Stablecoin Payment Weekly No. 13 Navigating the Path to B2B Cross-Border Settlement Amidst the Digital Payment Surge

Author of this Issue:

Kelly Wang, Junior Analyst at OSL Research

Email: [email protected]

I. Weekly Stablecoin Payment Data

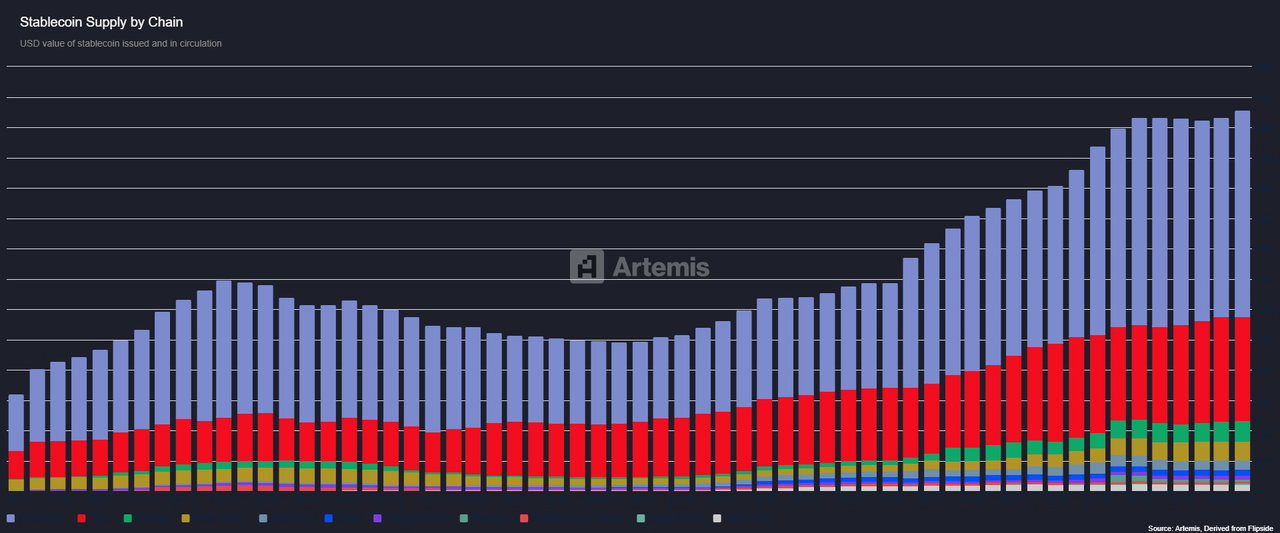

As of 2026-03-26 (7-day rolling basis), the total market capitalization/supply of stablecoins is approximately $336.1 billion, effectively breaking through the $300 billion milestone.

Messari monitoring shows: Stablecoin transfers remain highly active, with a cumulative transfer volume exceeding $8.49 trillion over the past 30 days. Daily fluctuations stay within the $280 billion to $285 billion range. Extrapolated by daily average, the total transfer volume for the past 7 days is between $1.8 trillion and $2 trillion.

OSL Research adjusted volume: After filtering out "noise" such as market making, wash trading (self-trading), and bot activity, the "effective" volume accounts for approximately 20% of the total, corresponding to a scale of roughly $360 billion to $400 billion over the past 7 days.

(Data Sources: Messari, Artemis, OSL Research)

("Effective" = Adjusted data excluding noise from market making, self-trading, and bots.)

Top 3 Stablecoin Protocols by Market Cap Growth This Week

Monerium EUR emoney (+6.9%; Weekly transfer volume $1.57M, +56.00%)

USDtb (+6.5%; Weekly transfer volume $225M, +45.10%)

MetaMask USD (+5.67%; Weekly transfer volume $46.37M, -22.46%)

OSL Research Growth Observations:

1. Monerium EUR emoney (EURe): Market cap grew by 6.9% this week. As a regulated electronic money issued by an authorized Electronic Money Institution (EMI) in Iceland, it is pegged 1:1 to the Euro and supports minting via SEPA bank transfers, Web3 IBANs, or APIs. Assets are backed by over-collateralized high-liquidity assets (cash/treasuries). Its advantage lies in SEPA Instant transfers (<60s with zero fees), driven primarily by Eurozone payment demand.

2. USDtb: Grew by 6.5% this week, issued by Ethena Labs. 90% of reserves are invested in BlackRock BUIDL (USD cash/treasuries/repos). Its core advantage stems from the yield provided by BUIDL and the brand endorsement of BlackRock/BNY Mellon. Funds are mainly used for DeFi collateral and CEX integration (e.g., Bybit).

3. MetaMask USD (mUSD): Grew by 5.67%, issued by Bridge (a Stripe subsidiary) and supported by the M0 protocol. Minted natively via the MetaMask wallet, its core momentum comes from MetaMask Card spending (1-3% cashback) and Aave market rewards, making it popular among retail wallet users.

II. Weekly Stablecoin Payment & Infrastructure Highlights

1. Visa Report: Non-USD Stablecoins Become Mainstay of Cross-Border Payments Summary:

A joint report by VISA and Dune notes that non-USD stablecoins are accelerating into the "local currency" of the crypto ecosystem. Use cases have shifted from DeFi to cross-border payments, B2B settlements, and FX management. As of February this year, non-USD stablecoin supply reached $1.1 billion, a 3x increase from early 2023, with transfer volumes surging 1600% to $10 billion.

Source: The Block (2026/03/25)

Observation: Non-USD stablecoins are upgrading from fringe experiments to actual settlement anchors. Their core application has detached from yield-seeking and moved toward real capital flows. This implies a structural erosion of the monopoly pricing power of USD stablecoins, with institutional treasuries and corporate wallets becoming the primary liquidity pools.

2. Clarity Act Compromise Triggers Divergence; Coinbase Dissatisfied with Yield Clauses Summary:

U.S. Senators proposed a compromise on the stablecoin yield portion of the Clarity Act this week, eliciting varied reactions. Coinbase expressed dissatisfaction to Senate staff regarding the latest compromise text, though no public opposition has been declared. The proposal was presented to stakeholders on Monday; some expressed dissatisfaction, while others found the result better than expected. The proposal would direct certain regulators to define rules for yield-bearing activities, raising industry concerns about subjective standards. Additionally, the text may restrict companies' ability to link rewards to stablecoin transaction volume. During a call this week, Coinbase diverged from others; some firms felt giving up certain rewards was too costly, while others felt losing the overall Clarity Act framework posed a greater risk. Previously, news of the compromise impacted the market, with Circle's stock falling 20% on Tuesday before recovering slightly on Wednesday. White House Crypto Advisor Patrick Witt criticized related predictions on X as "uninformed," stating "everything will be fine." The final text is expected late this week or early next week.

Source: CoinDesk (2026/03/26)

Observation: Restrictions on reward mechanisms in the CLARITY Act will pose a clear headwind for Circle’s short-term circulating supply expansion, especially after reward-driven holding incentives are cut. Secondary market liquidity may see a temporary contraction, but Circle's core revenue still relies on reserve interest sharing with channel partners like Coinbase, avoiding direct regulatory impact. This policy essentially creates a firewall between deposit-like yields and payment incentives, forcing issuers to accelerate their shift from a "bank-like" model to a pure transaction-driven ecosystem. In this game, the existing networks of Circle and its partners may actually strengthen their moats rather than lose ground to pure DeFi competitors.

3. Revolut Processes Over $1.2 Billion in Cross-Border Stablecoin Transfers via Polygon Summary:

Polygon announced that Revolut’s on-chain transaction volume surpassed $1.2 billion. This European fintech giant is deepening its blockchain commitment. Revolut previously applied to the OCC and FDIC for a U.S. National Bank Charter to operate as Revolut Bank US, NA. If granted, Revolut will have direct access to Fedwire and ACH, offer FDIC-insured deposits, and operate in all 50 states under a unified federal framework.

Source: Polygon (2026/03/26)

Observation:Traditional cross-border payment traffic is quietly shifting to low-cost Layer 2 tracks, validating Polygon's capacity and economic model in real-user scenarios. For institutions, this marks fintech giants moving beyond surface-level integration to embedding blockchain into core payment paths, squeezing the margins of legacy systems like SWIFT. This milestone complements Revolut's bank charter application: the combination of on-chain efficiency and federal licensing creates a hybrid architecture for both retail and institutional flows. Approval would allow seamless switching between USD stablecoins and global/local systems via Fedwire, ACH, and Polygon, significantly increasing strategic depth.

4. Bitget Wallet Launches Onchain Payments Matrix for Global Infrastructure Summary:

Bitget Wallet officially released its global payment infrastructure, "Onchain Payments Matrix," designed to provide a unified payment and settlement architecture for humans and Agents. It aims to bridge traditional finance with on-chain systems and promote stablecoin adoption in daily finance and the Agentic Economy. The matrix consists of five layers: Clearing & Settlement, Asset & Value, Account & Identity, Orchestration & Coordination, and Application & Distribution. It integrates stablecoin issuers, blockchains, card networks, banks, and ramps. It supports Agent-native accounts, programmable authorization, and automated payments, allowing Agents to settle within preset strategies. Partners include Ripple, Mastercard, Visa, Tether, Circle, and MoonPay.

Source: The Block (2026/03/24)

Observation: Support for Agent-native accounts and automated payments lowers friction and decentralizes settlement sovereignty. Bitget has upgraded the wallet from a tool to an Agent-driven payment hub, positioning itself for future traffic and data sovereignty. While partnerships with Ripple, Mastercard, and Visa strengthen the TradFi-on-chain bridge, multi-party coordination for clearing and ramps still faces regulatory and liquidity fragmentation. Success depends on Bitget's on-chain volume and institutional adoption curves.

5. Tether Pauses $20 Billion Financing Plan Awaiting Audit Results Summary:

Stablecoin issuer Tether Holdings SA has paused a previously planned $20 billion capital raise while awaiting the results of its first comprehensive financial audit. Sources reveal that potential investors and bankers have been urging Tether to improve transparency. Some investors reportedly remain ready to support the firm even before the results.

Source: Bloomberg (2026/03/25)

Observation: This is essentially a final standoff between institutional capital and reserve veracity. Relying on quarterly attestations no longer meets the due diligence thresholds of large LPs and banks, exposing the tension between Tether's scale and its connection to traditional finance. Choosing a "Big Four" audit at this critical junction shows management realizes that without a verifiable balance sheet, large capital injections will carry high governance premiums. Continued investor interest highlights USDT's indispensability in liquidity networks, but it also means investors are trading low transparency for early-entry premiums.

6. Ripple Tests RLUSD-Driven Trade Finance in Singapore Summary:

Ripple announced participation in the Monetary Authority of Singapore’s (MAS) BLOOM initiative to test RLUSD stablecoin applications in cross-border trade payments within a regulatory sandbox. Partnering with supply chain finance provider Unloq, they are piloting a system on the XRP Ledger. When preset conditions (e.g., shipping verification) are met, RLUSD automatically triggers payment, replacing traditional manual verification and correspondent banking. The pilot uses Unloq’s SC+ platform to integrate obligations, settlement, and financing into a single execution layer.

Source: CoinDesk (2026/03/25)

Observation: By integrating trade obligations and settlement into one layer, Ripple dismantles the manual verification chains of correspondent banks. This can shift cross-border timing from T+3 to near-real-time. This pilot builds a moat of Asian licenses and native blockchain settlement, aiming to seize the compliant entry point for institutional trade finance and force legacy banks to yield inefficient segments.

7. Cloudflare Competes with Coinbase/Zerohash for NET Dollar Issuance Rights Summary:

Sources reveal that Coinbase and Zerohash are competing to be the issuer for Cloudflare’s upcoming "NET Dollar" stablecoin, set to launch later this year. NET Dollar is designed for seamless transactions in "Agentic Networks," where autonomous AI agents browse, negotiate, and settle payments independently. Cloudflare plans to embed stablecoin functionality directly into network infrastructure for efficient micropayments in AI-driven content access, data processing, and automation.

Source: Crowd Fund Insider (2026/03/20)

Observation: An edge computing giant embedding stablecoins into global CDN and proxy infrastructure aims to provide a native USD anchor for AI Agent micropayments, bypassing existing payment stack friction. NET Dollar marks the evolution of stablecoins from storage tools to the native settlement layer of the next-generation internet, lowering costs for AI-driven services and building Cloudflare's moat in the Agentic Economy.

8. Circle Calls on EU to Accelerate DLT Reform and Relax Stablecoin Settlement Rules Summary:

Circle has urged the EU to speed up digital asset regulatory reforms, arguing that current progress may slow institutional adoption of tokenized markets. In feedback to the EU "Market Integration Proposal," Circle called the plan an important step but noted deficiencies in scalability, regulatory mechanisms, and settlement rules. Circle supports optimizing DLT pilot frameworks, increasing asset scope and transaction limits, and suggested a "dynamic threshold" mechanism for automatic regulatory adjustments rather than periodic legislative updates.

Source: The Block (2026/03/24)

Observation: Circle's public feedback is a push against regulatory lag in the tokenization space. Deficiencies in current frameworks directly hinder institutional adoption. Circle's proposed "adaptive governance" aims to reduce uncertainty in transitioning from pilots to formal systems, accelerating capital migration from legacy securities infrastructure to DLT.

III. Weekly Regulatory & Policy Signals

1. Hong Kong: Exploring Digital RMB Wallet Upgrades; Recognizing Stablecoin Potential Summary:

Secretary for Financial Services and the Treasury Christopher Hui responded to HK stablecoin and e-CNY development, stating that the number of e-CNY wallets registered with HK mobile numbers is growing steadily, reaching 80,000 by late January. The PBoC and HKMA are exploring wallet upgrades to increase limits and expand use cases. He stated that stablecoins, CBDCs, tokenized deposits, and FPS cross-border links have the potential for settlement and payment scenarios under compliant frameworks.

Source: HKSAR Government Press Release (2026/03/25)

Observation: While 80,000 wallets represent an early stage, this is a strategic test of cross-border infrastructure between the HK government and the PBoC. The goal is to pave the way for stablecoin-CBDC hybrid applications rather than just retail penetration. By recognizing the potential of these tools, HK is building a differentiated competitive advantage with compliance as a shield to avoid being marginalized in US-China fintech competition.

2. South Korea: Stablecoin Skeptic Shin Hung-song Nominated as Central Bank Governor Summary:

President Lee Jae-myung nominated BIS Monetary and Economic Dept head Shin Hung-song as Governor of the Bank of Korea. Last August, Shin called KRW stablecoins a "shortcut to bypassing FX controls" and a potential channel for capital flight. He resigned from the BIS immediately after the nomination. While Lee Jae-myung made KRW stablecoin issuance a campaign issue, the central bank has blocked legislation for months. BIS reports state stablecoins lack stable currency functions and pose risks to monetary sovereignty.

Source: DLNews (2026/03/23)

Observation: This marks a public showdown between the Presidency and the central bank over monetary sovereignty and capital controls. Shin's immediate resignation from the BIS, paired with Lee's campaign promises, suggests the government intends to break legislative resistance through personnel changes. Shin's term may move Korea from "blocking" to "controlled pilots," which would be a high-stakes experiment for an emerging market against the USD stablecoin dominance.

3. USA: CFTC Clarifies Capital Requirements for Crypto Assets as Collateral Summary:

The CFTC issued detailed guidance for a pilot on crypto as collateral. Key points: 1. Capital requirements: Only BTC, ETH, and stablecoins are accepted. BTC/ETH have a 20% capital charge; stablecoins are 2%. 2. Limited use: Only dedicated payment stablecoins in client segregated accounts are allowed. 3. Clearinghouses: Only those meeting CFTC credit, market, and liquidity risk requirements can accept crypto as initial margin.

Source: ChainCatcher (2026/03/03)

Observation: This guidance opens a controlled valve for institutional BTC/ETH exposure in the clearing chain. A 2% haircut for stablecoins defines the boundary for capital arbitrage. Restricting use to segregated accounts prevents systemic risk from leaking into uncleared swaps. This means only large clearinghouses with mature risk models can access this new margin pool, further marginalizing small players and increasing industry concentration.

IV. Analyst Commentary: The Path to Breakthrough for Stablecoin B2B Cross-Border Settlement

By Kelly Wang, Junior Analyst at OSL Research

Email: [email protected]

Industry Status: The B-End Becomes the Core Use Case

As of March 2026, global stablecoin market cap has reached $336 billion, with the top five protocols holding over 89% market share. USDT maintains dominance with 58% share, while USDC leads in institutional transactions due to compliance. Stablecoins are rapidly moving beyond crypto trading into the real economy. In 2025, total transfers exceeded $33 trillion, with B2B payments surging to 60%. This trend is driven by differences in transaction attributes, pain points, and commercial value between B-end and C-end; B2B supplier settlement has become the first area for large-scale, high-value adoption.

Core Logic for B-End First: Why Stablecoins Land in B2B Rather Than C-End

The B2B-first/C-end-lagging pattern results from differences in cost-benefit, decision-making, compliance, and pain point rigidity.

From a cost-benefit perspective, B2B transactions are high-value and frequent. Traditional wire fees are 3%-7%, leading to massive loss in fees and interest on in-transit funds. Stablecoins compress fees to under 1% and free up capital, offering rich, direct returns. Conversely, C-end amounts are small and absolute fee savings are too low to offset the learning curve and risk for individuals.

In decision-making, B2B is driven by professional finance teams with efficiency as a KPI. It is rational and scalable. C-end users are scattered with varying levels of trust, making adoption costs exponential.

In compliance, B2B settlement is backed by real trade contracts and invoices, making it easier for regulators to verify. C-end transfers are often complex and risk triggering FX control or money laundering red lines, leading to stricter oversight.

Regarding pain point rigidity, long cycles and high fees in traditional B2B settlement directly stress corporate cash flow and supply chains—this is a survival issue. For C-end, high fees and delays are merely a bad user experience, making B-end the priority.

Positioning Boundaries: Complementary Layer Rather Than Replacement

Stablecoins are positioned as an efficient middle layer, not a replacement for banks. This is the optimal solution dictated by compliance, division of labor, and commercial trust.

Legally, fiat storage and large-scale clearing must be done by licensed banks. Stablecoin issuers generally lack bank charters and must act as auxiliary tools. Functionally, banks and stablecoins complement each other. Banks handle fund safety, AML, and credit backing; stablecoins provide 24/7 peer-to-peer transmission to fix efficiency gaps. In trust, companies keep core funds in banks for insurance and regulation, using stablecoins only as an FX/transfer bridge to control risk.

Finance departments, as the requesters, measure settlement efficiency and cost. Only a clear ROI triggers a project. Compliance departments hold veto power, checking issuance, FX compliance, and traceability to ensure AML standards. IT departments evaluate API difficulty and deployment cycles, preferring lightweight solutions. Risk management monitors liquidity and FX volatility, setting limits to prevent losses. This chain requires stablecoin products to be compliant, transparent, and easy to integrate to pass corporate approval.

Cost Structure Breakdown: Comprehensive Optimization of Explicit and Implicit Costs

Stablecoin value lies in eliminating high implicit costs.

Traditional Wire (Total cost 3%-7%): Explicit fees (remitting, intermediary, and receiving banks) total 1%-3%. FX spreads are wide (1%-3%). Implicit costs from 1-5 day settlement cycles account for 0.05%-0.1% in interest. Operational costs (reconciliation, manual audit) add 0.5%-1%.

Stablecoin Settlement (Total cost 0.8%-1.2%): Explicit fees (fiat-stablecoin conversion and gas) are 0.5%-0.9%. FX spreads use real-time market rates (0.1%-0.2%). Near-instant arrival makes in-transit costs zero. Smart contracts reduce manual operation to under 0.1%. For high-volume firms, the annual savings far exceed the simple fee difference.

OSL BizPay: A Practice in Compliant Implementation for Institutional Stablecoin Infrastructure

OSL BizPay adheres to this logic by acting as a middle layer that optimizes efficiency without disrupting the banking system.

Its positioning is clear: “Cross-border payments don’t need new use cases. They need better infrastructure.” BizPay builds a compliant bridge between Web2 and Web3, focusing on upgrading existing processes rather than creating new ones. It focuses on three scenarios: trade settlement, global treasury movement, and emerging market corridors. It is driven by the compliant institutional stablecoin USDGO, supporting instant fiat-to-stablecoin conversion.

Through the “stablecoin sandwich” model—using stablecoins as an efficient middle layer to eliminate multi-party inefficiency—BizPay reduces 3-5 day cycles to 2-5 minutes with 24/7 service. Total fees drop from 3-7% to 0.8-1.2%. Technically, it includes on-chain safety abstraction, gas management, and an internal OTC desk for a seamless experience. Its API is integrated with leading Asia-Pacific partners, supporting corridors like Africa-Europe and Africa-HK.

Crucially, BizPay can be integrated in as little as two weeks, lowering the barrier for entry. It addresses real pain points: compliance friction, high costs, and low efficiency. By leveraging USDGO, BizPay is helping global firms turn stablecoins into daily operational infrastructure.

Stablecoin-driven B2B settlement is becoming a reality for optimizing cash flow. It helps stablecoins serve the real economy and provides a clear track for application innovation. In 2026, as volumes grow, this field will contribute more sustainable activity. Over the coming months, we will monitor B2B growth, corporate use cases, and multi-chain routing in supply chains. Success in this track requires staying compliant, focusing on real customer pain points, and refining practical products.

Disclaimer and Disclosure

1. Nature of Document

This document (“Document”) has been prepared solely by internal personnel of OSL for informational purposes. It does not constitute investment, legal, tax, or other professional advice and should not be relied upon as such. No part of this Document may be reproduced, distributed, or transmitted to any third party in any form without the prior written consent of OSL.

This Document does not constitute an offer, solicitation, marketing material, product disclosure, or legal document, nor does it form the basis of any binding contract or commitment. It is intended solely to provide OSL’s observations and strategic insights on the industry and does not represent OSL’s official opinions, strategies, or decisions.

The authors are not independent research analysts, and this Document does not constitute “investment research” as defined under applicable laws and regulations. Accordingly, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any pre-dissemination trading restrictions.

2. Non-Reliance

The information, opinions, and analyses contained herein are based on publicly available information and OSL’s internal judgment. They do not take into account the individual objectives, financial circumstances, or needs of any recipient. This Document is not a personal recommendation or solicitation to buy, sell, or otherwise transact in any financial instrument, product, or service.

Before making any investment or other decision, recipients must consult their own independent advisors, considering their individual circumstances, objectives, experience, and resources. All investments involve risk; values may fluctuate, and investors may receive less than the original invested amount. Past performance is not indicative of future results.

3. Accuracy, Completeness, and Limitation of Information

This Document is based on information that OSL considers reliable; however, OSL has not independently verified its accuracy, completeness, or fairness. Reasonable care has been taken to ensure that the content is not false or misleading, but OSL makes no representation or warranty, express or implied, regarding its accuracy, completeness, fairness, or reasonableness.

OSL is not responsible for any errors, omissions, or consequences arising from reliance on third-party information referenced herein. Performance of any discussed instruments, entities, or strategies may be materially affected by market, regulatory, technical, or other factors.

4. Forward-Looking Statements

This Document may contain forward-looking statements that involve known and unknown risks, uncertainties, and other factors. Actual results, performance, or achievements may differ materially from those expressed or implied. OSL does not undertake any obligation to update, revise, or withdraw any forward-looking statements.

5. Conflicts of Interest

OSL, its affiliates, and employees may hold positions in, or engage in transactions involving, the assets or entities discussed herein. The authors or other personnel involved in the preparation of this Document may receive compensation that is linked to the performance of OSL’s business. OSL has implemented policies and procedures to identify and manage potential conflicts of interest.

6. Intellectual Property and Restrictions on Use

This Document is protected by copyright and is intended solely for the designated recipient. Recipients may store, display, analyze, modify, reformat, and print this Document for their own internal use only. Recipients may not, without OSL’s prior written consent:

Resell, redistribute, or commercially exploit this Document;

Reverse engineer, extract, or create derivative works, including for training or use in machine learning/artificial intelligence systems;

Publish or transmit this Document to third parties

7. Limitation of Liability

To the maximum extent permitted by applicable law, OSL, its affiliates, officers, employees, and agents shall not be liable for any direct, indirect, incidental, consequential, or special damages arising from or in connection with the use of, reliance upon, or interpretation of this Document, including but not limited to:

Loss of profits;

Business interruption;

Data loss;

Reputational harm.

8. Global Distribution Notes

Recipients are responsible for compliance with local laws. Distribution of this Document may be restricted in certain jurisdictions. Recipients must ensure that it is not distributed to any person or entity to whom such distribution would be unlawful.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

India's RBI wants banks out of crypto. The real issue is whether compliance is even possible.

India's RBI is not just tightening crypto rules. It is removing the institutional path to compliant participation.

India's RBI wants banks out of crypto. The real issue is whether compliance is even possible.

BNB's million-TPS AI chain raises the compliance question institutions cannot skip

BNB Chain's new AI-agent Layer 1 puts speed in the spotlight, but institutional adoption still depends on settlement certainty, transparency, and liability design.

BNB's million-TPS AI chain raises the compliance question institutions cannot skip

After GENIUS, Brussels wants to set the rules non-EU stablecoins must build to

The EU is using MiCA 2.0 to define how non-EU stablecoin issuers, tokenized deposits, and payment tokens reach European users after GENIUS.

After GENIUS, Brussels wants to set the rules non-EU stablecoins must build to

The Crypto Exchange Wants to Be Your Only Account

Crypto exchanges are adding stocks, options and AI advisors to become super apps. They're not after your next trade, but your whole account, and its risks.

The Crypto Exchange Wants to Be Your Only Account

"Not a Derivative. Not an IOU." Why a CEO Had to Say the Quiet Part Out Loud

A token can carry a stock's ticker and price yet grant none of a shareholder's rights. The three structures behind tokenized stocks, and what you really own.

"Not a Derivative. Not an IOU." Why a CEO Had to Say the Quiet Part Out Loud

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Visa and Mastercard announced AI-powered payment solutions on the same day, both designating stablecoins as key settlement channels. This article analyzes why stablecoins are the most suitable native settlement layer for AI payments.

Visa and Mastercard Take Action on the Same Day: Why Have Stablecoins Become the Winners in AI Payments?

Recommended for you

More topics

More topics