Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

First Is Not the Same as Done

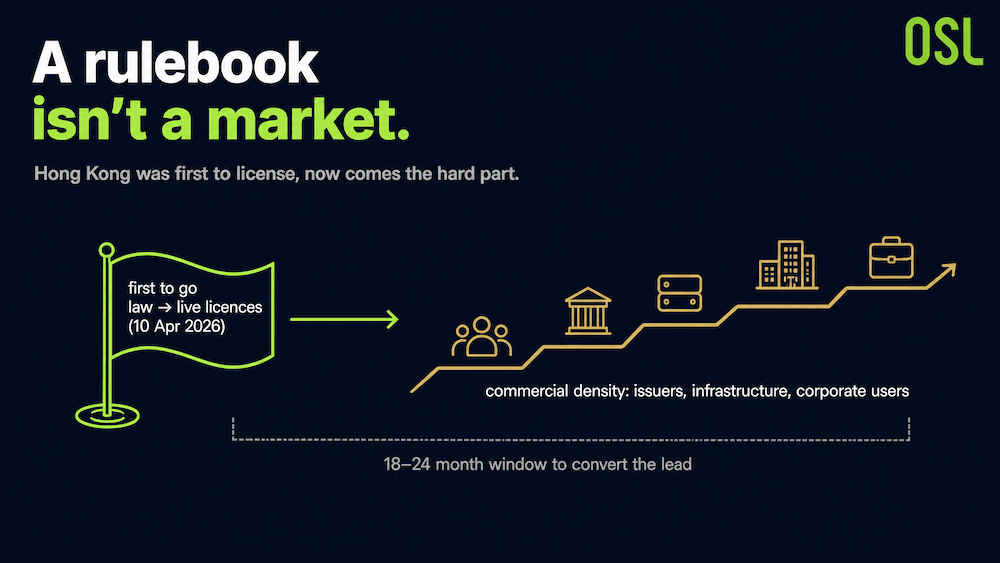

Being first to regulate gets the headlines. On 10 April 2026 the Hong Kong Monetary Authority granted the world's first fiat-referenced stablecoin issuer licences, the closing step of a process that began when the Stablecoins Ordinance (Cap. 656) took effect in August 2025. No other major centre has finished that loop. (For who got those licences and why, see the first two licensees and why they were chosen.)

Chart 1: Hong Kong's Stablecoin: “Legislate First, Then Develop the Market”

But the report is unusually honest about what comes next. Regulatory clarity, it argues, is only the first step. The real challenge is turning that clarity into commercial density, a working ecosystem of issuers, infrastructure, and corporate users deep enough to actually clear payments at scale. The report even prices the deadline: Hong Kong's institutional advantage has to become commercial density within 18 to 24 months, or the first-mover edge stops being sustainable.

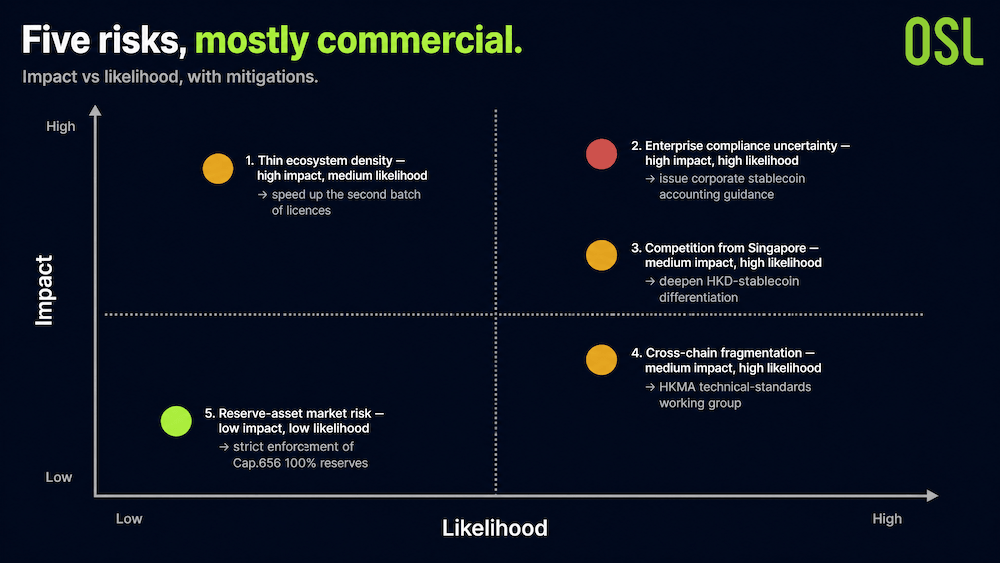

To its credit, the report names the obstacles directly, in a five-row strategic risk matrix. Here is what each one means.

Chart 2: Hong Kong Stablecoin Strategic Risk Heat Map

Source: Report: The Liquidity Hub of the Digital Economy (OSL × HKPU Faculty of Business)

The matrix rates five risks by impact and likelihood, each paired with a mitigation. Thin ecosystem density is high impact, medium likelihood; the mitigation is to speed up the second batch of licences. Enterprise compliance uncertainty is high impact, high likelihood; the mitigation is to issue corporate stablecoin accounting guidance. Intensifying competition from Singapore is medium impact, high likelihood; the mitigation is to deepen HKD-stablecoin differentiation. Cross-chain technical fragmentation is medium impact, high likelihood; the mitigation is an HKMA technical-standards working group. Reserve-asset market risk is low impact, low likelihood; the mitigation is strict enforcement of Cap. 656's 100% reserve rule.

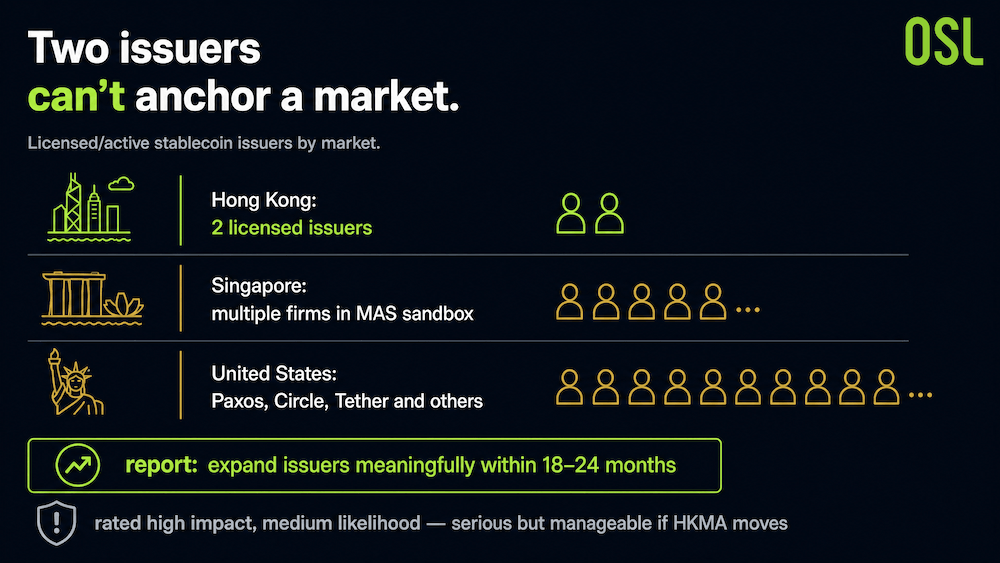

Risk 1: Too Few Issuers

The most immediate problem is also the simplest to state. Hong Kong has just two licensed stablecoin issuers, far below the density a mature payment system needs.

Compare the field. Singapore already has multiple firms inside the MAS regulatory sandbox. The United States has Paxos, Circle, Tether, and others in operation. Two issuers cannot anchor a competitive, multi-coin market, and a hub with only two issuers is fragile, concentration risk, limited choice, and little internal competition on price or features.

Chart 3: Cross-Market Comparison of the Number of Stablecoin Issuers

The report's mitigation is direct: speed up the second batch of licences and meaningfully expand the number of licensed issuers within 18 to 24 months. The matrix rates this risk high impact and medium likelihood, serious, but manageable if the HKMA moves.

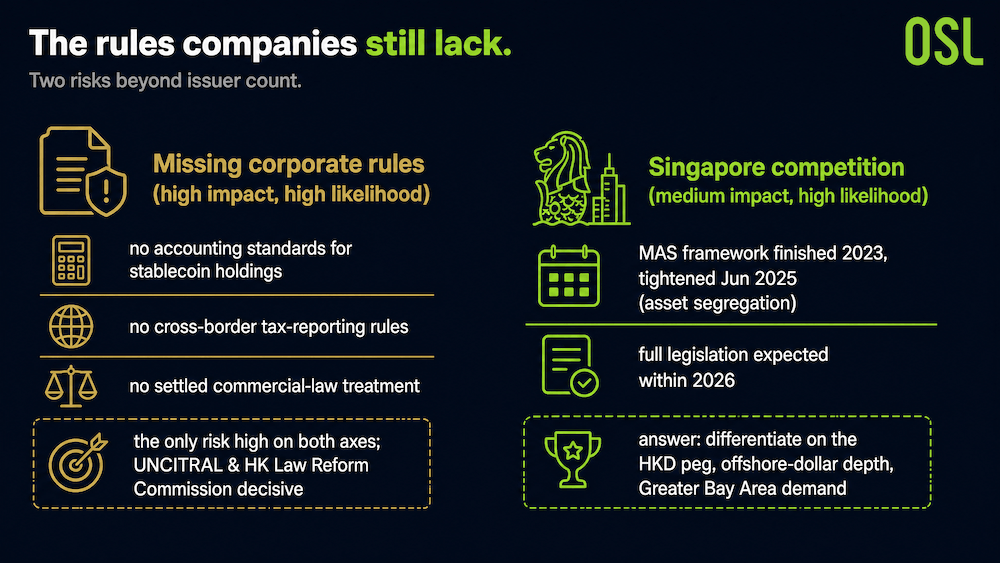

Risk 2: The Rules Companies Still Don't Have

This is the one most likely to bite, and it has nothing to do with stablecoin law itself. It is about the accounting, tax, and commercial-law plumbing that a finance team needs before it can use stablecoins in earnest.

Hong Kong has not yet published three things: accounting standards for how a company classifies stablecoin holdings on its balance sheet, tax-reporting rules for cross-border stablecoin flows, and settled commercial-law treatment for stablecoin settlement. Without those, a corporate treasurer cannot cleanly answer basic questions, how do I book this asset, what do I report, is this settlement final in law. The report calls these missing standards the main constraint on large-scale corporate adoption, and notes that work by UNCITRAL and Hong Kong's Law Reform Commission will be decisive.

The matrix rates this high impact and high likelihood, the only risk scored high on both axes. The mitigation, issuing corporate stablecoin accounting guidance, sits with standard-setters and law reformers more than with the HKMA alone, which is part of why it is hard.

Risk 3: Singapore Is Not Standing Still

Hong Kong's lead is real but not exclusive. Singapore finished its Single Currency Stablecoin framework back in 2023 and tightened it in June 2025 by mandating customer-asset segregation. Full stablecoin legislation is still being drafted and is expected within 2026. In other words, Singapore is close behind, and it is a credible alternative hub.

Chart 4: The Dual Risks of Lacking Corporate Governance and Competition in Singapore

The report's answer is differentiation rather than a pure speed race. Its suggested mitigation is to deepen the distinctiveness of HKD stablecoins, leaning on the things Singapore cannot easily copy: the Hong Kong dollar's peg to the US dollar, the city's offshore-dollar depth, and Greater Bay Area demand. That is the heart of Hong Kong's offshore-dollar and dual-anchor advantage. The matrix rates competition medium impact, high likelihood, less existential than the first two risks, but close to certain.

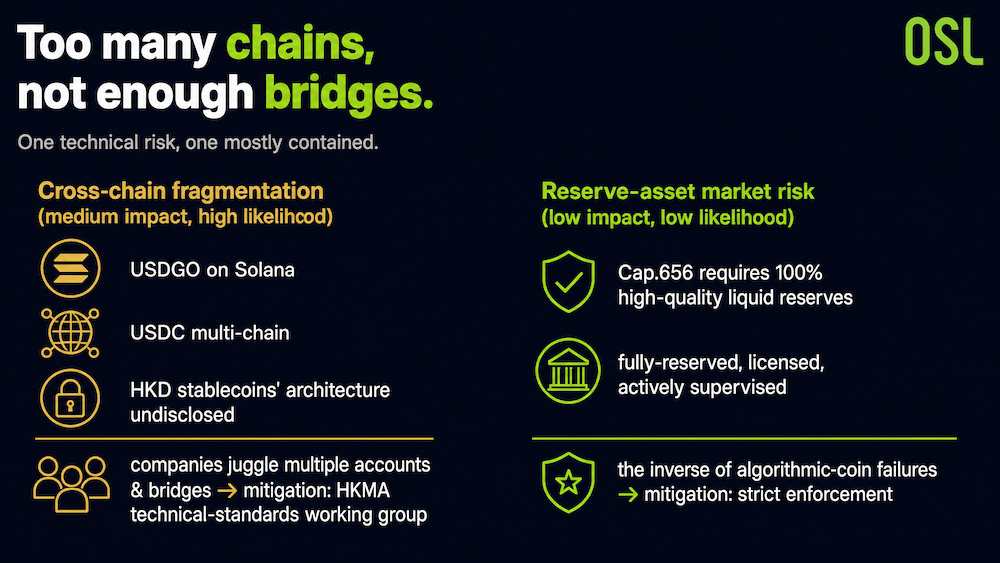

Risk 4: Too Many Chains, Not Enough Bridges

The next risk is technical. Today's stablecoins live on fragmented infrastructure. USDGO runs on Solana, USDC is multi-chain, and the planned HKD stablecoins have not yet disclosed their technical architecture.

For a company, that fragmentation is a real cost. Different chains that do not interoperate mean managing multiple on-chain accounts and several bridging protocols, which raises operational complexity and compliance overhead. A hub built on a tangle of incompatible chains is harder to use than the SWIFT system it hopes to improve on.

The report flags cross-chain interoperability standards as a key agenda item for the next 18 months, and its suggested mitigation is an HKMA technical-standards working group to push standardisation across the local ecosystem. The matrix rates this medium impact and high likelihood.

Risk 5: The Reserve Risk That's Mostly Handled

The last row is the one that worries the report least. Reserve-asset market risk, the danger that the assets backing a stablecoin lose value or liquidity, is rated low impact and low likelihood.

Chart 5: The Dual Risks of Cross-Chain Fragmentation and Reserve Risk

The reason it scores low is structural. Cap. 656 requires 100% reserves in high-quality liquid assets, and the mitigation is simply strict enforcement of that rule. This is the inverse of the algorithmic-stablecoin failures of earlier years: a fully-reserved, licensed coin under active supervision carries far less of this risk by design. It earns a place on the matrix for completeness, not because it is the thing to lose sleep over.

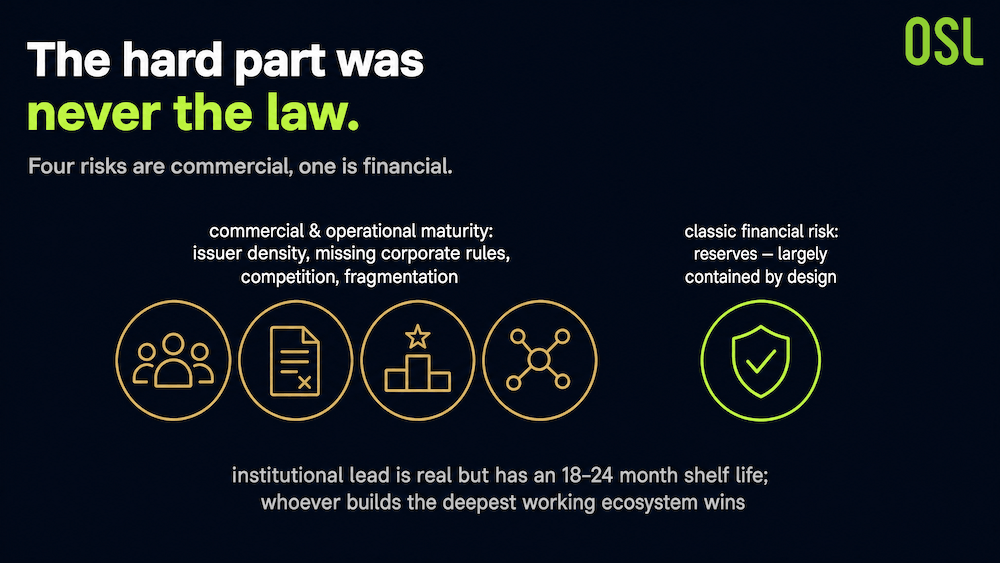

What the Matrix Really Says

Step back, and a pattern emerges. Four of the five risks, issuer density, missing corporate rules, competition, and fragmentation, are about commercial and operational maturity. Only the fifth is a classic financial risk, and that one is largely contained by design.

Chart 6: Risk Matrix Conclusions

That is the honest version of Hong Kong's stablecoin story. The hard part was never going to be the law, which Hong Kong finished first. The hard part is everything that turns a licence into a market a CFO will actually use: more issuers, real accounting rules, a differentiated product, and chains that talk to each other. The report's framing is clear-eyed, the institutional lead is real, but it has a shelf life of 18 to 24 months. After that, whoever has built the deepest working ecosystem wins, not whoever legislated first.

Frequently Asked Questions (FAQ)

Q1: What are the main risks to Hong Kong's stablecoin ambitions? The report lists five: thin issuer density, missing corporate accounting and tax rules, competition from Singapore, cross-chain fragmentation, and reserve-asset market risk. Four of the five are about commercial maturity rather than regulation.

Q2: Which risk is most serious? Enterprise compliance uncertainty. It is the only risk the report rates high on both impact and likelihood, because Hong Kong has not yet published accounting, tax, or commercial-law rules for corporate stablecoin use.

Q3: How many licensed stablecoin issuers does Hong Kong have? Two, as of mid-2026, far below what the report says a mature payment system needs. By comparison, Singapore has multiple firms in its MAS sandbox and the US has Paxos, Circle, and Tether among others.

Q4: Why is cross-chain fragmentation a problem? USDGO runs on Solana, USDC is multi-chain, and the HKD stablecoins' architecture is undisclosed. Without interoperability, companies must manage multiple on-chain accounts and bridges, raising operational and compliance costs.

Q5: How long does Hong Kong have to act? The report gives an 18 to 24 month window to convert its institutional lead into commercial density before the first-mover advantage erodes.

Related reading

Hong Kong Gave Its First Stablecoin Licences to Banknote Issuers: Here's Why — the selection logic behind the first two licences.

Hong Kong's Dollar Peg Is a Stablecoin Superpower: The Dual-Anchor Hub Strategy — the offshore-dollar edge that underpins Hong Kong's differentiation.

References

This article is for information only and is not investment, legal, or tax advice.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

Latest

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Break down USDGO rewards across all tiers: estimated rewards at 10K, 50K, 100K+, new-user bonuses, VIP stacking, and payout schedule.

USDGO Rewards Calculator: How Much You Hold, Estimated Rewards, How to Collect

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

Hong Kong's first PI-exclusive compliant stablecoin rewards program. Hold USDGO and earn from daily snapshots: up to 80 USDGO for new users and up to 17,260 USDGO across tiers. 1:1 USD peg, zero fees, no lock-up.

USDGO Premium Rewards Program: Hong Kong's First PI-Exclusive Compliant Stablecoin Rewards Program

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Recommended For You

More About Topics