BTC ETF Flows Turn Positive Amid Fragile Liquidity; Stablecoin Growth Remains Uneven

Weekly Market Update (Dec 15 - Dec 21, 2025)

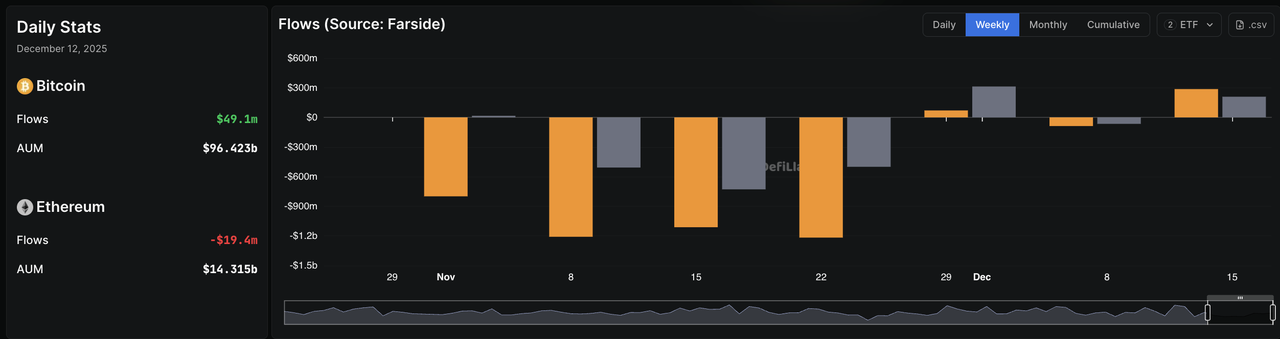

The third week of December (Dec 15–21) is starting with stabilization in institutional flows, rather than continued outflows. The latest completed net flow data (Dec 8–12) shows BTC spot ETFs turned back to net inflows (around US$49.1M on Dec 12), signalling that the heavy redemption pressure seen earlier has eased and that institutional appetite is no longer deteriorating in a straight line.

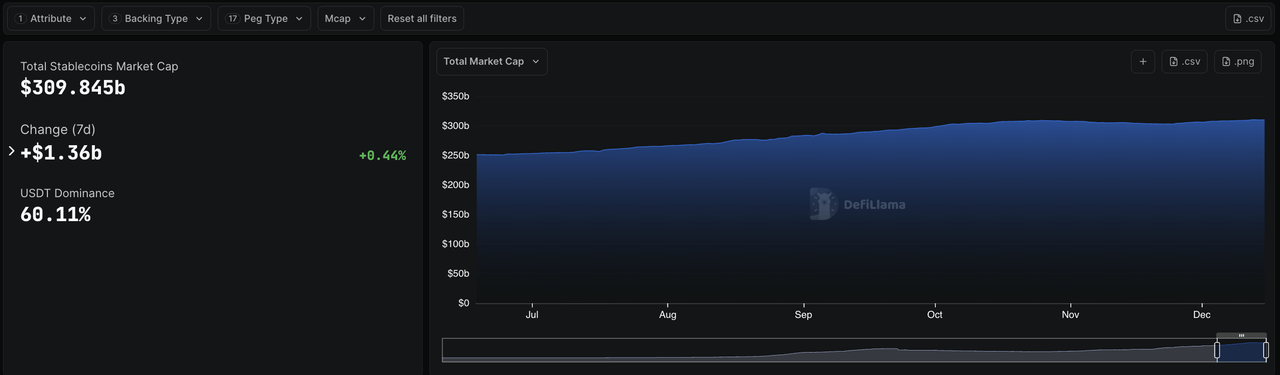

Meanwhile, aggregate stablecoin supply, as tracked by DeFiLlama, is modestly expanding (the total stablecoins ~US$309.94B, +US$1.65B / +0.53% over 7D), indicating that stablecoin-issued liquidity is slowly rebuilding rather than remaining broadly unchanged.

At a chain-specific level, several stablecoin pools on mid-size chains continue to show reductions, consistent with localized liquidity rotations/withdrawals even as the aggregate base grows: Arbitrum -3.90% (7D) and Avalanche -18.05% (7D), while Solana +2.47% (7D) continues to gain liquidity share.

Given the improving ETF flow impulse but uneven stablecoin distribution, liquidity conditions remain fragile rather than “tight across the board”: majors are supported, but order-book depth outside liquid venues remains shallow and volatility skew remains elevated across derivatives/options. Funding remains positive (7D accumulated funding: BTC ~0.0150%, ETH ~0.0029%, SOL ~0.0294%), implying leverage is rebuilding faster than spot depth in parts of the market, which sustains a cautious stance.

With institutional behavior still selective and liquidity still patchy, crypto continues to behave more like a yield/positioning-sensitive asset than a broad speculative "new money" trade — with price action driven more by portfolio rotation and macro-driven risk repricing than uniform inflows.

Key Market Review — Flows, Positioning & Institutional Behavior

Market Breadth: Narrow, Fragile & Flow-Driven

Market conditions this week remain fragile, as liquidity across major venues remains thin, and price action is increasingly dictated by ETF flow direction and the concentration of stablecoin liquidity. The key update compared to the prior framing: the latest completed ETF week (Dec 8–12) shows stabilization, not continued heavy redemptions (BTC net flows turning positive; ETH mixed/softer).

Bitcoin's range behavior still reflects shallow depth (moves occur without panic), but the market tone is better described as controlled repositioning rather than ongoing institutional capitulation.

Source: Bitcoin and Ethereum ETF flows on Farside Investors via Defillama (latest available data as of December 15, 2025).

Likewise, ETF flows reinforce this dynamic. Bitcoin and Ethereum products are no longer in a one-way outflow regime in the latest completed week: BTC improved into net positive territory (Dec 12 +US$49.1M), while ETH flows remain mixed with pockets of inflows earlier in the week but negative on Dec 12.

In contrast, Solana continues to show relative strength on liquidity metrics, with stablecoin supply on Solana still at an all-time high level and +2.47% (7D), supporting ongoing intra-crypto rotation toward perceived momentum/catalysts.

Across institutional desks, positioning remains defensive-to-selective: liquid majors are favored, hedging remains common, and inventory risk is managed tightly given year-end liquidity conditions. Until ETF inflows persist and stablecoin liquidity broadens across chains, conviction is likely to remain measured.

ETF Flows — Rotation Still Intact, Outflows Moderating

Asset | Weekly flow (Dec 15 ‑ 21) |

|---|---|

Bitcoin (BTC) | Outflow narrative replaced by stabilization: latest completed data shows BTC ETF flows back to net positive, with +US$49.1M on Dec 12. Farside Investors Selling pressure looks more like tactical rotation than panic. Still limited evidence of aggressive institutional accumulation, but redemption pressure has eased. |

Ethereum (ETH) | ETH flows remain mixed: strong inflows earlier in the week but net negative on Dec 12 (-US$19.4M). Farside Investors ETH still lags on follow-through; rotation favors higher-momentum pockets. |

Solana (SOL) | Rotation remains constructive on-chain: Solana stablecoins +2.47% (7D). DeFi Llama+1 Momentum positioning remains higher beta: SOL accumulated funding (7D) ~0.0294%, increasing volatility risk on reversals. Farside Investors |

Institutional & Treasury Positioning: Reserved, Cautious and Selective

Institutional behaviour remains cautious but no longer uniformly reduces exposure. Some allocators appear comfortable maintaining or adding liquid beta (via majors/ETFs), while many desks still prioritize capital efficiency and hedged structures given thin depth into year-end. The key macro risk in this week‘s window is U.S. CPI on December 18, which can reprice real yields and liquidity expectations quickly.

Global Stablecoins — Supply, Distribution & Liquidity Signal

Global stablecoin supply expanded modestly during the past week, with total stablecoin market capitalization rising to ~US$309.9B (US$1.6B, around 0.44% WoW). This marks a shift away from outright contraction, but the pace of growth remains slow and insufficient to signal a full liquidity cycle reversal.

Key observations:

Net stablecoin issuance remains selective, not broad-based, suggesting liquidity is returning cautiously rather than aggressively.

Chain-level divergence is widening:

Solana stablecoin supply continued to grow (around 2–3% WoW), reinforcing its position as a relative liquidity magnet.

Arbitrum and Avalanche experienced notable stablecoin drawdowns, reflecting capital rotation away from mid-tier ecosystems.

USDT and USDC growth remains subdued, indicating that large institutional allocators have not yet resumed meaningful balance-sheet expansion via stablecoins.

While the global stablecoin base is no longer stagnant, the lack of strong net minting and the concentration of liquidity on a few chains indicate that crypto liquidity remains distribution-constrained. This supports a regime where capital is rotating within the ecosystem rather than entering it at scale.

DeFi Overview — TVL Dynamics & Protocol Rotation

DeFi activity this week continues to reflect a liquidity-constrained, rotation-driven environment, rather than a broad re-risking phase. While headline metrics show TVL stabilization, the underlying composition reveals that capital is concentrating into simpler, lower-risk structures, with limited appetite for leverage-dependent or complexity-heavy strategies.

TVL: Stabilization Without Expansion

Total DeFi TVL has stopped declining aggressively, but remains range-bound, with movements driven more by asset price fluctuations than by fresh capital inflows. This indicates that the recent stabilization is valuation-supported, not flow-supported. While there is no clear evidence of new balance-sheet expansion from institutions or large DeFi allocators. But the TVL elasticity remains high — meaning price moves, rather than deposits, dominate changes.

In practical terms, DeFi is holding ground, not rebuilding.

Protocol-Level Rotation: Capital Seeking Simplicity

Capital allocation patterns show clear preference for core, low-complexity protocols:

Lending & Core Infrastructure (Defensive Allocation)

Protocols such as Aave, Compound, and core money markets have retained liquidity share.

Deposits remain largely overcollateralized and conservatively structured, with minimal use of recursive leverage.

Borrow demand remains muted, reflecting limited directional conviction.

Liquid Staking & Restaking (Relative Resilience)

Lido, EigenLayer, ether.fi continue to attract flows relative to other sectors.

Capital is drawn by protocol-native yield (staking rewards) rather than financial engineering.

Restaking participation remains steady, but new inflows are incremental, not explosive.

Structured Yield & Leverage Strategies (Capital Exit)

More complex DeFi strategies — including structured vaults, delta-neutral farms, and synthetic leverage products — continue to see outflows or stagnation.

These strategies are most sensitive to tight stablecoin liquidity, higher funding costs and reduced risk tolerance.

Overall, the DeFi activity continues to reflect a liquidity-led consolidation. Stablecoin supply is modestly expanding overall (+0.44% 7D), but distribution remains uneven: Solana gains while Arbitrum and Avalanche contract, consistent with continued ecosystem rotation rather than broad-based DeFi re-risking.

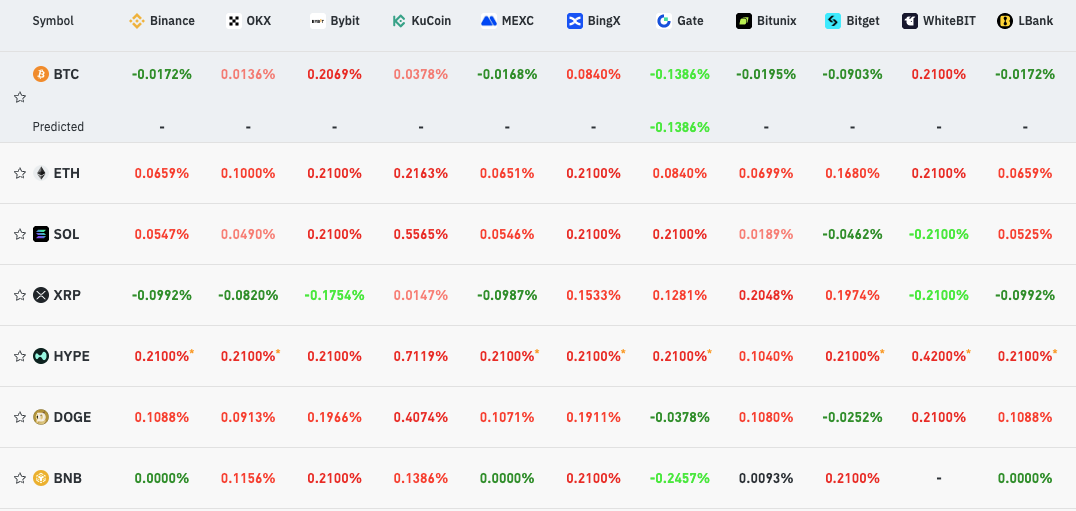

Funding Rate Snapshots

Source: https://www.coinglass.com/AccumulatedFundingRate (The data is based on the last 7 days' funding rate taken snapshot on December 15, 2025)

Asset | Funding trend | Interpretation |

|---|---|---|

BTC | Neutral but mildly defensive, low conviction directional trades | Indicates balanced or slightly short-biased positioning No signs of aggressive leverage buildup Consistent with risk-controlled institutional exposure BTC continues to act as a liquidity parking asset, not a leverage target |

ETH | Constructive bullish bias, healthy but crowded positioning | Reflects persistent long bias across retail and institutional participants Funding is elevated but not accelerating, suggesting controlled leverage ETH remains the preferred beta exposure relative to BTC |

SOL | Bullish but crowded with high volatility, liquidation-sensitive | Indicates aggressive long positioning Elevated funding dispersion suggests speculative leverage Vulnerable to sharp liquidations on adverse moves Dominated by momentum-driven flows rather than hedged exposure |

XRP | Range-bound, positioning conflict, low conviction | Indicates two-sided positioning Hedging or short interest persists on liquid venues Speculative longs appear concentrated offshore |

Outlook for the Remainder of the Week (Dec 15–21)

Macro & Liquidity Drivers

U.S. CPI (Dec 18) is the dominant macro catalyst for risk assets this week.

With the FOMC already concluded earlier in the month, CPI-driven repricing will dictate near-term liquidity expectations.

Liquidity & Flow Watchpoints

Persistence of ETF inflow stabilization into and after CPI.

Acceleration (or stalling) of global stablecoin supply growth.

Whether stablecoin expansion broadens beyond a few dominant chains.

Absent a stronger stablecoin issuance impulse, upside is likely to remain range-bound and rotation-driven rather than trend-driven.

Positioning Summary This Week

Given current conditions, institutions remain focused on:

BTC, ETH, SOL as liquid core exposures.

Minimizing exposure to long-tail, low-liquidity assets.

Prioritizing liquidity management and conservative sizing into key macro events.

Waiting for broader stablecoin expansion and sustained ETF inflows before scaling risk.

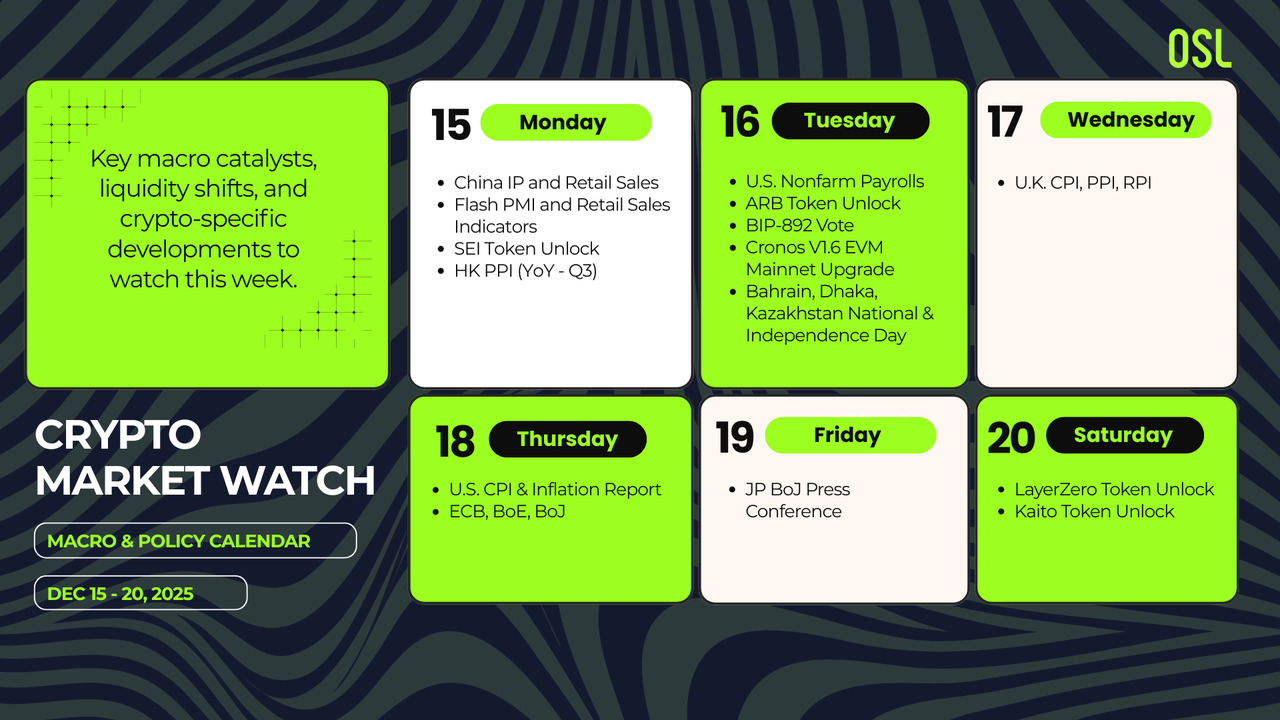

Crypto Market Watch: Key Events & Liquidity Drivers (Dec 15–21, 2025)

Event Category | Region Focus | Why It Matters | Dates |

|---|---|---|---|

U.S. Labor Market & Employment Data | U.S. | After delayed releases due to the government shutdown, November nonfarm payrolls and other labor data are released mid-week. Strong jobs mean tighter policy expectations; weak jobs mean dovish Fed expectations and increased risk appetite. | Dec 16 (Nonfarm Payrolls) |

U.S. CPI & Inflation Reports | U.S. | November CPI is a major inflation indicator. A hotter print could strengthen the USD and tighten liquidity, pressuring risk assets including crypto, while a softer print can support more dovish expectations and stabilize flows. | Dec 18 (CPI) |

Central Bank Policy Decisions | EU, UK, Japan | ECB, BoE, and BoJ decisions will shape global monetary conditions and risk sentiment. Policy stances outside the U.S. can influence FX flows and risk appetite across markets. | Dec 18–19(ECB, BoE, BoJ) |

Flash PMI & Retail Sales Indicators | U.S., Europe | Flash PMIs and retail sales gauge economic momentum ahead of final prints. These are early signals of growth/slowdown trends, which influence policy expectations and market risk pricing. | Dec 15–19(PMIs / Retail Sales) |

China Economic Data | China | China's industrial production and retail sales data early in the week provide clues on consumer demand and growth momentum, affecting global risk sentiment and commodity-linked FX flows. | Dec 15 (China IP & Retail Sales) |

Source: https://www.investing.com/holiday-calendar/

Crypto-Specific Catalysts to Watch

Catalyst Type | Example Event | Impact | Why It Matters | Dates |

|---|---|---|---|---|

Token Unlocks & Supply Events | ARB Token Unlock (~$19M unlocked) | Increased circulating supply → potential selling pressure | Additional supply in thin liquidity windows can widen funding spreads and increase volatility for ARB & correlated L2 tokens. ARB unlocks feed into broader supply dynamics for L2 ecosystems. | Dec 16 |

Network & Protocol Activity | Sei Token Unlock (~55.56M tokens) | Short-term volatility | Unlock on mid-cap assets like Sei can redistribute supply from locked holders into markets, pressuring prices and influencing funding rates for correlated multisector tokens. | Dec 15 |

Ecosystem Engagement / Team Updates | Web3 talks, AMAs, team events for Aleo, Conflux, Turbo, Fluid | Narrative and engagement drivers | Project-level updates and community talks can catalyze attention, narrative momentum, and short-term trading flows, especially if tied to roadmap steps or product milestones. | Dec 15–21 |

Market Structure & Liquidity | Exchange microstructure shifts & liquidity clustering | Capital rotation across venues | Markets often process supply shocks (e.g., unlocks) through liquidity repricing — majors can attract flows while smaller assets face widening perp funding and OI dispersion. (General pattern from past unlock/microstructure regime shifts) | Dec 15–21 |

Source: https://coinmarketcap.com/events/, coinmarketcal.com

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics