When Re-Engagement Meets Reality — BTC Dominance Holds as Liquidity Stays Constrained

The second full trading week of January is typically where early optimism is tested. After the initial re-engagement at the start of the year, markets move past thin liquidity and headline-driven repricing and begin to reveal whether positioning can be sustained without fresh capital.

Jan 12–18 delivered a clear verdict. Bitcoin held firm, dominance remained elevated, and institutional participation persisted, but market breadth failed to expand. Stablecoin supply stayed flat, funding conditions became increasingly differentiated across assets, and risk expression narrowed. Rather than transitioning into a breakout phase, the market settled into confirmation and consolidation.

This pattern was not unique to crypto. In commodities, energy and precious metals remained supported, but momentum slowed. Price action reflected hedging demand and capital preservation rather than aggressive reflation trades. Across asset classes, capital was present — but carefully managed, hedged, and recycled rather than broadly deployed.

Key Market Review: Crypto Stability Mirrors Cross-Asset Caution

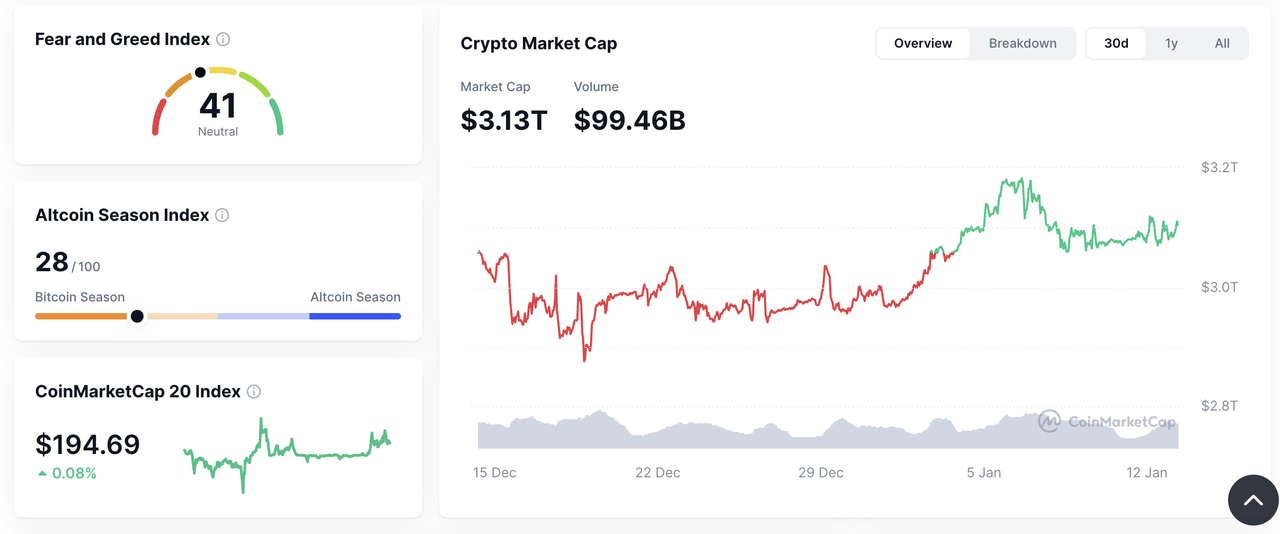

By mid-January, crypto market structure closely resembled broader cross-asset behavior. Total market capitalization stabilized in the low-$3 trillion range, Bitcoin dominance remained near cycle highs, and Ethereum's share stayed comparatively muted. Participation outside the majors failed to meaningfully accelerate.

The same posture was visible in commodities. Gold remained range-bound but well supported, signaling demand for macro hedges without urgency. Energy markets were steady rather than explosive, as geopolitical risk premiums were offset by demand uncertainty and disciplined supply. In both cases, markets were pricing resilience, not acceleration.

Liquidity — The Common Constraint Across Assets

Liquidity remains the binding constraint, and it is where crypto and commodities align most clearly. In crypto, aggregate stablecoin supply remained effectively flat throughout the week. Capital was available and deployable, but it was not expanding. In commodities, futures curves and positioning conveyed a similar message: exposure was being held, but leverage extension remained limited.

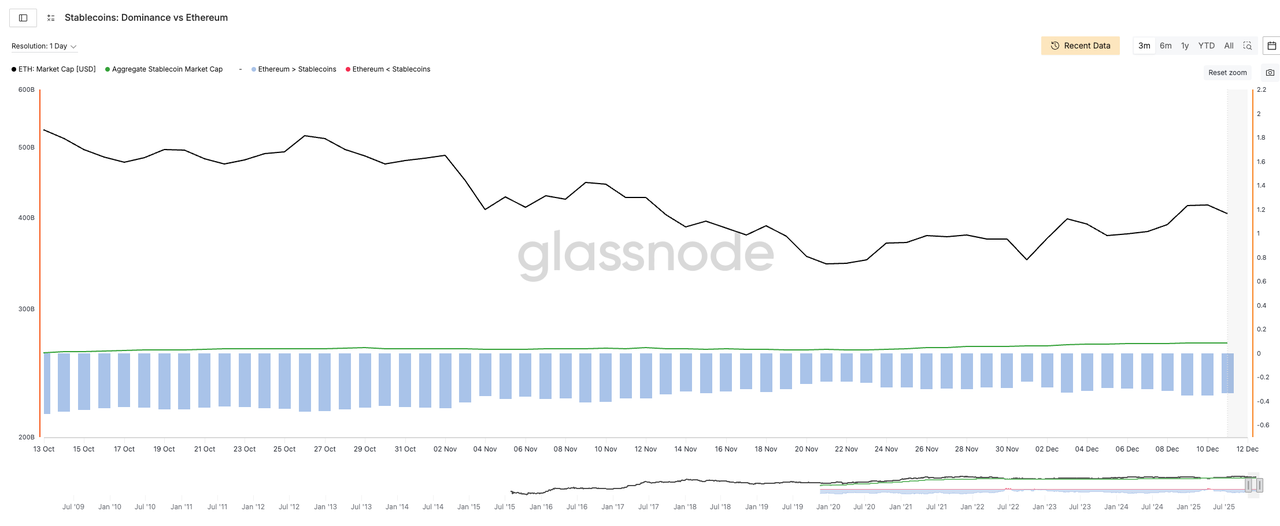

Ethereum continued to dominate stablecoin balances, reinforcing its role as the system's settlement rail — analogous to U.S. Treasuries or gold in traditional markets. Capital was positioned for flexibility, ready to respond to macro shifts, but reluctant to commit aggressively without clearer signals on inflation, rates, and growth.

When both crypto liquidity and commodity positioning reflect caution, it typically signals a macro regime where risk is managed rather than maximized.

Institutional Flows — Hedging First, Expansion Later

ETF flows into Bitcoin remained supportive throughout the week, providing a structural bid and reinforcing BTC's role as a digital macro hedge. Ethereum continued to attract selective interest, but without urgency. These patterns echo flows seen in commodity-linked instruments, where allocations have favored defensive exposure over directional bets.

Just as gold allocations tend to increase when investors seek protection rather than yield, Bitcoin flows during this period appear driven more by portfolio resilience and optionality than by outright growth expectations. The absence of aggressive accumulation underscores that institutions are still testing the regime, not committing to it.

Asset | Latest Daily Flow (Jan 9) | AUM (approx.) | Interpretation for Jan 12–18 |

|---|---|---|---|

Bitcoin (BTC) | –US$250m | ~US$92.67B | Short-term outflows on Jan 9 reflect tactical repositioning as the market digests early gains, but overall BTC flows have shown broad engagement since the turn of the year, supporting BTC’s defensive role with institutions maintaining exposure even as flows oscillate. (DeFi Llama) |

Ethereum (ETH) | –US$93.8m | ~US$13.106B | Similar tactical flows versus structural participation; ETH flows have been comparatively smaller and more variable, signaling measured beta exposure rather than a broad shift in institutional risk appetite. (DeFi Llama) |

Solana (SOL) | Proxy inflows noted in market proxies | — | Solana does not yet have deep liquid, regulated ETF flow data on DeFiLlama, but market proxies and ecosystem proxies indicate sensitivity to short-term rotation and funding rather than large, regulated capital flows. |

This week's ETF flow data highlights the measured and tactical nature of institutional engagement. While Bitcoin and Ethereum exhibited net outflows on a given reporting date, this should not be conflated with a loss of institutional interest. Rather, it reflects short-term repositioning amid consolidation and profit-taking, consistent with broader liquidity constraints.

Bitcoin's large AUM base continues to function as the primary liquidity anchor, with institutions holding exposures even as daily flows fluctuate. Ethereum's flows — smaller and less consistent — align with its role as secondary beta. Solana's flow profile remains best understood through on-chain proxies and trading activity rather than deep regulated ETF flows, underscoring its current sensitivity to derivatives positioning and stablecoin distribution more than pure flow acceleration.

This flow pattern supports the week's broader narrative: institutional participation is supportive but not aggressively expanding. The ETF channel continues to absorb and manage capital, acting as a stabilizer in a market where stablecoin liquidity is flat and concentrated. Sustained upside will likely require more persistent and broad-based ETF flows rather than isolated daily prints — a pattern that institutional allocators are keenly watching.

Global Stablecoins — Liquidity Is Available, but Concentration Limits Breadth

The market's digestion phase is best understood through stablecoins. Aggregate supply remained flat, confirming that system liquidity did not expand even as prices held firm. Capital was neither fleeing nor accelerating — it was waiting.

More importantly, liquidity remained highly concentrated. Ethereum continued to dominate as the primary settlement rail, reflecting institutional preference for depth, reliability, and execution quality when conviction is conditional. This concentration naturally supports resilience in major assets but limits the durability of broad-based rallies.

Without new issuance or wider dispersion, leverage and positioning become the marginal drivers of price, explaining why volatility during the week was event-driven rather than trend-driven.

Market Structure — Acceptance Above Key Levels Matters More Than Breakout Speed

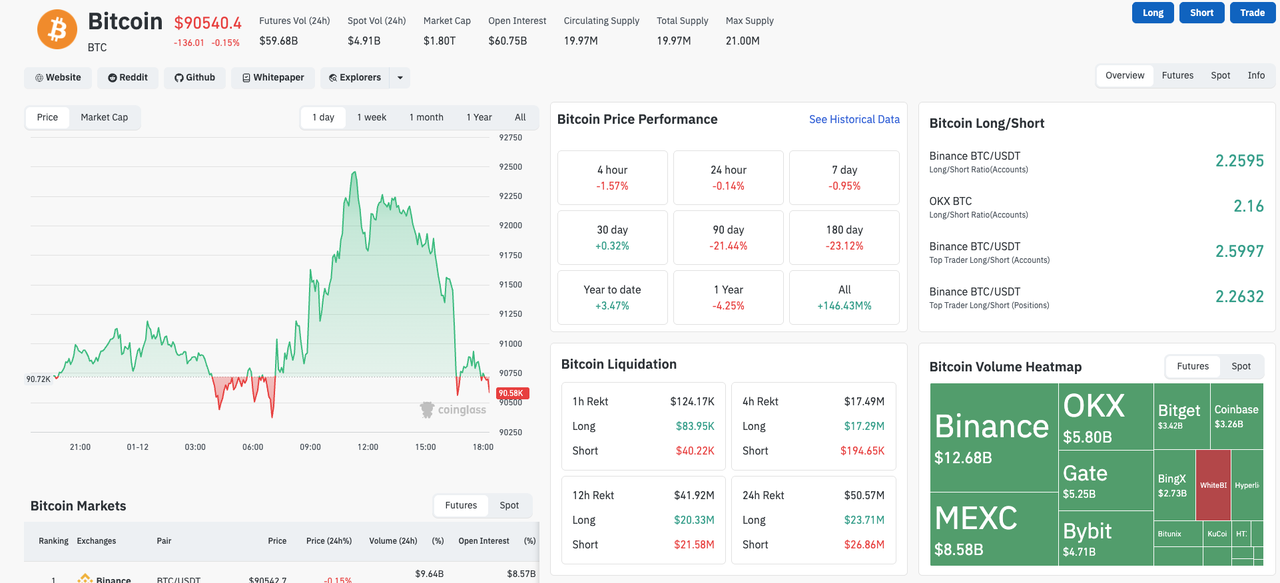

Bitcoin's ability to hold above key levels through Jan 12–18 should be read less as a momentum signal and more as a liquidity acceptance test. In environments where new capital formation is limited, price stability becomes a function of whether existing capital is willing to stay engaged, rather than whether incremental buyers are rushing in.

This is precisely what the market demonstrated during the week. Spot and ETF flows provided enough structural demand to absorb supply, while derivatives activity drove short-term volatility without destabilizing the broader range. The absence of follow-through is therefore not a sign of weakness, but evidence that the market is digesting early-January positioning under constrained liquidity conditions.

A similar pattern is often observed in commodities during mid-cycle pauses: prices remain elevated, but extension stalls until liquidity, demand, or policy conditions change. Crypto, during this period, behaved much the same way.

DeFi & On-Chain — Rotation Dominates as Capital Reallocates Within the System (Jan 12 to Jan 18)

Source: TVL and DEX on DeFillama

Against that stablecoin backdrop, DeFiLlama's TVL and DEX data paint a coherent picture. Total value locked remained broadly stable during Jan 12–18, signaling that on-chain balance sheets are holding, not contracting. However, the absence of stablecoin growth confirms that this stability is not being underwritten by fresh capital inflows.

Instead, activity is increasingly concentrated where turnover efficiency is highest. DEX volumes remained robust at the system level, but leadership skewed toward venues and chains optimized for rapid trading and short-duration risk expression. Solana, in particular, absorbed a disproportionate share of DEX and perpetual volume even as its stablecoin base declined, indicating higher velocity on existing capital rather than new liquidity entering the ecosystem.

Ethereum, by contrast, continued to function as the system's balance sheet and settlement layer. Its dominant TVL and steady, but less frenetic, DEX activity underscore its role as the venue where capital consolidates for collateral efficiency, custody-aligned execution, and institutional-grade risk management.

The divergence between chains is therefore not contradictory — it is complementary. One rail concentrates liquidity and preserves optionality; the other expresses tactical risk. Crucially, because stablecoin issuance and dispersion did not accelerate, these dynamics remained rotation-led rather than expansionary.

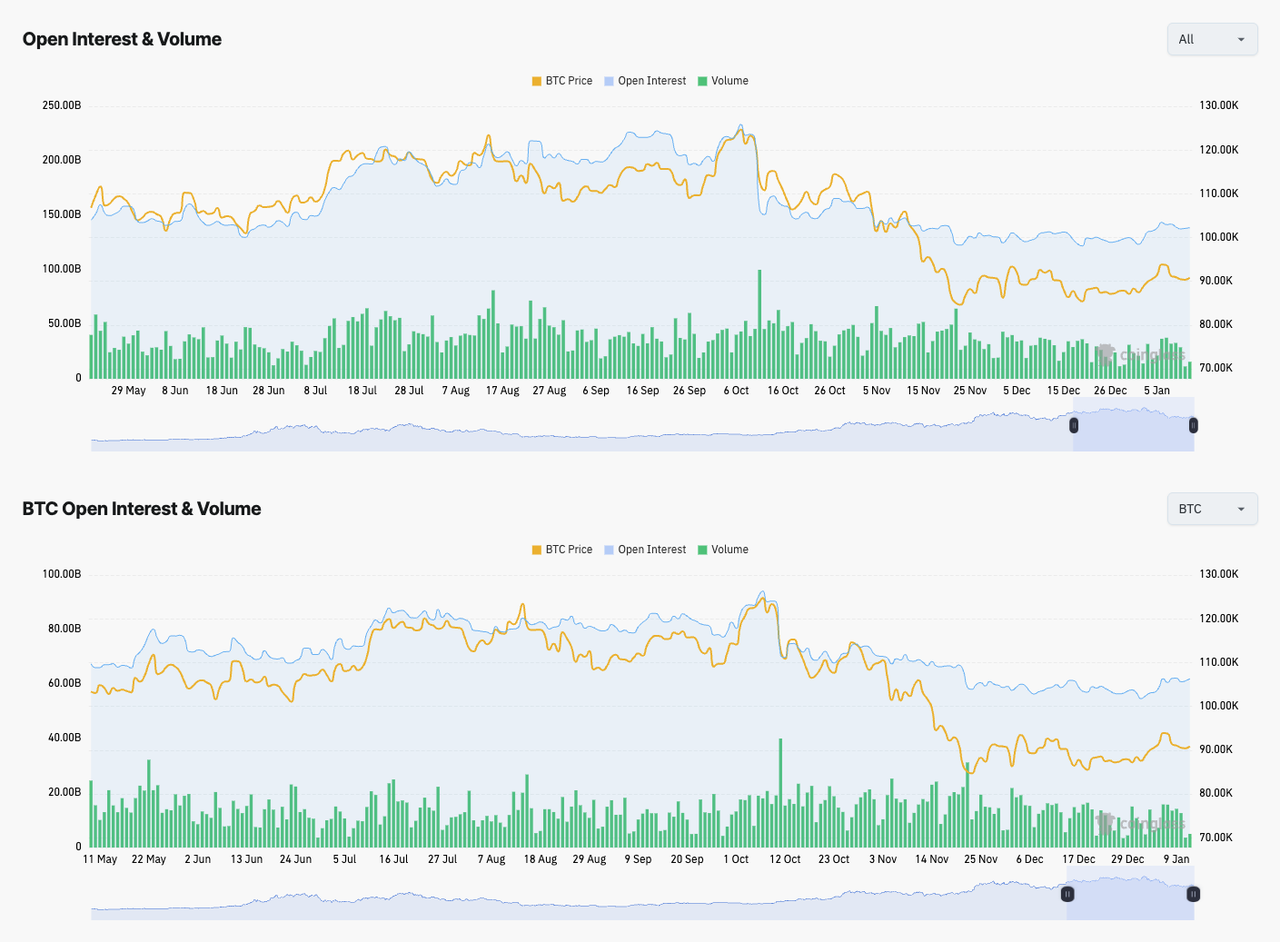

Derivatives — Leverage Rebuilt, but Still Constrained by Liquidity

Source: Coinglass Open Interest & Volume

CoinGlass futures data shows that derivatives activity remained elevated through Jan 12–18, reflecting continued engagement as desks moved from re-entry into position management. Open interest stayed high across major contracts, confirming that leverage has returned to the system, but the pace of expansion slowed compared with early January — a sign that positioning is being maintained rather than aggressively added.

The relationship between open interest and trading volume is instructive. While turnover remained healthy, leverage has not been accompanied by a commensurate expansion in spot depth or system liquidity. In this setup, futures positioning tends to amplify short-term price moves rather than establish durable trends, particularly around macro headlines and data releases.

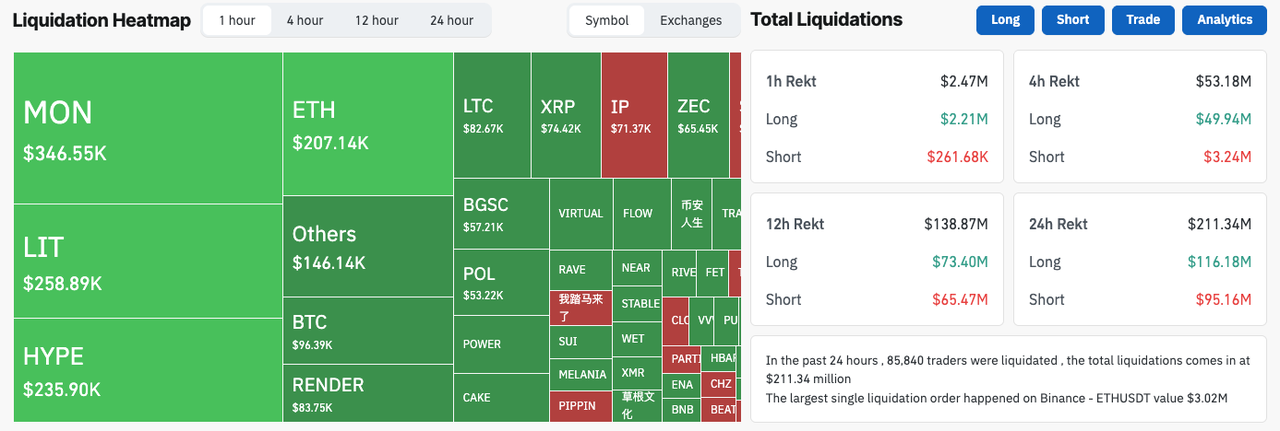

Liquidations during the week were episodic and two-sided, clearing pockets of crowded positioning without triggering a broader deleveraging event. This pattern is consistent with a range-bound, consolidation regime, where leverage is actively managed and reset rather than forced out in one direction.

For institutional participants, the takeaway is straightforward: derivatives remain an important driver of intraday volatility, but without broader liquidity expansion, leverage should be viewed as tactical rather than trend-defining.

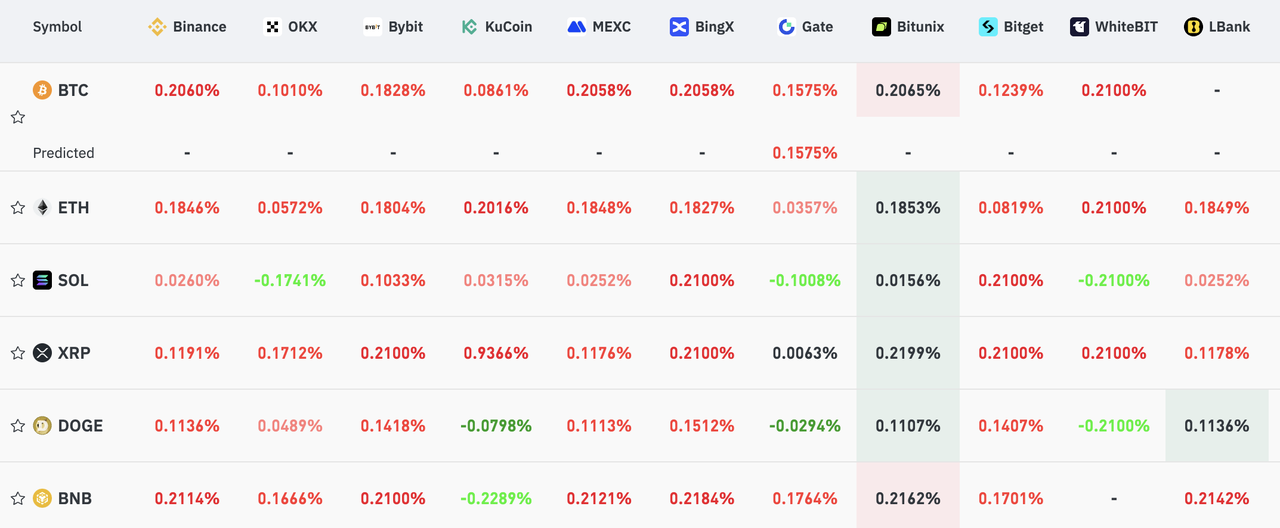

Funding & Positioning — Positive Carry Persists, but Conviction Is Uneven

Source: https://www.coinglass.com/AccumulatedFundingRate (The data is based on the last 7 days' funding rate taken snapshot on January 13, 2025)

Asset | Funding Character | Cross-Exchange Signal | Institutional Interpretation |

|---|---|---|---|

BTC | Mildly positive, dispersed | Funding clustered in the ~0.10%–0.20% range across venues, with no single exchange dominating | Balanced positioning with active hedging. BTC remains the system's liquidity anchor rather than a crowded long; supportive for consolidation above key levels but not a breakout driver without new liquidity. |

ETH | Consistently positive, tight | Positive funding across nearly all venues with relatively low dispersion | Cleanest long structure among majors. Reflects stronger consensus positioning and preferred beta exposure; constructive so long as spot and ETF flows remain supportive. |

SOL | Elevated, fragmented | Funding oscillates between positive and negative across exchanges | Tactical risk expression dominates. Indicates higher volatility and liquidation sensitivity, particularly around macro catalysts or leverage adjustments. |

XRP | Uniformly positive, crowded | Funding clustered near upper bounds across multiple venues | Crowded long positioning limits follow-through. Prone to range-bound or mean-reverting price action in a liquidity-constrained environment. |

With ETF flows supportive but stablecoin liquidity flat, this funding structure favors selective upside led by BTC and ETH, while assets with crowded or fragmented funding profiles (SOL, XRP) remain more vulnerable to volatility spikes and tactical reversals. Unless funding dispersion narrows and spot liquidity deepens, rallies are likely to remain rotation-driven rather than trend-defining.

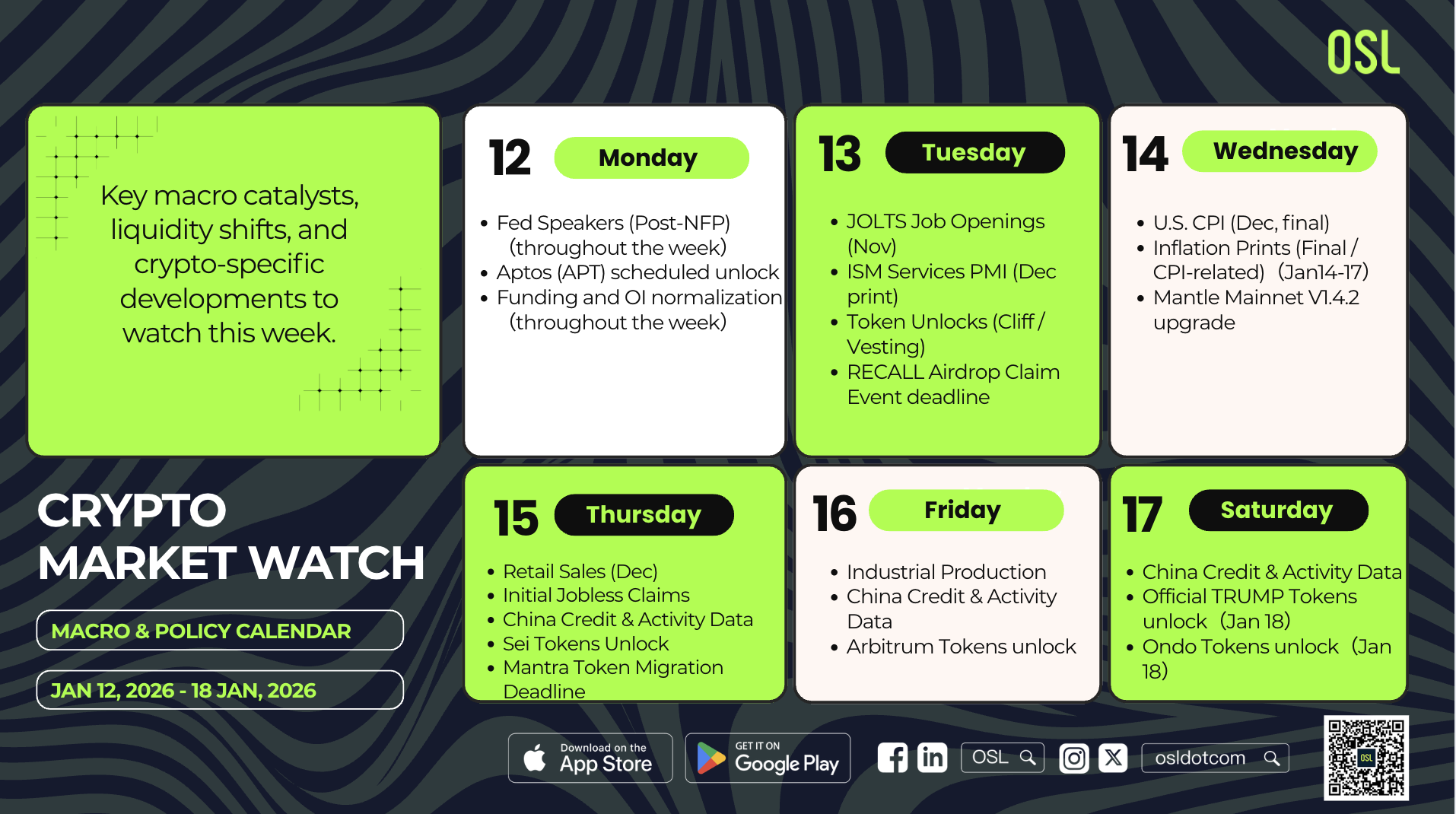

Crypto Market Watch: Key Events & Liquidity Drivers (Jan 12–18, 2026)

Event Category | Region Focus | Why It Matters (Liquidity / Risk) | Date |

|---|---|---|---|

U.S. CPI (Dec, final) | U.S. | Critical confirmation of inflation trajectory after NFP. A hotter-than-expected print could reprice front-end rates, strengthen USD, and pressure leveraged crypto positioning; a benign print supports consolidation above key levels. | Jan 14 |

Retail Sales (Dec) | U.S. | Gauge of real-economy demand and consumption strength. Weak prints reinforce disinflation narrative and risk support; strong prints may revive rate volatility, impacting crypto beta. | Jan 15 |

Initial Jobless Claims | U.S. | High-frequency labor stress signal. Sudden deterioration can support risk assets via rate-cut expectations; resilience keeps policy uncertainty elevated. | Jan 15 |

Fed Speakers (Post-NFP) | U.S. | Messaging around inflation persistence and financial conditions can drive intraday volatility, especially with leverage elevated and liquidity flat. | Throughout week |

Industrial Production | U.S. | Manufacturing momentum check following ISM data. Weakness supports “soft landing” risk-on framing; strength may tighten conditions. | Jan 16 |

Inflation Prints (Final / CPI-related) | Europe | Confirms whether EU disinflation remains on track. Spillover into EUR rates and USD strength affects global risk appetite and crypto funding dynamics. | Jan 14–17 |

China Credit & Activity Data | China | Credit growth and activity indicators influence commodity demand and EM risk sentiment, indirectly affecting crypto via cross-asset flows. | Jan 15–17 |

Crypto-Specific Catalysts to Watch (Jan 12–18, 2026)

Catalyst Type | Example Event | Date |

|---|---|---|

Token Unlocks (Vesting / Emissions) | Aptos (APT) scheduled unlock Sei Tokens Unlock Arbitrum Tokens unlock Official TRUMP Tokens unlock Ondo Tokens unlock | Jan 12 Jan 15 Jan 16 Jan 18 Jan 18 |

Crypto Events | RECALL Airdrop Claim Event deadline Mantle Mainnet V1.4.2 upgrade Mantra Token Migration Deadline | Jan 13 Jan 14 Jan 15 |

Perpetual Market Rebalancing | Funding and OI normalization | Throughout week |

Stablecoin Flow Watch | Chain-level inflows/outflows | Continuous |

ETF Flow Continuity | BTC & ETH spot ETFs | Daily |

Macro data this week shifted from direction-setting to validation. U.S. CPI, Retail Sales, and labor data tested whether early-January repricing was justified. With leverage elevated and liquidity flat, even second-tier releases carried the potential to drive outsized intraday moves.

At the same time, crypto-specific catalysts — token unlocks, funding normalization, ETF flow continuity, and stablecoin movements — mattered less for their headlines and more for how they interacted with already-tight liquidity conditions. In a market where majors are supported but breadth is thin, even routine supply events can disproportionately impact relative performance.

Closing Thoughts

Jan 12–18 was not about breaking higher — it was about proving acceptance. The market remains structurally sound, but liquidity-constrained. Bitcoin and Ethereum continue to lead, while higher-beta assets remain vulnerable to rotation and volatility.

Until liquidity expands — via stablecoin issuance, broader ETF participation, or macro easing — the regime favors discipline over aggression, and durability over momentum.

More About Topics

More About Topics

Latest

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Transfer to OSL: Gas Fee Rebate + VIP Bonus + Welcome Gift, Triple Rewards in One Go

Transfer to OSL for stackable triple rewards: Gas Fee rebate, VIP bonus and a welcome gift. SFC-licensed, transfer with confidence.

Transfer to OSL: Gas Fee Rebate + VIP Bonus + Welcome Gift, Triple Rewards in One Go

BlackRock Trims BTC as Bitmine Adds 75,000 ETH: Deciphering Institutional Capital Flows

BlackRock rebalances portfolios while Bitmine buys 75,000 ETH. Analyze why institutional capital is shifting from BTC to Ethereum.

BlackRock Trims BTC as Bitmine Adds 75,000 ETH: Deciphering Institutional Capital Flows

Top Crypto Exchanges in Hong Kong: Your Guide to Safe and Compliant Platforms

Explore the top cryptocurrency exchanges in Hong Kong. Learn how to choose a safe and compliant platform, featuring insights on licensed exchanges like OSL with $1 billion asset insurance, HKD trading, and SFC compliance.

Top Crypto Exchanges in Hong Kong: Your Guide to Safe and Compliant Platforms

Recommended For You

More About Topics

More About Topics