerce is following. Stablecoin payment volume — actual commercial activity, stripped of trading and bot noise — reached roughly $390 billion in 2025, more than doubling year over year (McKinsey/Artemis Analytics). Bitwise and Citi both project total stablecoin supply climbing to $4 trillion by 2030.

For e-commerce operators: find your friendliest corridor and test small. Once the channel is proven, scale from evidence.

For marketplace platforms: your international sellers want faster, cheaper payouts. The question is whether your infrastructure can deliver without the margin degradation that correspondent banking imposes at scale.

For gig economy platforms, in many emerging-market corridors, stablecoins are not an alternative. They are the only infrastructure that makes the economics work efficiently. Try it.

Usually, low volume entails higher fees, but starting small is paramount when testing corridors. Once everything is proven and the corridor is trusted, increase volume and negotiate prices. Stablecoin channels will welcome you. Build trust before you build volume.

Remember, stablecoins are the ultimate form of crypto adoption. The infrastructure is already here.

More topics

More topics

Latest

How Businesses Can Manage Stablecoin Settlement Risk in Corporate Payments?

Businesses can reduce stablecoin settlement risk by treating settlement as a controlled workflow, not only as a token transfer. They should review the stablecoin issuer, reserves, redemption terms, counterparties,...

How Businesses Can Manage Stablecoin Settlement Risk in Corporate Payments?

What Makes a Stablecoin Institutional Grade?

A stablecoin may be considered institutional grade when enterprises can review its issuer, reserve transparency, governance, redemption assumptions, compliance controls, operational workflow and reporting evidence....

What Makes a Stablecoin Institutional Grade?

What Compliance Teams Should Review Before Using USDGO for Payments and Settlement?

Compliance teams should ask about USDGO's issuer, reserves, attestations, redemption assumptions, eligible users, supported routes, jurisdictions, onboarding, screening, recordkeeping, reporting, fees and exception...

What Compliance Teams Should Review Before Using USDGO for Payments and Settlement?

How Corporate Boards Can Review Stablecoin Risk Controls for Payments and Settlement?

To explain stablecoin risk controls to a corporate board, management should separate the asset, service route, counterparties, controls and reporting model. The board should see issuer and reserve review, eligibility...

How Corporate Boards Can Review Stablecoin Risk Controls for Payments and Settlement?

Why Stablecoin Compliance Matters for Corporate Payment Workflows?

Stablecoin compliance matters for corporate payments because payment teams must confirm the asset, counterparty, route, jurisdiction, approval process, screening, records and reconciliation controls before value...

Why Stablecoin Compliance Matters for Corporate Payment Workflows?

How Can Stablecoin Settlement Support Import and Export Businesses?

Stablecoin settlement can give importers and exporters an additional route for agreed cross-border trade obligations. A workable route begins with the sales contract and invoice: the parties must define the amount,...

How Can Stablecoin Settlement Support Import and Export Businesses?

Recommended for you

More topics

More topics