「Stablecoin & Payments Weekly Pulse」 Vol.10:OSL USDGO 100% Yield, Circle Arc L1 & Western Union USDPT

Welcome to Issue 10: Essential Updates in Stablecoin and Payments

1. This Week's Stablecoin Payment Data

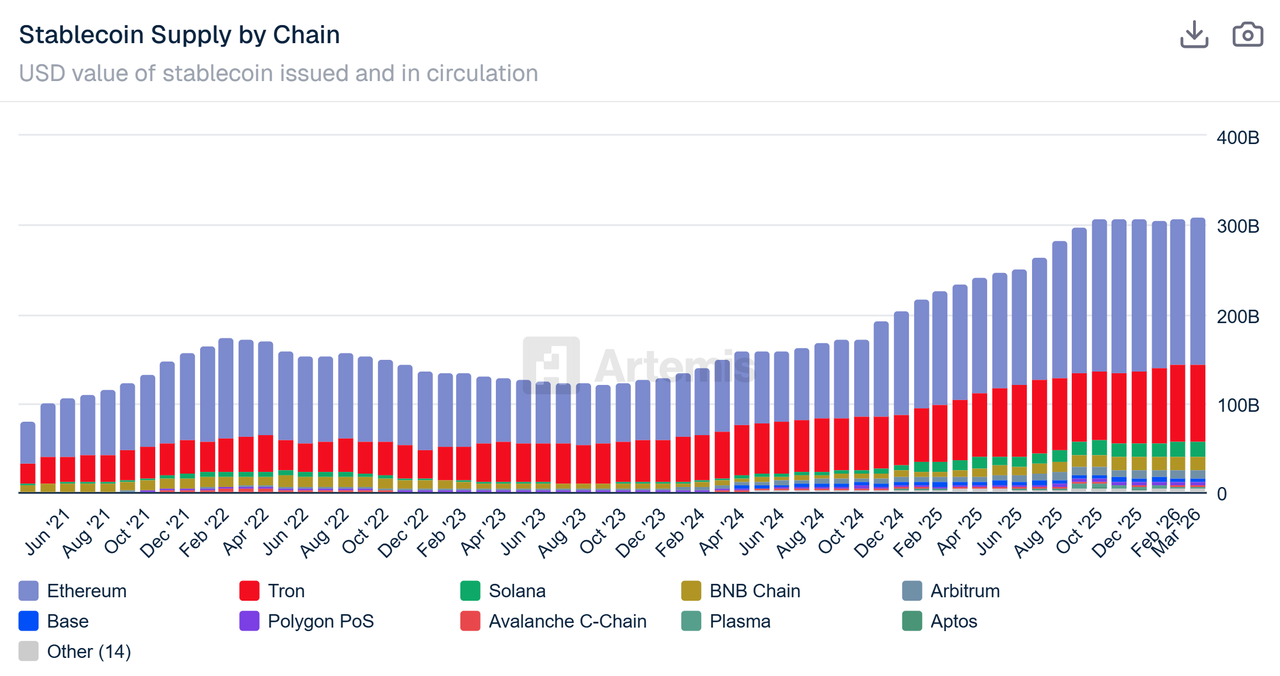

As of March 5, 2026 (7-day rolling basis), the total stablecoin market capitalization and supply stands at approximately $309.2 billion, maintaining its position in the $300 billion range. This steady level reflects ongoing demand stability in a fluctuating market environment.

Messari data shows continued transfer activity, with cumulative volumes over the past 30 days exceeding $8.81 trillion. Daily averages range from $291 billion to $300 billion; extrapolating, the past 7 days likely saw totals between $1.8 trillion and $2 trillion. These figures demonstrate stablecoins' enduring role in high-volume on-chain transactions.

Adjusting for long-term noise, OSL Research estimates the "effective" volume—excluding market-making, wash-trades, and bot transactions—at roughly one-fifth of the total, placing the past 7 days around $360 billion to $400 billion. This adjusted metric highlights genuine economic transfers, offering a clearer picture of real-world utility beyond automated noise.

(Data sources: Messari, Artemis, OSL Research)

("Effective" = adjusted data, excluding non-economic noise.)

What do these steady volumes suggest about market resilience in your view? Share in the comments!

2. OSL Research Growth Observations

This week's top three stablecoin/protocol growth by market capitalization:

1.Global Dollar (+9.84%; weekly transfers $2.02B, +7.67%):

Issued by Paxos Digital Singapore and regulated by the Monetary Authority of Singapore (MAS) , Global Dollar is backed 1:1 by USD reserves. Users can mint or redeem 24/7 via Paxos dashboards or APIs. The 9.84% growth stems from its revenue-sharing model: Approximately 97% of reserve asset yields are distributed to Global Dollar Network partners like Kraken , Robinhood , and Anchorage Digitalbased on contributions such as app promotion and liquidity provision. This incentivizes institutions to boost minting and liquidity. Funds show high turnover characteristics, circulating rapidly in Global Dollar Network enterprise payments, Solana decentralized exchange liquidity pools, and lending protocols—widely used for cross-border settlements and trading hedges.

2. Tether Gold (+7.40%; weekly transfers $3.99B, +204.60%):

The scale expansion this week is largely driven by geopolitical safe-haven sentiment and gold price rises. Risks around the Strait of Hormuz blockade pushed gold above $5,400 per ounce, combined with large institutional transfers (for example, Antalpha 's $15.39 million to Bybit Fintech Limited ), leading to a sharp surge in weekly transfers. Funds exhibit safe-haven-driven, fast-turnover patterns, with large deposits reflecting active arbitrage rather than long-term holding. As CME Groupfutures markets close on weekends, tokenized gold becomes the sole public channel for gold price discovery during off-hours. The on-chain market handles nearly 100% of weekend price discovery, and futures reopening often aligns with on-chain trends.

3. MetaMask USD (+4.46%; weekly transfers $60.16M, -85.59%):

Issued by Bridge (under Stripe ) via the M0 protocol, MetaMask USD is backed 1:1 by short-term U.S. Treasuries under regulatory custody, integrated natively into MetaMask wallets on Ethereum and Linea. The 4.46% growth is fueled by wallet-native features and payment incentives. Users mint via in-wallet fiat on-ramps or stablecoin swaps, enjoying up to 3% minting rewards. The ecosystem loop includes seamless swaps, trading, lending, and yield optimization, plus 萬事達卡 -linked MetaMask Card cashback (1% standard, 3% on first $10,000 for premium). Combined with swap rewards and holding incentives, this drives user engagement.

3. This Week's Stablecoin Payments and Infrastructure News

1.OSL StableHub Launches USDGO Limited-Time 100% Annualized Yield Incentive

OSL Group's StableHub introduced a time-limited reward program for USDGO: New users holding USDGO on OSL Global can earn up to 100% annualized rewards (capped at 1,000 USDGO per user, 7-day validity); existing users get 18% on limited amounts plus 3% long-term on excess. Active from March 10 to April 10, 2026.

Insight:

This activity signals OSL's stablecoin operations entering a scale-up phase: The reward structure focuses costs on new user acquisition and liquidity building, with caps and tiered rates keeping long-term pool margins manageable. It aligns with evolving stablecoins from "issuance and launch" to "tradable, circulatable, settleable." StableHub's role clarifies: Integrating USDGO holding, trading depth, and settlement utility into one loop—laying a solid foundation for expanded payment and on/off-ramp applications.

2. Circle Launches Arc Layer 1 Chain Tailored for USDC

Circle unveiled Arc, a Layer 1 blockchain designed for institutional finance and agent economies, with ~700-800ms confirmations and USDC as gas units—aiming for "1 cent, 1 second, 1 click." It also introduced Nanopayments for micro-transfers and x402 protocol to advance artificial intelligence payments.

Insight:

Circle's move targets agent economy payment infrastructure, solidifying USDC's ecosystem lead. Nanopayments and x402 anticipate artificial intelligence-driven micro-payments; "1 cent, 1 second, 1 click" challenges SWIFT's cross-border dominance—potentially eroding traditional shares as agents scale.

3. Western Union Launches USDPT Stablecoin for Global Transfers

Western Union partnered with Crossmint to launch USDPT on Solana as part of its "digital asset network." Issued by Anchorage Digital Bank, users convert to local currencies at 360,000+ Western Union points worldwide; Solana enables instant payments, digital USD storage, and global cash access.

Insight:

USDPT's cash-out integration with Solana's speed builds a bridge for digital-to-fiat liquidity, locking Western Union's network edge. It guards against regulatory risks on Solana congestion and stable redemptions—expanding from remittances to a broader hybrid ecosystem.

4. World's Largest Stable USDT Dips 0.8% to $183.61B This Month

USDT market cap fell 0.8% to $183.61 billion this month, continuing January's drop from $186.84 billion peak—first consecutive monthly contraction since 2022 Terra collapse. USDC held steady at ~$75 billion, with minimal yearly growth.

Insight:

This liquidity fuel drain points to proactive decompression amid macro repricing. Strong U.S. jobs data lifted Treasury yields, trimming short-term rate cut expectations. Watch Tether's next large mints for signs of cycle recovery and fresh capital repricing.

5. Crypto Now Has Over 200 Trackable On-Chain Stables

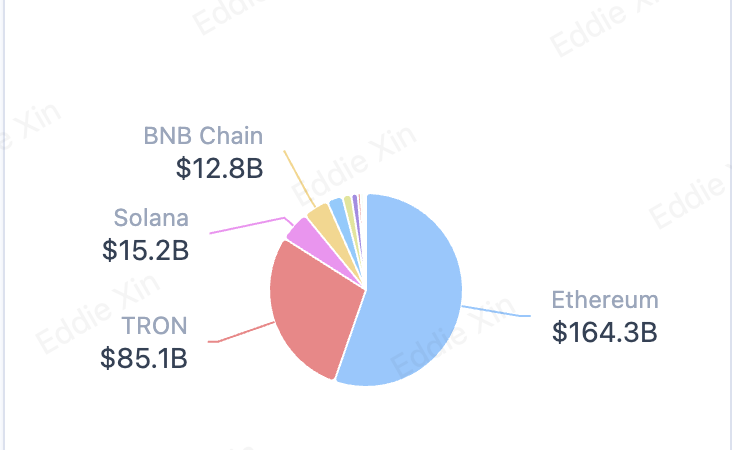

Dune data: Crypto boasts more than 200 traceable stables across 37 chains (35 EVM + Solana/Tron); cap >$320B, non-USD $2.4B. Centralized exchanges hold $80B; January transfers >$10T (56% decentralized exchange)—highest since April 2022.

Insight:

This reveals institutions accelerating from off-chain custody to on-chain programmable liquidity: Centralized exchange holdings show broker/market-maker reliance on crypto-native flows; decentralized exchange dominance signals DeFi's leap to primary settle/leverage venue—shifting risk factors from "exchange depth" to "on-chain depth" for primaries and hedges.

6. Standard Chartered Hires Ex-JPM Blockchain Head for Payments

渣打银行 appointed ex- J.P. 摩根 Kinexys co-head Naveen Mallela as global payments lead, starting May 4—to modernize cash management.

Timed with record stable transfers and regulatory sandboxes, this signals globally systemically important banks betting on "programmable money infrastructure." Mallela's hire fills blockchain gaps, positioning Standard in talent/tech arms race with HSBC/Citi. Expect RWA tokenization, real-time cross-border, stable bridges—locking pound's edge pre-2027.

7. In Economic Decision Scenarios, 22 of 36 AI Models Pick Bitcoin as Top Money Tool

Bitcoin Policy Institute study: In simulated decisions, 22 of 36 artificial intelligence models ( OpenAI / Anthropic / 谷歌 / DeepSeek AI / xAI / MiniMax , etc.) chose Bitcoin as preferred money; none picked fiat first. Bitcoin for long-term storage; stables for payments/settles in 28 scenarios.

Insight:

Artificial intelligence favors stables for instant/low-friction in pursuits of scalability—splitting from Bitcoin. Maps to dual-layer machine economies: Bitcoin as store/settler, stables for daily micros/settles. Squeezes traditional central bank digital currencies.

8. Tether + Lugano Invest CHF 5M in Plan B Phase 2

Tether.io and Città di Lugano launch Plan ₿ Phase 2 (2026-2030), investing up to CHF 5 million in digital infra for sovereignty/tech autonomy. Focus: Digital asset/automation management, trade/commodity hubs, privacy IDs, local artificial intelligence/agents, distributed urban infra. Since 2022, >400 merchants accept BTC/USD₮/LVGA; digital bonds/municipal crypto payments piloted.

Insight:

Tether's renewal is defensive/offensive: Low-cost locks Switzerland as European bridgehead vs. U.S./EU regulations; artificial intelligence/distributed infra fusion seizes "artificial intelligence-driven city economies." Counters single-issuance reliance.

9. Latam Stable App ARQ Raises $70M, Expands from Remits to Wealth Management

ARQ secured $70 million from Sequoia Capital / Founders Fund ; funds for rebranding, hiring, expanding from USD transfers to wealth management, local high-yield accounts, credit. Formerly DolarApp, offers multi-currency accounts/wallets/FX/debit cards for cross-border storage/transfers. >2M users, $10B+ annual volume.

Insight:

Sequoia's emerging market consumer finance infrastructure bets + Founders' crypto-native view signal "Latam stable super apps" as next emerging market alpha. In high-inflation/fragmented/capital-controlled Latam, ARQ expands from remittances to management/accounts/credit—eroding traditional banks' retail/small and medium enterprise shares.

4. Analyst Observation: Rate Cut Cycle—What Drives Circle's Continued Growth?

Analyst: Eddie Xin, Chief Analyst, OSL Research

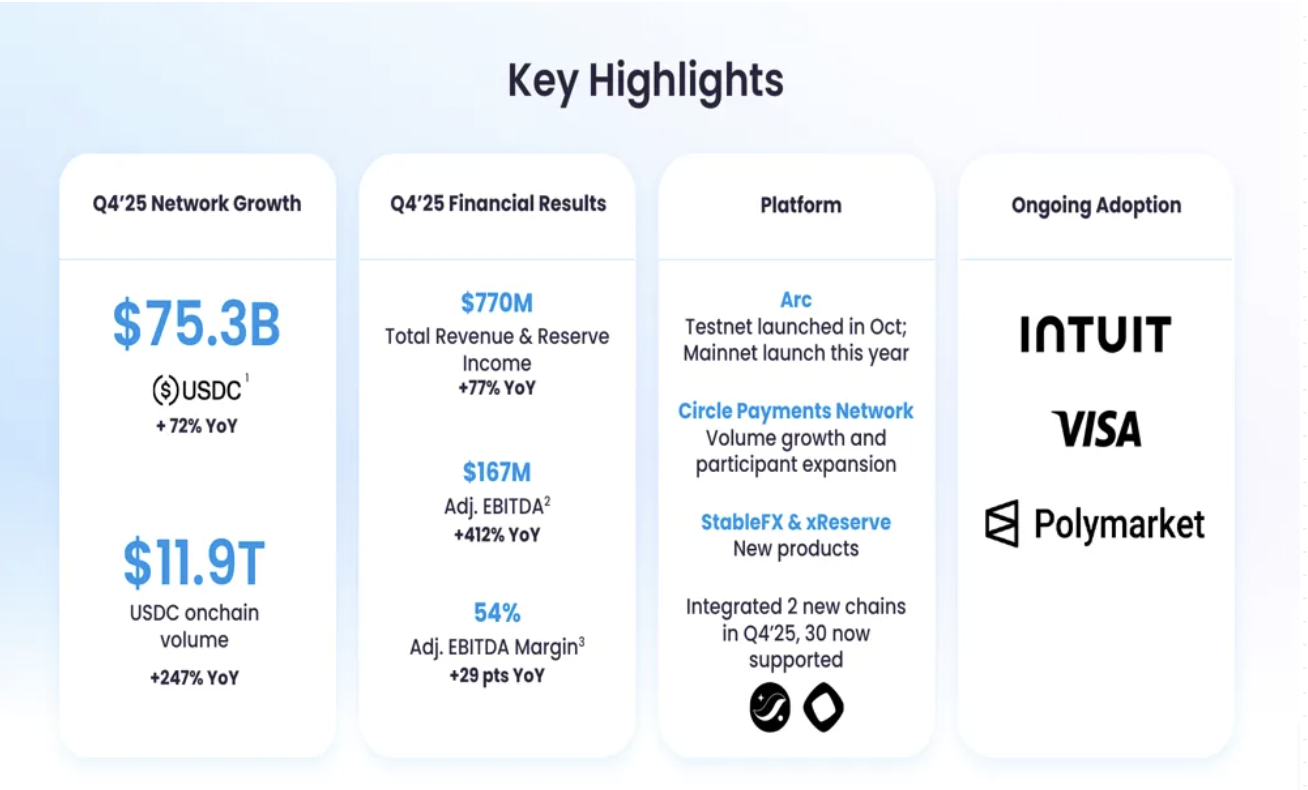

Circle (NYSE: CRCL) released its Q4 and full-year 2025 earnings.

Q4 revenue was approximately $770 million, surpassing the consensus expectation of $740 million. Adjusted earnings before interest, taxes, depreciation, and amortization surged year-over-year. The stock price rose nearly 20% following the report, based on market close. When breaking down the numbers, Circle's revenue remains heavily reliant on interest income from client funds invested in high-liquidity assets like Treasuries. In Q4, total revenue of $770 million included about $733 million from interest, accounting for over 95%. This model is clear and replicable, but it is also weighty and highly sensitive to interest rate cycles.

The current macroeconomic environment is entering a rate cut phase. As interest rate hubs decline, the "spread eating" business naturally thins out. If Circle were merely a proxy for Treasury yields, its valuation could not sustain expansion on shrinking margins. The elasticity in the stock price suggests the market is repricing a different narrative: a shift from an interest-based operation to a payments infrastructure provider.

The conference call's Q&A session reflected this pivot. Analysts did not dwell long on interest income details. Instead, they focused on stablecoins' potential in artificial intelligence scenarios: Could they be embedded in artificial intelligence workflows? Could they serve as a medium for agent-to-agent value transfers? Could they evolve from "cryptocurrency settlement tools" to "native money for machine economies"? These questions reveal the market's effort to confirm sources of "growth revenue."

The elements that ignited institutional enthusiasm in the report were Circle's updates on the Arc network and the Circle Payments Network. Arc functions like a self-built "clearing highway," designed to extract stablecoin settlements from the congestion and uncertainties of public chains. The company disclosed that since the testnet opened on October 28, 2025, more than 100 banks and payment institutions have joined. It handles 230,000 daily transactions with 0.5-second settlements and near-24/7 availability. The mainnet is planned for launch in 2026.

The Circle Payments Network acts more like the "on-ramps, tolls, and logistics centers" along this highway. It is not a blockchain but an API-driven payment orchestration system. It connects bank account systems with on-chain assets, covering on-ramps, off-ramps, routing, compliance verification, and reconciliation clearing. It aims to solve a long-standing pain point—fiat held in banks and value on the chain—by enabling seamless conversion, transmission, and delivery within the same process.

From the market's perspective, interest income is "given by macro conditions." Network fees and payment service fees are "generated internally." The former is squeezed by rate cuts; the latter depends on network effects and scaled settlement scenarios. Institutions are more willing to assign premium valuations to the latter.

A consensus is forming among leading stablecoin issuers to build their own Layer 1 networks—Circle with Arc, Tether with Stable and Plasma, and Stripe with systems like Tempo. The paths differ, but the goal is the same: to control settlements. Fees and settlement costs can be designed as part of the business model, even payable directly with their own stablecoin. Compliance elements like rules, blacklists and whitelists, risk strategies, and audit interfaces can be engineered in. Settlements from issuance to circulation and redemption form a closed loop, reducing dependence on external chains' congestion and governance issues.

For Ethereum, the implications are significant: Assets and scenarios will migrate toward efficiency and compliance. In the past, chain value was anchored in asset scale and settlement activity, with stablecoins serving as a cornerstone and the most stable source of demand. As large-scale transfers and commercial settlements shift to issuer-built networks, public chains face not just a narrative challenge but a loss of cash-flow-type demand. Gas revenues will thin out, and the focus of on-chain capital markets will rebalance. Artificial intelligence agent payments and reconciliations, if scaled under compliance, are more likely to prefer controllable, auditable, and editable dedicated networks over universal ones.

Circle's stock rise is not simply a response to "higher interest earnings." The market is betting on its transition from "stablecoin issuer" to "settlement network operator": Connecting banking systems on one end with on-chain assets on the other. The "1 cent, 1 second, 1 click" vision is building momentum. In financial history, those who own the rails often hold more pricing power than those who merely ride them.

Disclaimer and Disclosure

1. Nature of Document

This document (“Document”) has been prepared solely by internal personnel of OSL for informational purposes. It does not constitute investment, legal, tax, or other professional advice and should not be relied upon as such. No part of this Document may be reproduced, distributed, or transmitted to any third party in any form without the prior written consent of OSL.

This Document does not constitute an offer, solicitation, marketing material, product disclosure, or legal document, nor does it form the basis of any binding contract or commitment. It is intended solely to provide OSL’s observations and strategic insights on the industry and does not represent OSL’s official opinions, strategies, or decisions.

The authors are not independent research analysts, and this Document does not constitute “investment research” as defined under applicable laws and regulations. Accordingly, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any pre-dissemination trading restrictions.

2. Non-Reliance

The information, opinions, and analyses contained herein are based on publicly available information and OSL’s internal judgment. They do not take into account the individual objectives, financial circumstances, or needs of any recipient. This Document is not a personal recommendation or solicitation to buy, sell, or otherwise transact in any financial instrument, product, or service.

Before making any investment or other decision, recipients must consult their own independent advisors, considering their individual circumstances, objectives, experience, and resources. All investments involve risk; values may fluctuate, and investors may receive less than the original invested amount. Past performance is not indicative of future results.

3. Accuracy, Completeness, and Limitation of Information

This Document is based on information that OSL considers reliable; however, OSL has not independently verified its accuracy, completeness, or fairness. Reasonable care has been taken to ensure that the content is not false or misleading, but OSL makes no representation or warranty, express or implied, regarding its accuracy, completeness, fairness, or reasonableness.

OSL is not responsible for any errors, omissions, or consequences arising from reliance on third-party information referenced herein. Performance of any discussed instruments, entities, or strategies may be materially affected by market, regulatory, technical, or other factors.

4. Forward-Looking Statements

This Document may contain forward-looking statements that involve known and unknown risks, uncertainties, and other factors. Actual results, performance, or achievements may differ materially from those expressed or implied. OSL does not undertake any obligation to update, revise, or withdraw any forward-looking statements.

5. Conflicts of Interest

OSL, its affiliates, and employees may hold positions in, or engage in transactions involving, the assets or entities discussed herein. The authors or other personnel involved in the preparation of this Document may receive compensation that is linked to the performance of OSL’s business. OSL has implemented policies and procedures to identify and manage potential conflicts of interest.

6. Intellectual Property and Restrictions on Use

This Document is protected by copyright and is intended solely for the designated recipient. Recipients may store, display, analyze, modify, reformat, and print this Document for their own internal use only. Recipients may not, without OSL’s prior written consent:

Resell, redistribute, or commercially exploit this Document;

Reverse engineer, extract, or create derivative works, including for training or use in machine learning/artificial intelligence systems;

Publish or transmit this Document to third parties.

7. Limitation of Liability

To the maximum extent permitted by applicable law, OSL, its affiliates, officers, employees, and agents shall not be liable for any direct, indirect, incidental, consequential, or special damages arising from or in connection with the use of, reliance upon, or interpretation of this Document, including but not limited to:

Loss of profits;

Business interruption;

Data loss;

Reputational harm.

8. Global Distribution Notes

Recipients are responsible for compliance with local laws. Distribution of this Document may be restricted in certain jurisdictions. Recipients must ensure that it is not distributed to any person or entity to whom such distribution would be unlawful.

More topics

More topics

Latest

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

Explore if stablecoins can lower global remittance costs (currently 6%) and their role in solving financial exclusion in orphaned corridors.

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

Discover how stablecoins restructure B2B payments, reduce costs by 70%, and solve the $27T trapped liquidity issue in the SWIFT network.

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

Explore the three stages of stablecoin evolution: from exchange trading chips and DeFi liquidity to becoming global compliant payment infrastructure.

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Discover how stablecoins address trapped cash, FX risk, and visibility gaps in corporate treasury through quiet pilots and institutional adoption.

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Discover the significance of Bitcoin's 200-week SMA, historical returns, and how to use technical indicators for long-term crypto investing.

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Analyze Bitcoin market structure using on-chain data. Learn why the recent sell-off's realized loss is half of the previous round.

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Recommended for you

More topics

More topics