Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

A Very Short List

When a regulator opens a new licensing regime, the interesting question is usually not who applied, but who got through. Hong Kong's first stablecoin round answers it sharply.

The HKMA received 36 applications by the 30 September 2025 deadline. After a six-month review, it issued two licences on 10 April 2026, to The Hongkong and Shanghai Banking Corporation (HSBC) and to Anchorpoint Financial, a joint venture of Standard Chartered Bank (Hong Kong), HKT, and Animoca Brands. They appear on the official register as licence numbers FRS02 and FRS01, both effective that day, per the HKMA's Register of Licensed Stablecoin Issuers.

Two out of thirty-six is a roughly 6% pass rate. The HKMA had signalled the round would be small, and it was. But the more telling detail is the identity of the winners.

The Banknote Connection

Hong Kong is unusual: its central bank does not print most of its cash. Under authorisation from the government through the HKMA, three commercial banks issue Hong Kong dollar banknotes, HSBC, Standard Chartered (Hong Kong), and Bank of China (Hong Kong), a system that traces back to private note issuance in the 1800s, as the HKMA's currency pages describe.

Look at the first stablecoin licences again. HSBC is a note-issuing bank. Anchorpoint is led by Standard Chartered, another note-issuing bank. So two of the city's three banknote issuers are now also its first licensed digital-dollar issuers. As CoinDesk noted, the decision to start with the note-issuing banks looks deliberate.

The logic is straightforward. These banks already carry the operational and trust obligations of putting Hong Kong dollars into circulation against backing held with the Exchange Fund. Extending that role to a fully-reserved digital token is a smaller conceptual leap than handing the job to a newcomer. For a regulator whose stated priority was risk management, reserve quality, and anti-money-laundering controls, the safest first movers were the institutions already trusted with the physical currency.

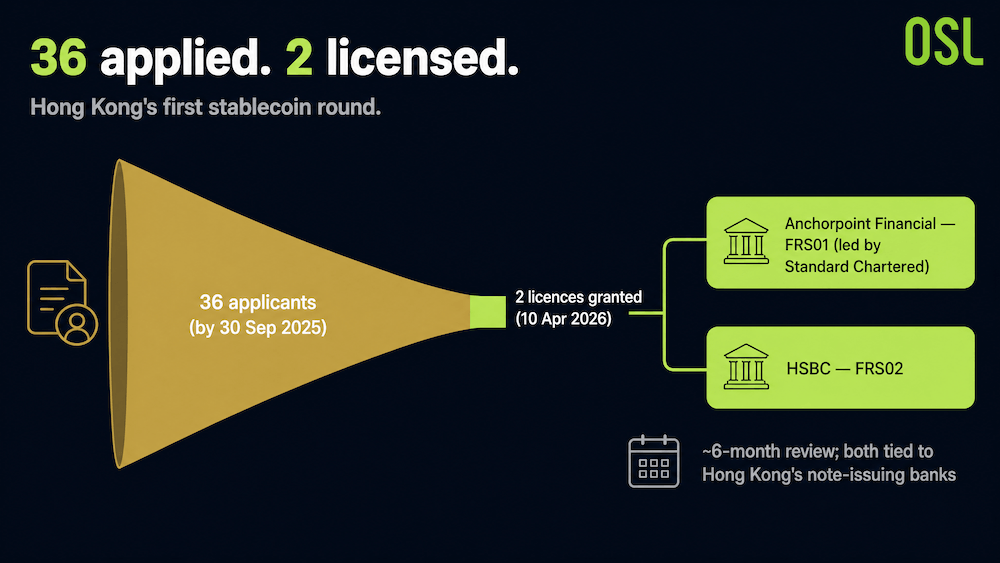

Chart 1: From 36 Applicants to 2 Licensees

source: HKMA's Register of Licensed Stablecoin Issuers, HKMA inSight — Robust development of the regulated stablecoin ecosystem in Hong Kong (10 April 2026)

The funnel is steep. Thirty-six entities applied by the 30 September 2025 deadline. The HKMA spent six months reviewing each one, then granted two licences on 10 April 2026: Anchorpoint Financial (FRS01) and HSBC (FRS02). Both licences took effect the same day. Of the two licensees, both are tied to Hong Kong's note-issuing banks, HSBC directly, and Anchorpoint through its lead partner Standard Chartered.

What the Two Will Actually Issue

Both licensees plan to start with a Hong Kong dollar (HKD) stablecoin, not a US dollar one. That matters, because it points the first wave of Hong Kong's regulated tokens at local and regional use rather than international dollar settlement. It also leaves the bigger international prize open, which is why Hong Kong's dollar peg makes it a natural USD-stablecoin hub.

HSBC plans to launch an HKD-denominated stablecoin in the second half of 2026 and to integrate it into PayMe and the HSBC HK App, reaching retail and corporate users directly. In its own statement, HSBC said each token will be fully backed at all times by high-quality liquid assets held in segregated accounts.

Anchorpoint plans a phased rollout from the second quarter of 2026, focused on cross-border payments, tokenised asset settlement, and supply chain finance. Together the two issuers turn Hong Kong's legal clarity and the HKD's credit base into what the OSL × Hong Kong Polytechnic University report calls "programmable digital liquidity."

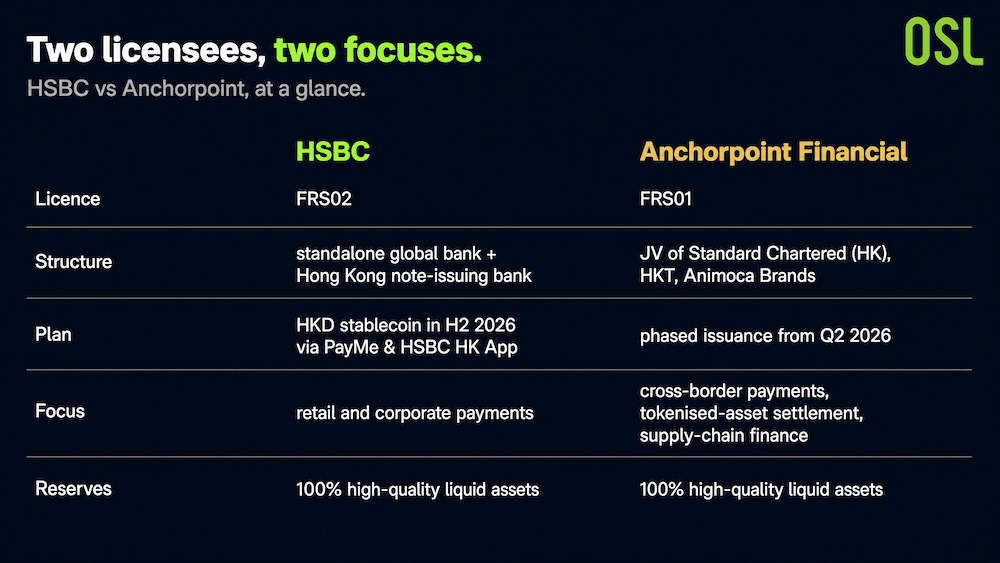

Chart 2: The Two First Licensees at A Glance

source: HKMA inSight — Robust development of the regulated stablecoin ecosystem in Hong Kong (10 April 2026), HSBC

The two licensees differ in structure and focus. HSBC holds licence FRS02; it is a standalone global bank and a Hong Kong note-issuing bank, and it plans an HKD stablecoin in H2 2026 distributed through PayMe and the HSBC HK App, aimed at retail and corporate payments. Anchorpoint Financial holds licence FRS01; it is a joint venture of Standard Chartered Bank (Hong Kong), HKT, and Animoca Brands, and it plans phased issuance from Q2 2026, aimed at cross-border payments, tokenised asset settlement, and supply chain finance. Both must hold 100% reserves in high-quality liquid assets under the Stablecoins Ordinance.

The Ordinance Behind the Licences

The licences sit on top of a law that was finished before the applications were judged. Hong Kong's Stablecoins Ordinance (Cap. 656) was passed on 21 May 2025 and took effect on 1 August 2025, with the HKMA setting a six-month transition period. That sequencing, law first, licences second, is what lets Hong Kong claim to be the first major financial centre to close the loop from legislation to live issuance.

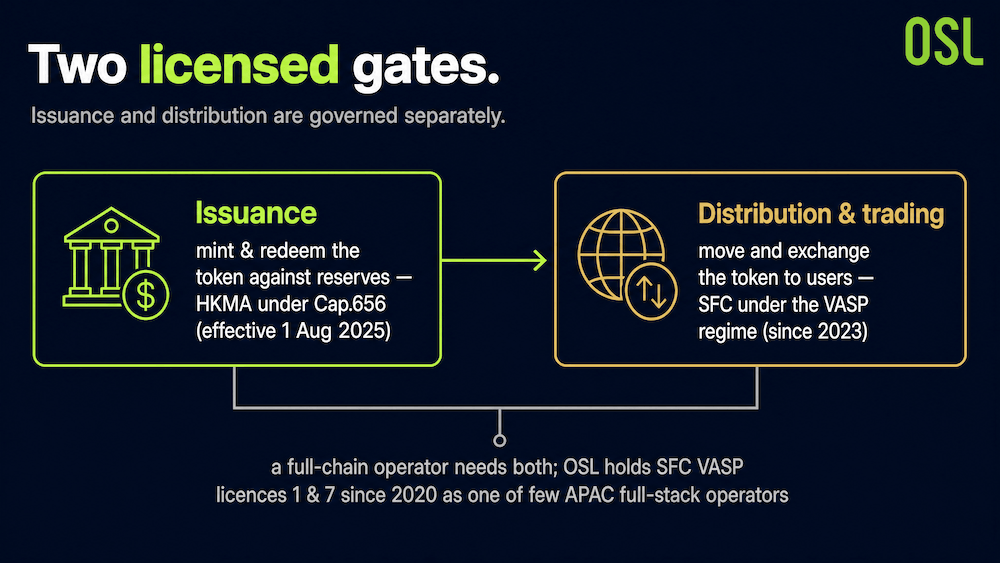

The framework also has a second layer that is easy to miss. Issuing a stablecoin requires an HKMA licence, but distributing and trading one requires a separate Virtual Asset Service Provider (VASP) licence from the Securities and Futures Commission. The two regimes interlock. The report points to OSL as an example of the full stack: it has held SFC VASP licences (types 1 and 7) since 2020, which lets it handle distribution, enterprise payments, and stablecoin conversion within the licensed perimeter. Issuance and circulation are governed separately, and a serious participant needs to satisfy both.

Chart 3: Hong Kong's Two-licence Structure

The structure splits stablecoin activity into two licensed gates. Issuance, minting and redeeming the token against reserves, sits with the HKMA under Cap. 656. Distribution and trading, moving the token to users and exchanging it, sits with the SFC under the VASP regime introduced in 2023. A firm that wants to run the full chain needs both. OSL, holding SFC VASP licences 1 and 7 since 2020, is cited as one of the few Asia-Pacific operators able to run that full compliant stack.

Why Start So Narrow

Licensing two issuers is a strong signal, but it is also a constraint. The report is candid about the gap between regulatory clarity and a working market.

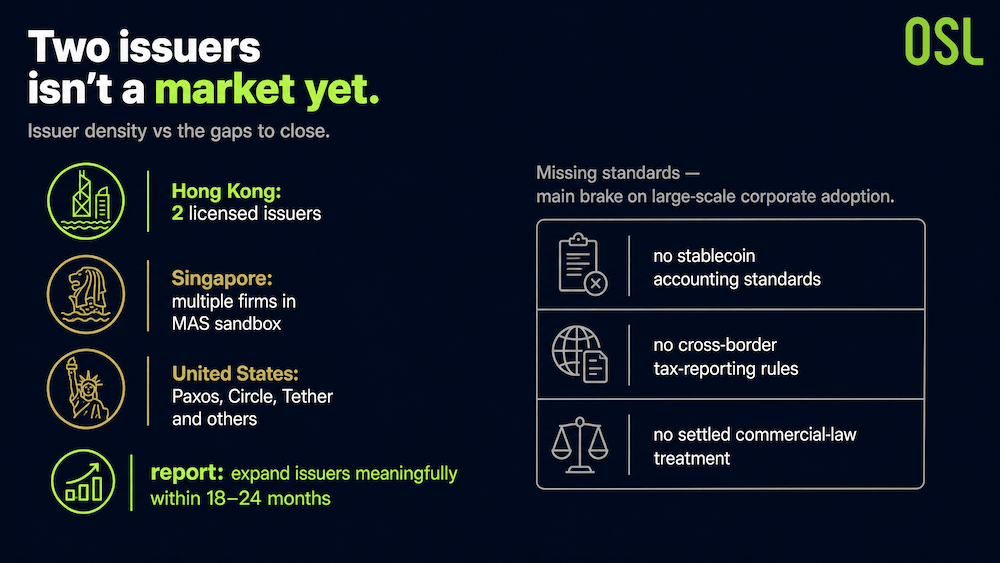

Hong Kong currently has only two licensed issuers, which is far below the density a mature payment system needs. By comparison, Singapore has multiple firms in the MAS sandbox, and the United States has Paxos, Circle, and Tether among others. The report argues Hong Kong needs to expand the number of licensed issuers meaningfully within 18 to 24 months to build a competitive, multi-coin ecosystem.

There are softer gaps too. Hong Kong has not yet published accounting standards for how a company should classify stablecoin holdings on its balance sheet, nor tax-reporting rules for cross-border stablecoin flows, nor settled commercial-law treatment of stablecoin settlement. The report flags these missing standards as the main brake on large-scale corporate adoption, and notes the work of UNCITRAL and Hong Kong's Law Reform Commission will matter here.

Chart 4: Comparison of Stablecoin Issuer Density

So the narrow start is a beginning, not an end state. The regulator chose maximum trust first, with the explicit expectation that breadth follows. Issuer density is only one of the execution risks Hong Kong still has to clear.

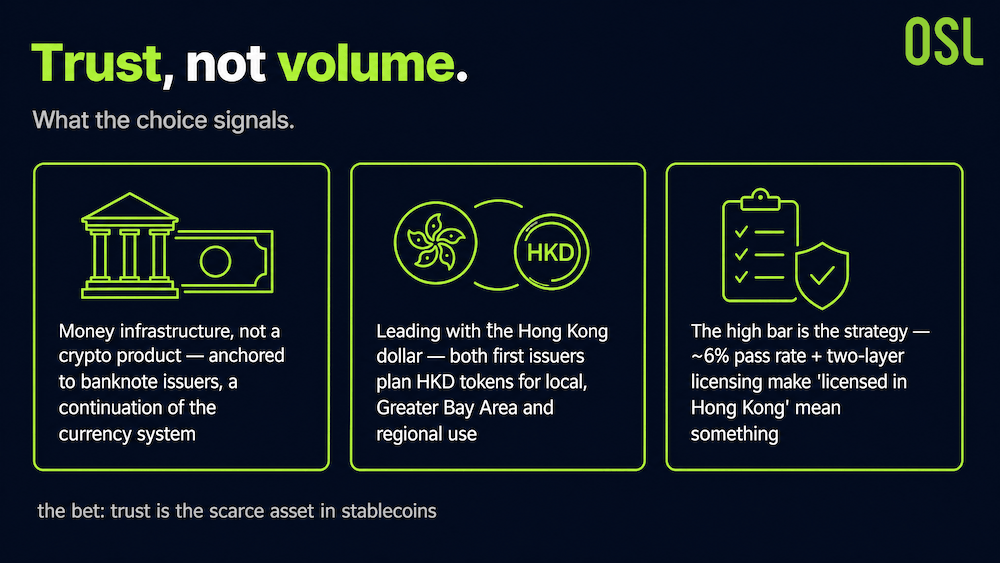

What It Signals

Reading the choice as a whole, three things stand out.

First, Hong Kong is treating stablecoins as money infrastructure, not as a crypto product. Anchoring the first licences to banknote issuers makes the digital token feel like a continuation of the currency system rather than a break from it.

Second, the city is leading with the Hong Kong dollar. Both first issuers plan HKD tokens aimed at local, Greater Bay Area, and regional commercial use, even though the larger international opportunity is in US dollar settlement.

Third, the high bar is the strategy. A 6% pass rate and a two-layer licensing structure are designed to make "licensed in Hong Kong" mean something to a corporate treasurer or a regulator elsewhere. The bet is that trust, not volume, is the scarce asset in stablecoins, and that the institutions already trusted to print the currency are the right place to start.

Chart 5: Three Indicators for Choosing a Stablecoin in Hong Kong

Frequently Asked Questions (FAQ)

Q1: How many stablecoin licences has Hong Kong granted, and to whom? Two, as of mid-2026. The HKMA granted issuer licences to HSBC (FRS02) and Anchorpoint Financial (FRS01) on 10 April 2026, both effective that day.

Q2: Why are the first licensees significant? Both are tied to Hong Kong's note-issuing banks. HSBC is one of the three banks authorised to print Hong Kong dollar banknotes, and Anchorpoint is led by Standard Chartered, another note-issuing bank. The regulator effectively started with the institutions already trusted to issue physical currency.

Q3: How selective was the first round? Very. The HKMA received 36 applications by the 30 September 2025 deadline and approved two, a pass rate of roughly 6%, after a six-month review.

Q4: What will the first stablecoins be denominated in? Hong Kong dollars. HSBC plans an HKD stablecoin in the second half of 2026, integrated into PayMe and the HSBC HK App. Anchorpoint plans phased issuance from Q2 2026 for cross-border payments, tokenised asset settlement, and supply chain finance.

Q5: Does an issuer licence cover everything? No. Issuing a stablecoin needs an HKMA licence under Cap. 656; distributing and trading it needs a separate SFC Virtual Asset Service Provider licence. A full-stack operator must hold both.

Related reading

Hong Kong's Dollar Peg Is a Stablecoin Superpower: The Dual-Anchor Hub Strategy — why the HK$7.80 peg and offshore-dollar depth make Hong Kong a natural USD-stablecoin clearing hub.

Hong Kong Won the Stablecoin Regulation Race. Now Comes the Hard Part — the five-item risk matrix standing between a licence and a working market.

References

This article is for information only and is not investment, legal, or tax advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

Latest

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Break down USDGO rewards across all tiers: estimated rewards at 10K, 50K, 100K+, new-user bonuses, VIP stacking, and payout schedule.

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

Hong Kong's first PI-exclusive compliant stablecoin rewards program. Hold USDGO and earn from daily snapshots: up to 80 USDGO for new users and up to 17,260 USDGO across tiers. 1:1 USD peg, zero fees, no lock-up.

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Recommended For You

More About Topics