A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The Advantage Hiding in an Old Peg

Most stablecoin coverage focuses on rules: who got licensed, which framework is toughest. Hong Kong's deeper edge is not regulatory at all. It is monetary, and it has been sitting in plain sight for four decades.

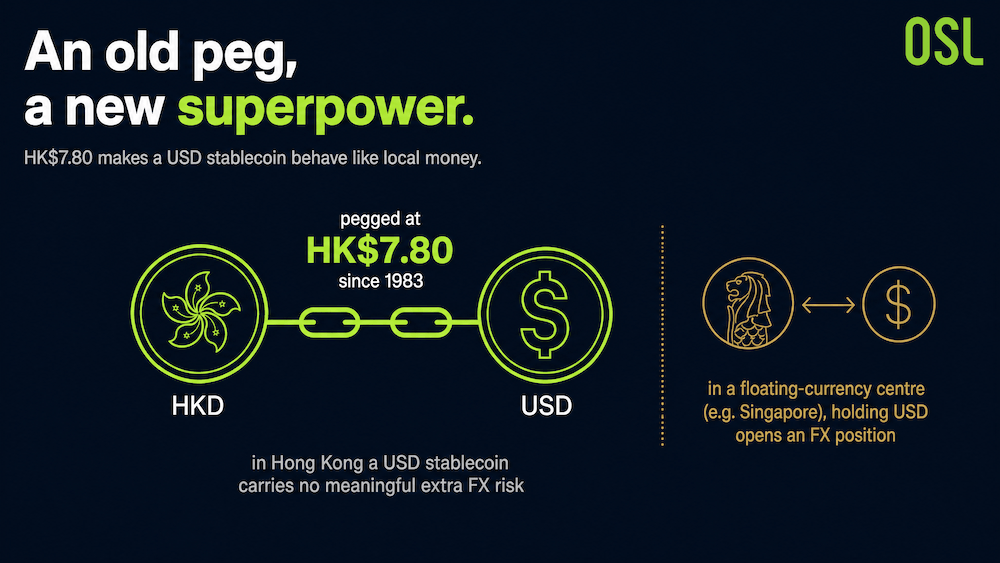

Since 1983, Hong Kong has run a Linked Exchange Rate System that pegs the Hong Kong dollar to the US dollar at HK$7.80. For a stablecoin hub, that peg does something specific and valuable: it lets a Hong Kong company hold a US dollar stablecoin like USDGO, USDC, or USDT without taking on meaningful currency risk against its home unit. The OSL × Hong Kong Polytechnic University report calls this a unique advantage that sets Hong Kong apart from other Asia-Pacific centres such as Singapore, where the local dollar floats and holding USD introduces an open FX position.

Chart 1: Advantages of Hong Kong’s 1983 Hong Kong Dollar–U.S. Dollar Pegged Stablecoin

Put plainly: in Hong Kong, a USD stablecoin behaves almost like domestic money. That is a quiet but real reason for a treasurer to clear dollars through Hong Kong rather than somewhere with a floating currency.

Deep Dollars, Not Just a Peg

The peg only matters because there are real dollars behind it. Hong Kong is one of the world's most important offshore US dollar markets, with a large base of USD deposits and a mature foreign exchange market. On top of that sits a developed ecosystem of physical transshipment trade, multimodal logistics, and professional services in audit, law, and offshore tax.

For stablecoin clearing, the plumbing is the point. Hong Kong's banking system holds some of the deepest offshore US dollar liquidity anywhere, and it runs mature real-time payment and interbank clearing infrastructure, the Faster Payment System (FPS) and CHATS, plus institutional clearing networks. That combination is what lets the report argue Hong Kong has the natural conditions to absorb large-scale USD stablecoin clearing for the region.

There is a demand signal to match. The report cites OSL's 2025 annual results, core operating revenue up 150% year on year, alongside a US$200 million funding plan to expand stablecoin trading infrastructure. The report reads that as a reflection of fast-growing institutional demand for USD stablecoins.

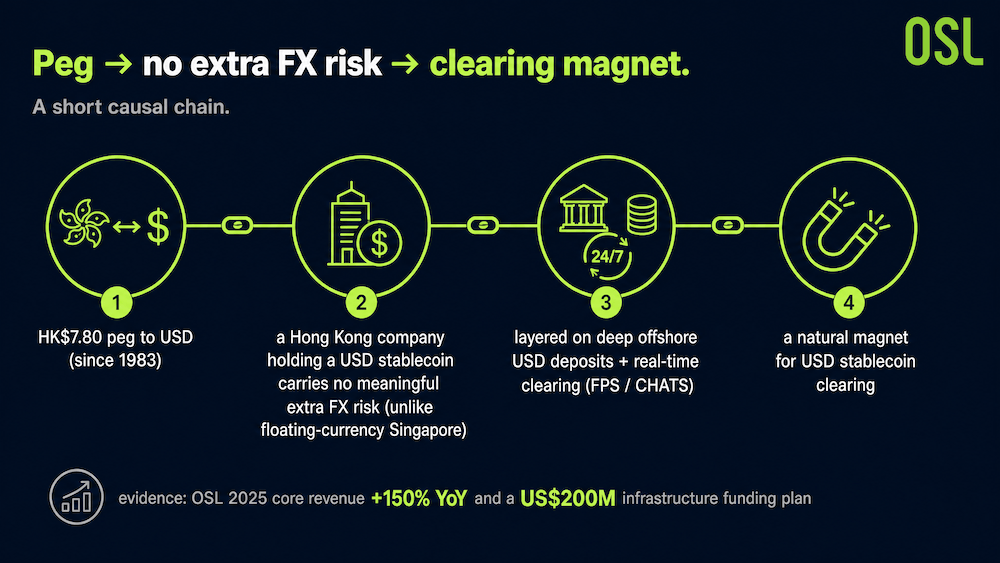

Chart 2: Why a USD stablecoin "feels local" in Hong Kong

The chain is short. Since 1983 the HK$7.80 peg has tied the Hong Kong dollar to the US dollar. Because of that, a Hong Kong company holding a USD stablecoin carries no meaningful extra FX risk against its home currency, unlike a company in a floating-currency centre such as Singapore. Layered on deep offshore USD deposits and real-time clearing rails (FPS/CHATS), that makes Hong Kong a natural magnet for USD stablecoin clearing. OSL's 150% year-on-year core revenue growth in 2025 and a US$200 million infrastructure funding plan are cited as evidence the demand is already arriving.

The Dual-Anchor Idea

Here is where Hong Kong's strategy gets distinctive. Rather than pick between a local-currency coin and a dollar coin, the report frames the goal as running both, a "dual-anchor" structure.

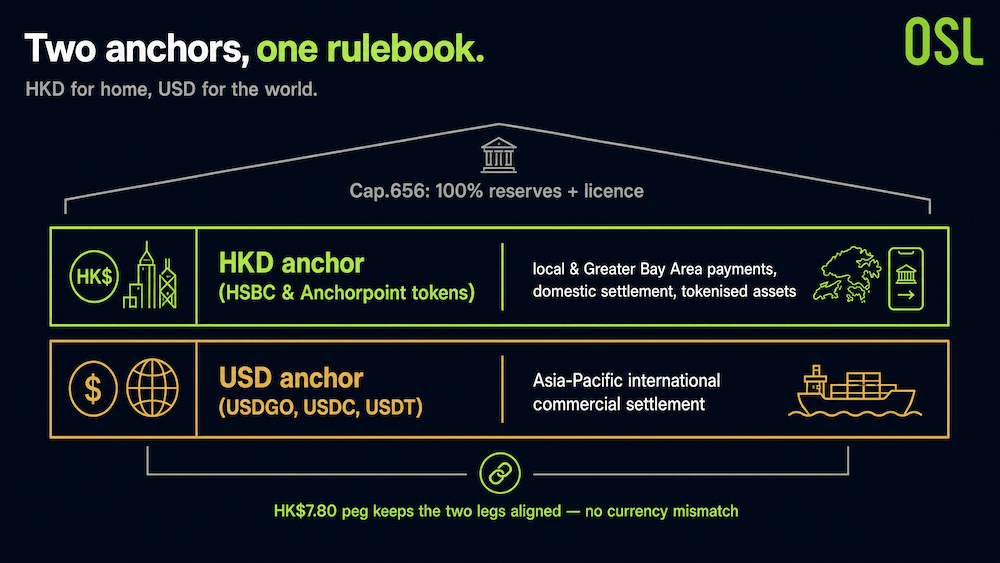

The two anchors do different jobs. HKD stablecoins, the tokens HSBC and Anchorpoint plan to launch, serve local Hong Kong and Greater Bay Area use cases: retail payments, domestic settlement, tokenised assets close to home. USD stablecoins (USDGO, USDC, USDT) carry the international leg, Asia-Pacific cross-border commercial settlement. Both must meet the same bar under the Stablecoins Ordinance (Cap. 656): 100% reserves and a licence.

The peg is what makes the two anchors complementary rather than competitive. Because HKD and USD move together, a business can use an HKD coin at home and a USD coin abroad without a destabilising currency mismatch between the two legs. The report's ambition is explicit: integrate the HKD's local strength with the USD's international settlement function to build a dual-anchor stablecoin hub for Asia-Pacific. Both HKD issuers are note-issuing banks, which is no accident, Hong Kong licensed its banknote issuers first for a reason.

Chart 3: The dual-anchor structure

Two anchors sit under one rulebook. The HKD anchor (HSBC and Anchorpoint tokens) serves local and Greater Bay Area payments, domestic settlement, and tokenised assets. The USD anchor (USDGO, USDC, USDT) carries Asia-Pacific international commercial settlement. Both are bound by Cap. 656's 100% reserve and licensing requirements, and the HK$7.80 peg keeps the two legs aligned so a company can move between them without a currency mismatch.

The Market Behind the Hub

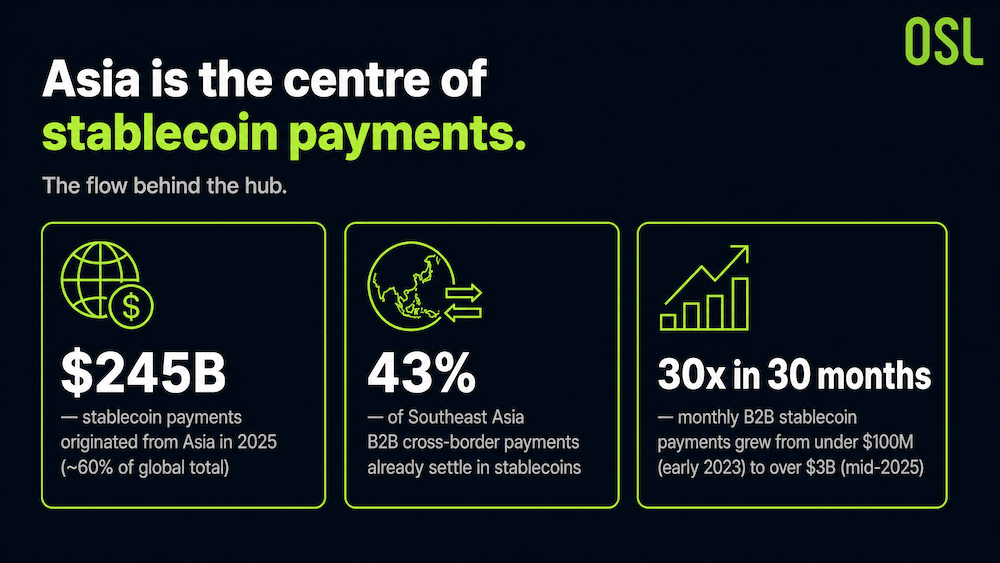

A clearing hub needs flow, and the regional numbers are large. Asia has become the centre of stablecoin payments: the report cites US$245 billion in stablecoin payments originated from Asia in 2025, about 60% of the global total (Crypto Briefing, 2025), and notes that 43% of B2B cross-border payments in Southeast Asia already settle in stablecoins (TazaPay, 2025). Monthly B2B stablecoin payments grew from under US$100 million in early 2023 to over US$3 billion by mid-2025, a 30-fold rise in 30 months.

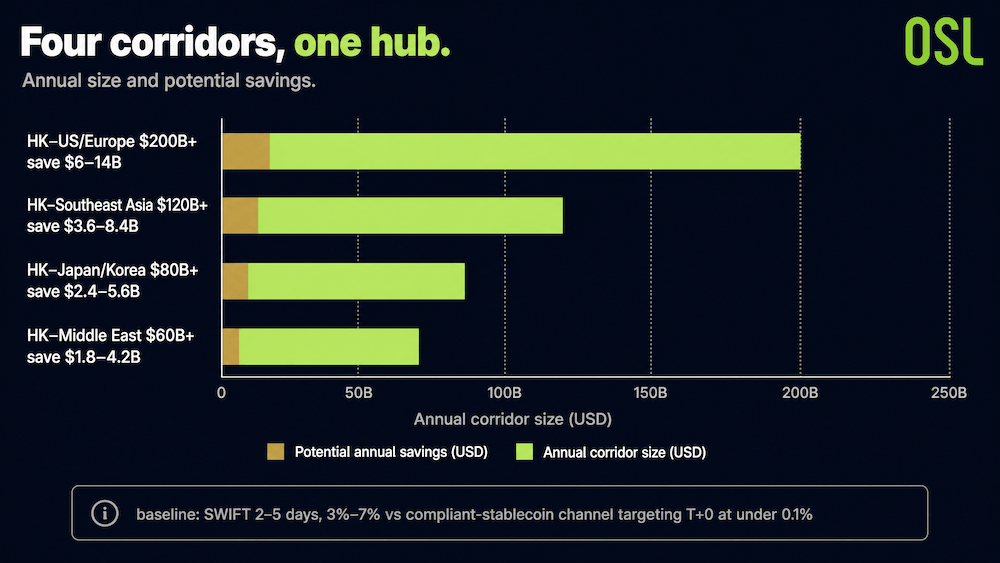

Hong Kong's pitch is to be the node that connects this flow. The report maps four core corridors anchored on Hong Kong, each with its own pain point and savings potential. Against a baseline where traditional SWIFT payments take 2–5 days and cost 3%–7%, the report contrasts a compliant-stablecoin channel (OSL BizPay) targeting T+0 settlement at under 0.1%.

Chart 4: Hong Kong's four key B2B corridors

The corridors vary in size and maturity. Hong Kong–US/Europe is the largest at over US$200 billion a year, institution-led, with cross-time-zone settlement and regulatory differences as the main friction, and an estimated US$6–14 billion in annual savings potential. Hong Kong–Southeast Asia runs over US$120 billion a year, where 43% of B2B already uses stablecoins, with multi-currency conversion and intermediary fees as the pain point and US$3.6–8.4 billion in potential savings. Hong Kong–Japan/Korea is over US$80 billion, held back by heavy compliance paperwork and settlement lag, with US$2.4–5.6 billion in potential savings. Hong Kong–Middle East is over US$60 billion and still early, constrained by FX controls and banking-hours mismatch, with US$1.8–4.2 billion in potential savings. The comparison baseline: SWIFT at 2–5 days and 3%–7%, versus a compliant-stablecoin channel targeting T+0 at under 0.1%.

Chart 5: Key Data Card on the Asia-Pacific Stablecoin Payments Market

What Could Still Go Wrong

The peg is an advantage, not a guarantee. The report is clear that institutional strength has to convert into commercial density within a window of roughly 18 to 24 months, or the first-mover lead erodes. These constraints are mapped in full in Hong Kong's stablecoin risk matrix.

The constraints are concrete. Hong Kong has only two licensed issuers so far, thin for a real clearing hub. Enterprise rules are unfinished: no published accounting treatment for stablecoin holdings, no settled cross-border tax reporting, no commercial-law certainty for stablecoin settlement. And the technology is fragmented, USDGO runs on Solana, USDC is multi-chain, and the planned HKD stablecoins have not disclosed their technical architecture, which leaves companies juggling multiple chains and bridges. The report names cross-chain interoperability standards as a key agenda item for the next 18 months.

None of these undoes the monetary edge. But they are the difference between having the right ingredients and serving the dish.

The Takeaway

Hong Kong's stablecoin case usually gets told through its law. The more durable story is monetary. A 1983 peg and a deep offshore dollar market mean a US dollar stablecoin can sit on a Hong Kong company's books almost like local cash, an advantage Singapore's floating dollar cannot match. Combine that with real-time clearing rails and a fast-growing regional payment flow, and the dual-anchor hub, HKD for home, USD for the world, stops sounding like a slogan and starts looking like a plan. Whether it works comes down to execution over the next two years, not to the peg, which is already doing its job.

Frequently Asked Questions (FAQ)

Q1: Why does Hong Kong's currency peg help with stablecoins? Because the Hong Kong dollar has been pegged to the US dollar at HK$7.80 since 1983, a Hong Kong company can hold a US dollar stablecoin without taking on meaningful extra currency risk against its home unit. In a floating-currency centre, holding USD opens an FX position.

Q2: What is the "dual-anchor" strategy? Running two kinds of stablecoin under one regulatory framework: HKD stablecoins for local and Greater Bay Area use, and USD stablecoins (USDGO, USDC, USDT) for Asia-Pacific international settlement. The peg keeps the two aligned.

Q3: How big is the Asian stablecoin payment market? The report cites US$245 billion in stablecoin payments originated from Asia in 2025, about 60% of the global total, with 43% of Southeast Asian B2B cross-border payments already settling in stablecoins.

Q4: How much cheaper could stablecoin corridors be than SWIFT? The report contrasts traditional SWIFT payments (2–5 days, 3%–7% fees) with a compliant-stablecoin channel targeting T+0 settlement at under 0.1%. Estimated annual savings range from US$1.8–4.2 billion on the Hong Kong–Middle East corridor to US$6–14 billion on Hong Kong–US/Europe.

Q5: What could stop Hong Kong from becoming the hub? Thin issuer density (only two licensees so far), unfinished enterprise accounting and tax rules, and cross-chain fragmentation. The report gives Hong Kong an 18–24 month window to turn its institutional lead into commercial scale.

Related reading

Hong Kong Gave Its First Stablecoin Licences to Banknote Issuers: Here's Why — how 36 applicants became two, and why the first licensees were the city's note-issuing banks.

Hong Kong Won the Stablecoin Regulation Race. Now Comes the Hard Part — the five risks between a regulatory lead and a working hub.

References

This article is for information only and is not investment, legal, or tax advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

Latest

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Break down USDGO rewards across all tiers: estimated rewards at 10K, 50K, 100K+, new-user bonuses, VIP stacking, and payout schedule.

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

Hong Kong's first PI-exclusive compliant stablecoin rewards program. Hold USDGO and earn from daily snapshots: up to 80 USDGO for new users and up to 17,260 USDGO across tiers. 1:1 USD peg, zero fees, no lock-up.

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Recommended For You

More About Topics