Crypto Market on the Eve of Rate Cut Bets: Liquidity Squeeze Amid Sustained ETF Outflows

Weekly Market Update (Dec 8 - Dec 14, 2025)

The second week of December saw continued capital outflows from BTC spot ETFs, according to publicly available net flow data, indicating that institutional appetites remain subdued.

Meanwhile, aggregate stablecoin supply, as tracked by DeFiLlama, remained broadly unchanged, suggesting that large-scale stablecoin-issued liquidity has not yet returned to the market.

At a chain-specific level, several stablecoin pools on smaller or mid-size chains showed moderate reductions, hinting at localized liquidity rotations or withdrawals.

Given the outflows from major spot ETFs and the stagnant supply of stablecoins, liquidity conditions remain tight, particularly for large-cap and high-beta assets. Order-book depth remains shallow and volatility skew remains elevated across derivatives and options, leading to a cautious market stance.

Protocol-level DeFi flows have not shown reliable signs of renewed capital inflows, reinforcing a risk-off sentiment among institutional participants.With institutional demand muted and liquidity tight, crypto is now behaving more like a yield-sensitive asset than a growth-driven speculative asset — and price action is being driven less by new money and more by portfolio rotation and risk repricing.

Key Market Review — Flows, Positioning & Institutional Behavior

Market Breadth: Narrow, Fragile & Flow-Driven

Market conditions this week remain fragile as liquidity across major venues thinned and price action became increasingly dictated by ETF redemptions and the contraction in stablecoin liquidity. Bitcoin struggled to regain momentum above the low-US$90,000 range, with occasional dips into the mid-US$80,000s exposing how shallow order-book depth had become.

Yet the weakness still did not resemble panic-selling. Instead, it is seen as so institutions are reducing risk gradually, not capitulating. The behaviour reflected the broader macro backdrop with elevated real yields, tight dollar liquidity, and a cautious Fed narrative encouraging de-risking rather than directional positioning.

Source: ETF inflows on DeFillama (https://defillama.com/) as of December 8, 2025.

Likewise, ETF flows reinforce this dynamic. Bitcoin and Ethereum products continued to see overall outflows despite a slower inflow, though at a slower pace than late November's peak redemptions, indicating that the most aggressive phase of deleveraging had eased, even if appetite for renewed accumulation remained absent.

In contrast, Solana ETFs, especially in Asia, again drew incremental inflows, signalling selective rotation toward assets perceived to carry stronger momentum or clearer catalysts. The divergence between majors and SOL illustrated that capital was not exiting crypto entirely but reallocating within the ecosystem toward perceived relative strength.

Across institutional desks, positioning remained defensive. Treasuries and corporations largely paused new accumulation ahead of key macro prints, hedge funds cut gross exposure and leaned into market-neutral strategies, and market makers reduced inventory to avoid holding risk in thin liquidity conditions. While some longer-horizon allocators continued accumulating crypto-linked equities and infrastructure, these flows were insufficient to meaningfully influence market structure.

Until ETF outflows stabilize and stablecoin liquidity begins to rebuild, conviction is likely to remain subdued.

ETF Flows — Rotation Still Intact, Outflows Moderating

Asset | Weekly flow (Dec 8 ‑ 14) |

|---|---|

Bitcoin (BTC) | Net outflows slowed to US$230M–260M, down from late-November capitulation levels. Selling behaviour shifted from panic to controlled position reduction. Long-term holders continued absorbing supply, helping prices stabilize in the high US$80k range. No evidence yet of renewed institutional accumulation. |

Ethereum (ETH) | ETH ETFs recorded US$120M–140M in net outflows. ETH continues to lag with no near-term regulatory or macro catalyst. Capital continues rotating toward SOL, LSTs, and restaking-linked products. December marks ETH’s third straight week of negative ETF flows. |

Solana (SOL) | SOL sustained inflows of US$90M–100M for the week. Remains the top inflow recipient among large caps. ChinaAMC's Solana ETF continued receiving fresh allocations from regional institutions. Inflows reflect intra-crypto rotation, not risk-off conditions. |

Institutional & Treasury Positioning: Reserved, Cautious and Selective

Institutional behaviour remained firmly defensive. Corporate treasuries refrained from expanding digital-asset allocations, preferring to wait for clarity from the U.S. CPI release and the Federal Reserve's December policy meeting. Hedge funds continued to unwind directional longs and shifted toward market-neutral structures as funding costs stayed elevated and liquidity conditions remained thin. Market makers reduced inventory across major pairs, reflecting both widening spreads and the rising cost of capital deployment.

While isolated examples of long-term conviction appeared, such as continued accumulation in crypto-linked equities, these were the exception, not the rule. Broadly, institutions maintained a posture centered on liquidity preservation, not risk accumulation, reinforcing the sense that the market is still in a controlled de-risking phase.

DeFi Overview — TVL Dynamics & Protocol Rotation

DeFi activity mirrored the risk-off tone of the broader crypto market. Total value locked drifted lower across major ecosystems, driven primarily by price depreciation and the unwinding of leverage-dependent strategies. Ethereum maintained its position as the liquidity anchor, though inflows into Aave, Lido, and other core protocols stalled.

Restaking platforms, particularly EigenLayer and ether.fi, remained comparatively resilient as validator incentives continued to attract capital, even while more complex structured-yield strategies experienced diminished participation.

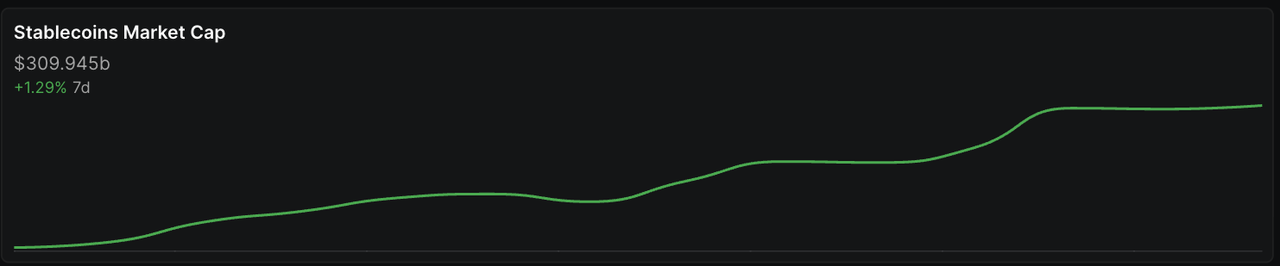

Source: Stablecoins market cap on DeFillama (https://defillama.com/) as of December 8, 2025.

Stablecoin supply showed little expansion during the period despite the all-time high stablecoin supply on Solana, signalling persistent tightness in DeFi's credit layer. The sector remains in a liquidity-led consolidation rather than a structural decline, with capital concentrating on collateral-backed, lower-risk instruments.

Funding Rate Snapshot: Leverage Rebuilding

Funding dynamics reflect leverage rebuilding despite weak spot flows:

Source: https://www.coinglass.com/AccumulatedFundingRate

(The data is based on the last 7 days' funding rate taken snapshot on December 8, 2025)

Asset | Funding Trend | Commentary |

|---|---|---|

BTC | Strongly positive | Long remains crowded. Liquidation risk rises if BTC breaks US$86K. |

ETH | Mildly positive | Cautious leverage rebuild, but still lagging the majors. |

SOL | Highly divergent | A mix of momentum long, hedged positions, which may cascade to elevated volatility. |

XRP/DOGE | Inconsistent | Retail-driven without a clear institutional trend. |

In summary, positive funding with weak spot flows can be translated into a fragile leverage structure.

Outlook for Next Week (16–22 Dec)

Fed & CPI Remain Critical

Dec 11 CPI and Dec 18 FOMC are the dominant macro catalysts.

The upcoming week will be dominated by the U.S. macro events, particularly the Federal Reserve's December meeting and the updated rate projections for 2026. With real yields elevated and liquidity conditions tight, any hawkish tilt from the Fed would reinforce the current derisking cycle, while a softer tone could help stabilize ETF flows and reduce pressure on spot markets.

ETF Flow Stabilization

For now, the balance of risks still favours cautious positioning. Large-cap liquidity remains the preferred allocation venue, and meaningful re-engagement from institutions will likely require both flow stabilization and clearer macro signals.

Stablecoin Supply

Contraction in USDT/USDC remains the largest structural headwind. Return to net minting would signal the earliest turning point for overall crypto liquidity. However, stablecoin supply remains the most important forward-looking indicator for crypto-native liquidity. Without renewed issuance, the market will struggle to sustain meaningful upside.

DeFi-specific catalysts, including restaking expansions and incentive updates across Layer-2 ecosystems, may generate localized rotations but are unlikely to shift broader sentiment without support from ETF flows and macro conditions.

DeFi & Restaking Catalysts

EigenLayer Phase-3 onboarding (Dec 9), Lido operator update (Dec 11), and Arbitrum/Base incentive epochs may spark localized rotation, but macro headwinds limit broader impact.

In general, BTC sits above a dense liquidation band at US$84K–86K. Any break below risks cascading liquidations due to crowded long positioning.

Positioning Summary This Week

Given the current conditions, institutions remain focused on:

BTC, ETH, SOL (liquid majors).

Minimize long-tail or low-liquidity alt exposure.

Prioritize liquidity management and conservative sizing.

Wait for confirmed ETF stablecoin flow reversals before scaling risk.

Patience and disciplined positioning remain on the edge.

Crypto Market Watch: Key Events & Liquidity Drivers (Dec 8–14, 2025)

Macro Events That Matter Most This Week

Event Category | Region Focus | Why It Matters | Dates |

|---|---|---|---|

Central Bank Speeches & Policy Signals | U.S., Global | Multiple Fed speeches ahead of the FOMC may shape expectations for 2026 rate cuts. Any hawkish tone tightens liquidity and pressures risk assets. Fed Interest rate decision and FOMC press conference on Dec 10. | Dec 9–13 |

U.S. CPI Release | U.S. | The most important macro event this week. A hot CPI print lifts real yields → tighter liquidity → crypto downside. A soft print could stabilize ETF flows. | Dec 11 |

Labor Market & Demand Indicators | U.S., Canada | Initial Jobless Claims and Michigan Sentiment offer insight into U.S. demand resilience. Softening data supports dovish expectations. | Dec 12–13 |

China & UK Growth Data | China, UK | China trade balance and credit data shape the global growth outlook; UK GDP signals economic momentum. Weak data reinforces “slow growth + tight policy.” | Dec 10–13 (CN) Dec 12 (UK) |

Source: https://www.investing.com/holiday-calendar/

Crypto-Specific Catalysts to Watch

Catalyst Type | Example Event | Impact | Why It Matters |

|---|---|---|---|

Ethereum Scaling Upgrades | Ethereum “Fusaka” Upgrade (PeerDAS) enters first full operational week | L2 throughput may improve; lower DA costs | Successful implementation supports ETH, L2 tokens, restaking demand |

Major Narrative Conferences | India Blockchain Week Dubai Blockchain Week Solana Breakpoint | Protocol announcements, ecosystem partnerships | Shapes narrative momentum in RWAs, restaking, L2s, DePIN |

Token Unlocks | PYTH (Dec 11), ARB (Dec 14), JTO (post–Dec 7) | Additional supply in thin liquidity → higher volatility | Unlock clusters create local selling pressure and wider funding spreads |

Exchange Microstructure Changes | Binance BTC-margin pair removals (effective Dec 4) | Liquidity migration and repricing in affected alts | May push flows back toward majors, altering perp funding and OI distribution |

Source: https://coinmarketcap.com/events/, coinmarketcal.com

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics