The Ultimate Guide to B2B Stablecoin Settlement: Bypassing Legacy Rails in 2026

Written by Jinia Shawdagor

If you’re still treating stablecoins mainly as crypto market tools, you’re missing the bigger story. Recent institutional activity has made stablecoin settlement hard to ignore, including a UAE-backed dirham stablecoin that processed a $30 million institutional transaction in May this year.

Companies running B2B cross-border payments care about faster settlement, lower intermediary costs, and better visibility over funds in transit, and that’s where stablecoin settlement fits, because it can move fiat-backed value across blockchain networks in minutes while many business payments still pass through long correspondent bank chains, where each intermediary adds cost, delay, and uncertainty.

That doesn’t mean stablecoins are replacing the banking system. Banks still control the parts of the payment stack that matter most, from fiat access and credit through to custody, compliance, local payout, and liquidity management, and SWIFT remains central to global bank messaging while it develops digital-ledger infrastructure of its own. The more realistic view is that stablecoin settlement is becoming a parallel rail for the flows where the existing route is slow, expensive, hard to track, or dependent on several intermediaries.

For multinational treasury teams, the question worth asking is where that rail can cut real cost, release trapped liquidity, and improve payment control without adding risks the business can’t justify.

What stablecoin settlement actually changes

A SWIFT-based payment usually runs on a T+2 timeline, so a payment sent on a Monday, for example, usually clears by Wednesday if nothing trips along the way.

It takes that long because of the correspondent bank chain sitting in the middle, where a series of intermediary banks each take a fee and add a delay before the money reaches the other side. For a business sending supplier payments abroad at any real frequency, that adds up to capital tied up in transit, FX exposure while the payment floats, and reconciliation work on both ends.

On-chain settlement shortens that window to minutes, because the payment becomes final the moment the block confirms and both parties read the same record without a correspondent markup buried inside it. USDT and USDC can hold their value through all of this since each one is pegged to the US dollar and backed by fiat-backed reserves held with licensed custodians, which is why a supplier in Vietnam can invoice in USDC and trust the dollar value won’t drift between the invoice date and the day they’re paid.

The FX claim is the part most coverage gets wrong, because a dollar stablecoin doesn’t remove currency risk so much as hand the timing of it to the receiver. The sender skips the correspondent fees and the unpredictable spreads, while the receiver still has to convert into local currency at some point, only now they get to choose when. For a treasury team weighing this up, that control over timing is often worth more than the minutes saved on settlement.

Correspondent banking | On-chain stablecoin settlement | |

|---|---|---|

Settlement time | T+2 (typically two business days) | Minutes, once the block confirms |

Intermediaries | A chain of correspondent banks, each adding a step | None between sender and receiver |

Operating hours | Bank hours, weekdays, subject to cut-offs and holidays | 24 hours, 7 days, including weekends |

Finality | Revocable until fully cleared | Final once the block confirms |

FX timing | Set by the corridor and its banks | Receiver chooses when to convert to local currency |

Fees | Markup taken at each intermediary, not always visible upfront | Network fee only, visible before sending |

Shared record | Each bank keeps its own ledger; reconciliation on both ends | Both parties read the same on-chain record |

The local-currency turn

The development worth watching most closely through 2026 gets very little attention, and it’s the rise of stablecoins pegged to currencies other than the dollar.

The DDSC transaction is the clearest example so far, since a dirham-pegged token settling a UAE corridor means neither side has to touch the dollar at all. With USDC or USDT, a euro-to-dirham payment still makes two dollar round-trips and picks up FX cost on each leg, whereas a local-currency stablecoin removes that round-trip entirely.

As euro tokens and other regional issuers come through under their own regulatory regimes, the corridor maths shifts away from “dollars, faster” and towards settling in whatever currency the corridor actually runs on.

The UAE move carries weight for that reason. DDSC came out of a partnership between International Holding Company, First Abu Dhabi Bank, and Sirius International Holding, and it was built for institutional payments, treasury operations, and trade settlement. When a bank that size sits behind a national-currency stablecoin, the question for treasury teams moves from whether the infrastructure is ready to which corridors it already covers.

Where the treasury case is real

The treasury case depends heavily on the corridor. It’s strongest on routes into high-FX-friction markets like Nigeria, Indonesia, and Argentina, where conversion fees, thin correspondent banking relationships, limited local liquidity, and settlement delays all stack on top of each other, and it’s weakest wherever banks already move money cheaply and quickly.

Where the local currency is volatile, the T+2 float can eat the margin on a supplier payment before it even arrives, so settling in a stablecoin lets the receiving business hold a dollar-equivalent asset and convert locally when the rate suits them. Faster and more predictable payment also makes a buyer a better counterparty, which tends to show up later in supplier negotiations and the payment terms a business can ask for.

The liquidity argument sits alongside this, because SWIFT doesn’t settle on weekends, and bank cut-offs, public holidays, and time-zone gaps mean capital can sit idle at exactly the moments a business needs it.

On-chain settlement, on the other hand, has no cut-off window, so a transfer clears at 3am on a Sunday the same way it does midweek, and that changes how a team thinks about working capital. A team that trusts the timing can hold smaller cash buffers and move money more precisely, instead of parking large balances just to absorb settlement lag.

That same shift in trust runs into a familiar obstacle on integration, where adoption often stalls on a wrong assumption, because treasury teams expect a stablecoin rail to mean rebuilding their stack when it rarely does. The main providers run through APIs that connect into SAP, Oracle, and NetSuite, with an orchestration layer handling wallets, network routing, gas fees, and confirmation behind the scenes, while settlement data feeds back into the ERP for reconciliation like any bank statement. In practice, going live looks like a normal treasury-technology project, with vendor selection, an integration sprint, and compliance sign-off, and the demand numbers back that up. Stripe, for one, reported its stablecoin payments volume doubled to around $400 billion in 2025, roughly 60% of it B2B, while volume on its Bridge platform more than quadrupled.

Source: Chainalysis, Visa, annual report

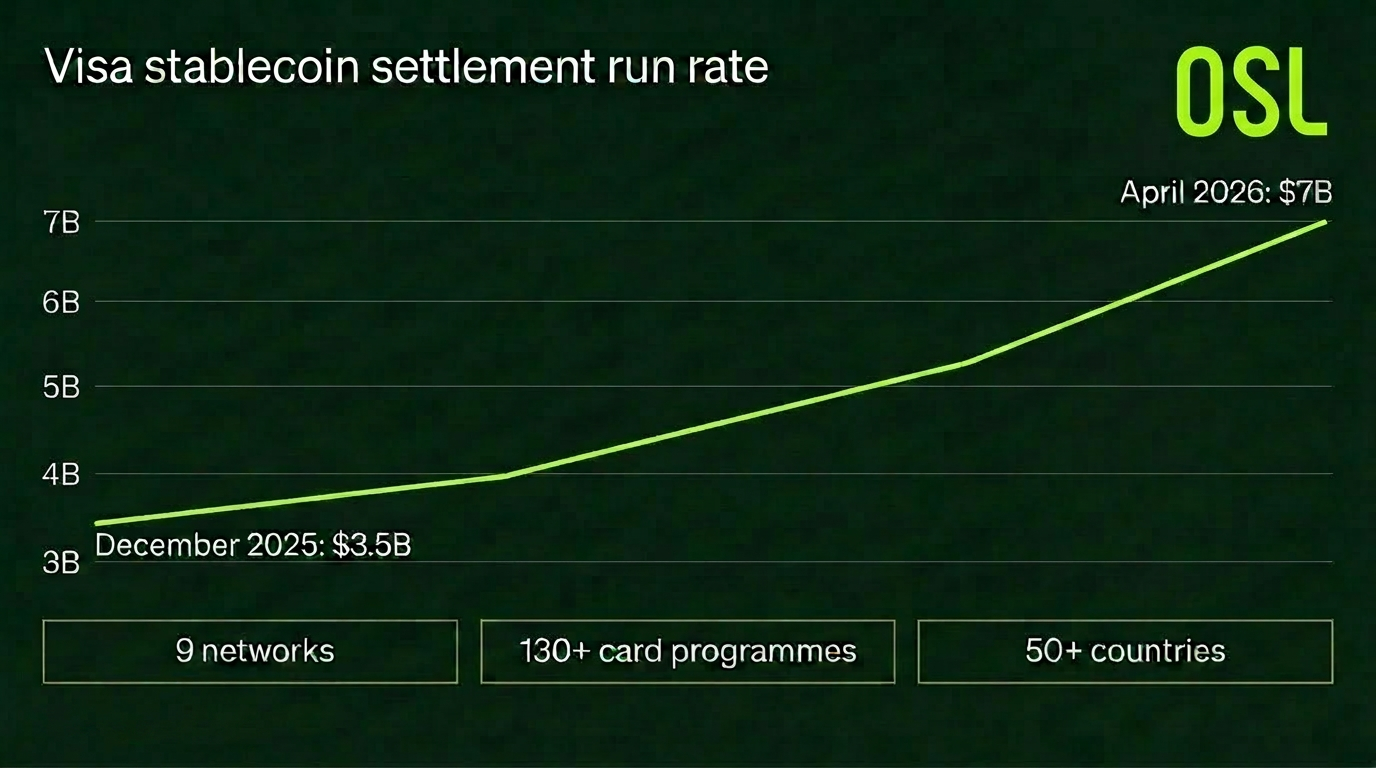

What the multi-chain pilots are really telling treasury teams

Visa’s pilot tends to get quoted as proof that the technology has matured, though it points to something simpler. The settlement pilot now spans nine blockchains and has reached a $7 billion annualised run rate, up 50% on the prior quarter and double its December 2025 level, and the fact that it takes nine networks to get there suggests the market is still scattered across chains rather than settled on a few.

A finance team may not need to be an expert in any of them, and most might have little interest in managing nine chains by hand. What they may want is one interface, with the routing happening underneath, so each payment lands on whichever network suits that corridor on cost, speed, and compliance. Visa operating across Ethereum, Solana, Base, Polygon, Arc, and the rest is really Visa taking that complexity on, so its partners don’t have to, and the practical takeaway for a treasury team may be to choose the vendor whose system does the routing, since the individual chain is likely to matter far less than the vendor pitch suggests.

Source: Visa, April 2026.

The compliance question has moved

A year ago, the question was whether any of this was even allowed, and that is mostly answered now, which changes what diligence has to look at.

In the US, the GENIUS Act is law, signed on 18 July 2025, and it sets federal licensing and reserve rules for payment stablecoin issuers. It isn’t fully in force yet, since it takes effect the earlier of 18 months after enactment or 120 days after regulators publish their final rules, so through 2026, the framework exists while the detailed rulemaking gets written, which means that for US enterprises, legality is no longer the blocker and issuer quality is what diligence now turns on.

In the EU, MiCA regulation remains the most developed framework and the one that matters for any business transacting with EU counterparties, because it requires stablecoin issuers operating in the EU to hold an e-money institution licence and keep fiat-backed reserves with licensed custodians. Circle has pursued MiCA compliance for USDC, while Tether’s USDT has faced more scrutiny over reserve transparency, and several EU venues have treated the two differently, so for EU-facing settlement, an issuer that isn’t MiCA-compliant doesn’t really make the shortlist.

That’s why the buying process now turns on counterparty diligence rather than waiting for a law to land. The FXC Intelligence cross-border buyer’s guide sets out the criteria worth applying, which include custody arrangements, whether reserves are independently audited, API uptime and SLA terms, how failed settlements get handled operationally, and the KYC and AML checks applied to counterparties. Brand recognition is a weak filter this early, since two issuers can both be well known while carrying very different reserve and disclosure profiles.

Where banks still hold the rail

None of this works without banks, because the fiat on-ramps and off-ramps, the credit lines, custody at scale, local payout networks, and the compliance perimeter all still sit with them, and a stablecoin rail that can’t connect cleanly to a bank at each end is a closed loop.

SWIFT isn’t standing still either, since it’s been building ledger infrastructure of its own, so the realistic picture for 2026 is two rails running in parallel, with treasury teams choosing per corridor rather than switching across wholesale.

The move for a treasury leader is a sequencing decision more than a platform one. It starts with mapping the highest-cost corridors by currency, destination, and by where settlement delay does the most damage, while running diligence on two or three providers against the criteria above.

From there, a contained pilot on one corridor with a willing supplier or subsidiary, with the success metrics agreed upfront, will say more than any outside report, because the settlement time against the legacy route, the all-in cost per transaction, and the reconciliation effort are what move internal sign-off. The correspondent bank chain still handles most of what it always did. The teams worth watching are the ones already running a live pilot on the corridors where it costs them most, because they’re building the internal numbers everyone else will be asking for in a year.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

How Businesses Can Manage Stablecoin Settlement Risk in Corporate Payments?

Businesses can reduce stablecoin settlement risk by treating settlement as a controlled workflow, not only as a token transfer. They should review the stablecoin issuer, reserves, redemption terms, counterparties,...

How Businesses Can Manage Stablecoin Settlement Risk in Corporate Payments?

What Makes a Stablecoin Institutional Grade?

A stablecoin may be considered institutional grade when enterprises can review its issuer, reserve transparency, governance, redemption assumptions, compliance controls, operational workflow and reporting evidence....

What Makes a Stablecoin Institutional Grade?

What Compliance Teams Should Review Before Using USDGO for Payments and Settlement?

Compliance teams should ask about USDGO's issuer, reserves, attestations, redemption assumptions, eligible users, supported routes, jurisdictions, onboarding, screening, recordkeeping, reporting, fees and exception...

What Compliance Teams Should Review Before Using USDGO for Payments and Settlement?

How Corporate Boards Can Review Stablecoin Risk Controls for Payments and Settlement?

To explain stablecoin risk controls to a corporate board, management should separate the asset, service route, counterparties, controls and reporting model. The board should see issuer and reserve review, eligibility...

How Corporate Boards Can Review Stablecoin Risk Controls for Payments and Settlement?

Why Stablecoin Compliance Matters for Corporate Payment Workflows?

Stablecoin compliance matters for corporate payments because payment teams must confirm the asset, counterparty, route, jurisdiction, approval process, screening, records and reconciliation controls before value...

Why Stablecoin Compliance Matters for Corporate Payment Workflows?

How Can Stablecoin Settlement Support Import and Export Businesses?

Stablecoin settlement can give importers and exporters an additional route for agreed cross-border trade obligations. A workable route begins with the sales contract and invoice: the parties must define the amount,...

How Can Stablecoin Settlement Support Import and Export Businesses?

Recommended for you

More topics

More topics