Crypto Investing in the Philippines: What Investors Should Know

The Philippines has become one of Asia’s most active retail crypto markets, powered by a young population, high mobile-internet usage, and a strong remittance economy. Crypto is now part of everyday financial life for many Filipinos, from trading and savings to gaming and cross-border payments. Against that backdrop, knowing how to buy crypto safely—and on the right platforms—matters more than ever.

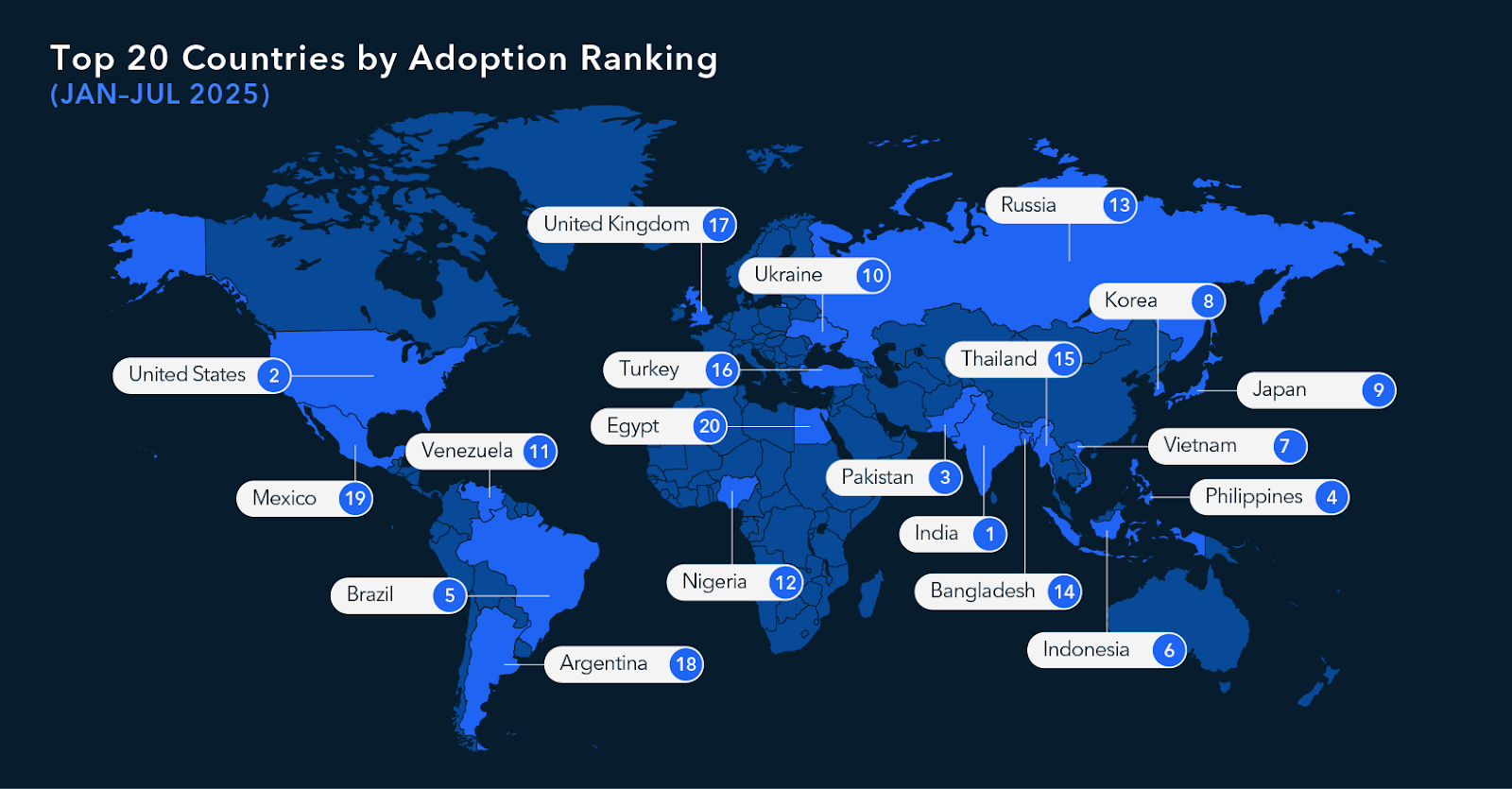

Crypto adoption in the Philippines

According to the 2025 Crypto Adoption and Stablecoin Usage Report by TRM Labs, the Philippines is ranked fourth for crypto adoption globally behind India, the United States and Pakistan.

Source: TRM Labs

Over the past few years, the Philippines has consistently appeared near the top of global crypto adoption rankings, reflecting strong grassroots participation rather than just institutional flows. Play-to-earn gaming and side-income trading introduced millions of users to digital wallets and tokens, and many of those early adopters have stayed in the market as spot traders or long-term holders. Overseas Filipino workers and their families have also experimented with crypto as an additional rail for sending and receiving value.

Today, Filipino crypto users range from students and gig workers to small business owners and professionals managing diversified portfolios. Local fintechs and exchanges offer familiar, app-based experiences, while international platforms give access to a broader range of coins and products. Institutions, meanwhile, are gradually exploring tokenisation, stablecoins, and digital asset infrastructure, although retail activity still drives the bulk of volumes.

Why Filipino investors are interested in crypto

For many Filipinos, crypto is first and foremost a way to access global capital markets with relatively low barriers to entry. Major assets such as bitcoin and ether provide 24/7 trading opportunities and an alternative to purely peso-based savings. Others use crypto primarily as a payment or transfer rail: for instance, receiving funds from relatives abroad in tokens or stablecoins, then converting to pesos through local on-ramps.

Regulatory environment: BSP, SEC, and key rules

Two authorities are central to the Philippine crypto landscape. The Bangko Sentral ng Pilipinas (BSP), which is the Central Bank of the Philippines, regulates Virtual Asset Service Providers (VASPs), which include exchanges and wallet providers that handle fiat–crypto conversion and custody. BSP sets requirements on licensing, minimum capital, cybersecurity, and AML/CFT controls, and it supervises how these businesses connect to the formal banking and payments system.

The Securities and Exchange Commission (SEC) focuses on digital assets that qualify as securities and on platforms that publicly offer or trade such assets. It has issued repeated warnings about unregistered offshore platforms targeting Philippine residents and has tightened its stance on firms that market to Filipinos without proper authorisation. At the same time, the SEC has clarified that crypto trading remains allowed in the Philippines, provided investors use entities that comply with applicable laws and regulations.

For everyday users, the implications are straightforward. Crypto is not legal tender, but buying and holding digital assets is permitted through duly registered or licensed providers. BSP-regulated VASPs must know their customers, monitor transactions, and follow strict AML/CFT standards. The SEC, meanwhile, can act against platforms or token offerings that bypass registration, which is why investors should treat any “licensed” or “approved” claims with healthy scepticism and verify them against official sources.

How people typically buy crypto in the Philippines

Most Filipino investors start their journey on BSP-licensed local exchanges and apps that support peso deposits and withdrawals. These platforms allow users to open an account, complete KYC, and buy major cryptocurrencies directly against PHP. Integration with local banks and e-wallets makes the experience feel similar to topping up a digital wallet or paying bills online, which has helped drive mass adoption.

More experienced users often add international exchanges to their toolkit to access a wider asset range, derivatives, or more advanced trading tools. In practice, that means funding accounts via card payments, international bank transfers, or by sending crypto from a local VASP to an offshore exchange wallet. When they take this route, Filipino investors accept that consumer protection and dispute resolution will be governed by the foreign platform’s regulator rather than Philippine law.

Peer-to-peer (P2P) markets also play a significant role. On P2P platforms, users buy and sell crypto directly with other individuals, settling in pesos via bank transfers, InstaPay/PesoNet, or e-wallets while relying on on-platform escrow to hold the crypto until payment is confirmed. This route offers flexibility on price and payment methods but requires more caution: investors must judge counterparties, watch for red flags, and be ready to abandon a trade if something feels off.

Larger investors—such as high-net-worth individuals, family offices, or corporates—may turn to over-the-counter (OTC) desks to execute big trades without moving the market. OTC transactions typically involve negotiated pricing and agreed settlement windows, plus more detailed onboarding and documentation. For these users, dealing with an established, regulated OTC provider is often preferable to relying on fragmented P2P channels or retail-only apps when transacting in size.

How Filipinos usually fund their crypto purchases

Peso bank transfers via InstaPay and PesoNet are the backbone of local crypto funding. Users send PHP from their bank accounts to a VASP’s designated account, then buy their preferred assets once the funds are credited. Because these transfers run through the regulated banking system, they are traceable and subject to banks’ own AML and risk-management frameworks. In some cases, banks may ask questions about large or frequent transfers to crypto platforms or apply additional checks.

E-wallets have become another important item on-ramp. Where integrations exist, users can move funds from their wallet to a licensed exchange with a few taps, then convert into crypto. This creates a loop that feels natural for many Filipinos: income arrives in a bank or wallet, moves into crypto as needed, and can be withdrawn back to PHP when it’s time to spend. However, e-wallet policies on crypto can change; users need to stay informed about any updated restrictions or conditions.

Some platforms accept debit and credit cards for instant crypto purchases, which can be convenient for occasional or small transactions. The trade-off is cost: card-based purchases often carry higher fees and, if processed cross-border, additional FX spreads and card-scheme charges. Active traders generally prefer bank transfers or structured OTC channels for recurring or larger flows to reduce cumulative friction.

Key risks when buying crypto in the Philippines

Key risks when buying crypto in the Philippines go beyond price swings and include who you trade with, which platforms you use, and how regulators treat those platforms. Filipino investors should understand these risk areas before committing significant capital so they can choose safer channels and put basic protections in place.

Platform and counterparty risk

Unlicensed or weakly supervised exchanges can suffer hacks, fund mismanagement, or sudden shutdowns.

In P2P trades, buyers face fake payment proofs, chargebacks, or sellers who disappear after receiving funds.

Sticking to reputable platforms, using on-platform escrow, and avoiding off-platform settlement helps reduce these risks.

Regulatory and enforcement risk

BSP can sanction or revoke licences of VASPs that fail to meet standards, affecting user access and withdrawals.

The SEC has acted against offshore platforms that target Filipinos without proper registration.

Relying heavily on unregulated venues increases the chance of being caught in enforcement actions or banking disruptions.

Market volatility and liquidity risk

Crypto prices can move sharply even for large-cap coins, magnifying gains and losses.

Illiquid altcoins often have wide spreads and shallow order books, making execution difficult.

Newer investors are especially exposed when they chase hype tokens or use leverage without fully understanding liquidation risk.

Scams and mis-selling risk

Common scams include fake “investment programs,” phishing sites that mimic exchanges, and social-media offers of guaranteed returns.

Some schemes sell unregistered “tokens” that claim to represent project shares but lack proper documentation.

Verifying URLs and app publishers, checking licences against official lists, and treating unsolicited offers with scepticism are essential safeguards.

How to choose a safe and regulated platform to buy crypto

When selecting a platform, licensing and transparency should come first. Filipino investors should confirm whether a provider is licensed as a VASP by BSP when it handles peso on- and off-ramps, or clearly regulated in another reputable jurisdiction if it operates offshore. Platforms that openly publish details about their licences, corporate structure, and compliance frameworks are usually preferable to those that offer little more than a brand name and marketing slogans.

Security and custody are equally important. Strong platforms segregate client assets from company funds, use institutional-grade cold storage and multi-signature controls, and subject their systems to independent audits. Some also work with regulated custodians and maintain insurance coverage for assets held in custody. These features do not eliminate risk, but they materially reduce operational and counterparty threats, especially for larger or longer-term holdings.

Once regulatory and security basics are covered, investors can look at market quality and support. Deep liquidity, tight spreads, and stable uptime help ensure efficient entry and exit for both small and large trades. Responsive customer service and clear incident-response playbooks are crucial when dealing with account issues, suspicious activity, or platform outages. Educational resources that explain wallet security, AML/KYC expectations, and basic tax considerations can also help investors make better decisions over time.

Buying and trading crypto with OSL

OSL is a regulated, publicly listed digital asset platform headquartered in Hong Kong, designed from the ground up for institutional-grade trading, custody, and infrastructure. It operates under strict regulatory oversight and applies robust AML/KYC, surveillance, and risk-management controls across its services. For Filipino investors who prioritise compliance and operational discipline, this structure offers a clear alternative to lightly supervised exchanges or informal P2P venues.

On the exchange side, OSL provides access to a curated range of liquid digital assets, including major cryptocurrencies and stablecoins. Clients trade on an institutional-grade venue that offers deep liquidity, professional order types, and 24/7 market access, supported by robust technology and risk controls. Rather than functioning as a loose marketplace, the platform follows formal onboarding, monitoring, and reporting processes similar to those used in traditional capital markets.

OSL also operates an OTC and RFQ desk for institutions, professional investors, and high-net-worth clients who need to execute larger trades discreetly and efficiently. These services provide tailored pricing, defined settlement windows, and dedicated coverage, aligning with the governance, documentation, and reporting requirements of more sophisticated users. For larger Filipino investors or regional institutions, such OTC infrastructure can be more appropriate than executing size through fragmented retail apps.

Custody is another core pillar of OSL’s offering. Its solutions feature segregated client wallets, rigorous security controls, and significant insurance coverage for digital assets held under custody. This framework is designed to manage operational risk in a way that individual users and smaller platforms often cannot match. For Filipino investors considering how to store larger crypto balances safely, combining trading and regulated custody within a single, institution-grade ecosystem can be a compelling option.

FAQs: Crypto investing in the Philippines

Is it legal to buy crypto in the Philippines?

Yes. Buying and holding crypto is allowed, provided you use licensed or otherwise compliant providers that follow BSP and SEC rules.

What is the safest way to fund my crypto purchases?

For most users, bank transfers and reputable e-wallet integrations into licensed platforms are safer than cash deals or informal arrangements.

Do I pay tax on crypto gains in the Philippines?

Tax treatment depends on your personal circumstances and the nature of your activity. You should obtain advice from a qualified tax professional rather than relying on general information.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoins aren’t just an issuance game — the real battle is over infrastructure, channel capital, and users.

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin activity cooled while firms kept investing. Vol. 19 examines regulation and enterprise demand across emerging-market payment corridors.

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

Stablecoin supply expands, payment infrastructure investment accelerates, and USDGO crosses US$1 billion in Stablecoin Weekly Pulse Vol. 18.

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

BlackRock's iShares Bitcoin Trust accounted for roughly 90% of a $225 million spot Bitcoin ETF outflow on July 23, raising questions about whether headline flow figures reflect sector sentiment or one fund's...

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

The CLARITY Act's removal from the Senate schedule with 72 hours before recess eliminates near-term procedural certainty, shifting analytical weight toward jurisdictions where licensing frameworks are already...

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

Recommended for you

More topics

More topics