2025 回顧 & 2026 展望— Web3 的下半場

Key Takeaways

2025 marked a true watershed for the Web3 industry — the decisive moment when the sector shifted from its noisy “first half” into the far more demanding and results-oriented “second half.”

Web3 Enters Its Second Half: 2025 as the Crypto Industry’s True Turning PointWe view 2025 as the decisive watershed for the crypto and Web3 ecosystem — the year the “first half” growth model finally ran out of road.The market has shifted away from its old engines: relentless asset-price appreciation and protocol-level innovation. Instead, it is converging toward a new reality where liquidity reigns supreme.In this transition, excessive token creation, chaotic distribution mechanics, and a cascade of risk events steadily drained available liquidity. The “dark forest” era of pure zero-sum games is drawing to a close.

Leaving the first half behind, the industry now steps into its second half — one powered by compliance-driven incremental growth.We define Web3’s “second half” this way: Within clearly defined regulatory boundaries, stablecoins and tokenized real-world assets serve as the primary carriers. On-chain technical capabilities become deeply embedded in genuine payment, clearing, and capital-market workflows — and, ultimately, gain acceptance from mainstream capital inflows and distribution channels.

The Real Drivers of Future Growth from Three Quantifiable Variables: First, whether on-chain settlement networks can continue to deliver lower unit costs and faster settlement times than traditional paths. Second, whether the issuance and redemption mechanisms for stablecoins and other digital assets can be fully audited, regulated, and accepted by financial channels. Third, whether on-chain assets can form a complete closed loop — with solid rights confirmation, transparent information disclosure, and effective secondary-market liquidity comparable to traditional systems.

2025’s Core Shift: The Competitive Battleground Moves from “On-Chain Activity & Trading Volume” to “Compliant, Scalable Financial Behavior”

Stablecoins are no longer confined to serving as internal pricing tools on exchanges. They have begun flowing into real-world scenarios: cross-border settlements, corporate treasury management, and online merchant payments.

RWA(Real-World Asset) shifts from concept proof to productization and institutionalization. Real-world asset tokenization has moved past proof-of-concept. The market now focuses on issuance, custody, disclosure, and suitability arrangements — rather than merely chasing the novelty of “putting assets on-chain.” This evolution means the dominant theme in 2026 will no longer center on bigger narratives. Success will hinge on the genuine ability to deliver end-to-end compliant solutions.

Scenario Outlook: In our baseline scenario, the advancement of the “second half” in 2026 will proceed step by step: first the monetary layer (stablecoins and core payment/settlement infrastructure), then the asset layer (tokenized securities and similar assets); first the institutional side, then the retail side; first cross-border and B2B scenarios, then local retail scenarios.

Upside catalysts include greater regulatory certainty and deepening cooperation with traditional channels;

Downside risks stem primarily from three sources: adverse macro liquidity conditions, major security incidents, or a sudden tightening of key regulatory stances. Any of these could materially disrupt the pace of advancement.We believe this baseline assessment has already been validated by the industry’s evolution through 2025. The following sections lay out the specific data, events, and trends that underpin this outlook.

2025 in Review

2.1 :Industry Data

Asset Prices & Macro Dashboard:

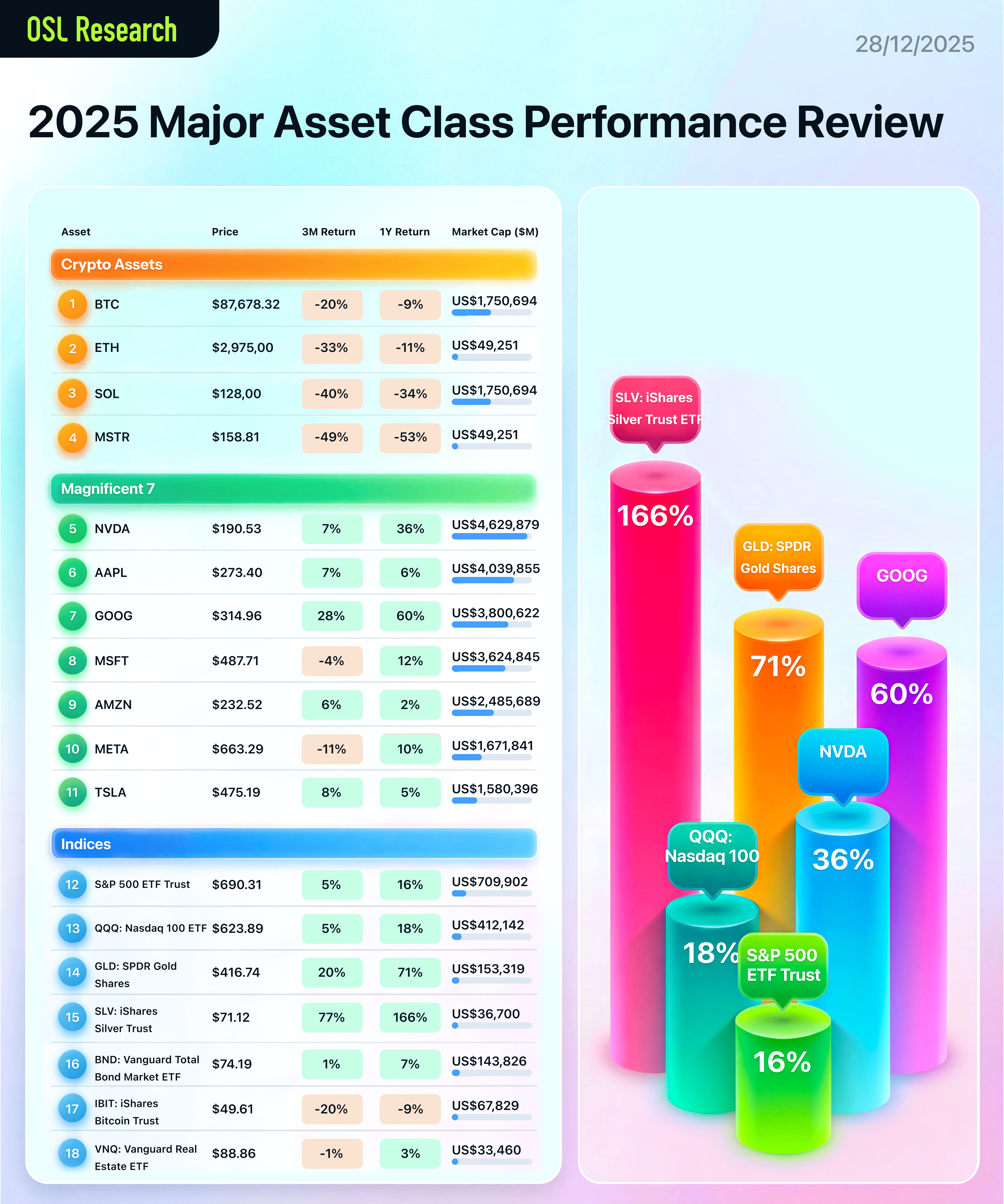

Risk assets showed pronounced divergence in 2025. Under expectations of monetary easing, U.S. equities posted moderate gains: the S&P 500 rose roughly 12% for the year, while the Nasdaq climbed about 18%. Traditional safe-haven assets delivered standout returns.

Gold surged more than 70% over the year, breaking to a new all-time high of approximately $4,525 per ounce in December (see chart below). Silver gained nearly 150%, platinum rose about 145%— marking some of the strongest annual performances in decades for these metals. By contrast, Bitcoin experienced a sharp mid-year rally only to give back most of those gains by year-end. It underperformed major asset classes overall, closing the year down around 10%, hovering near $90,000 in the final weeks. Ethereum and other leading crypto assets followed a broadly similar pattern. The once-familiar “all boats rise together” frenzy in crypto has faded. Instead, the market now moves in closer alignment with the rhythms of more mature financial markets.

On-Chain Metrics & Liquidity:

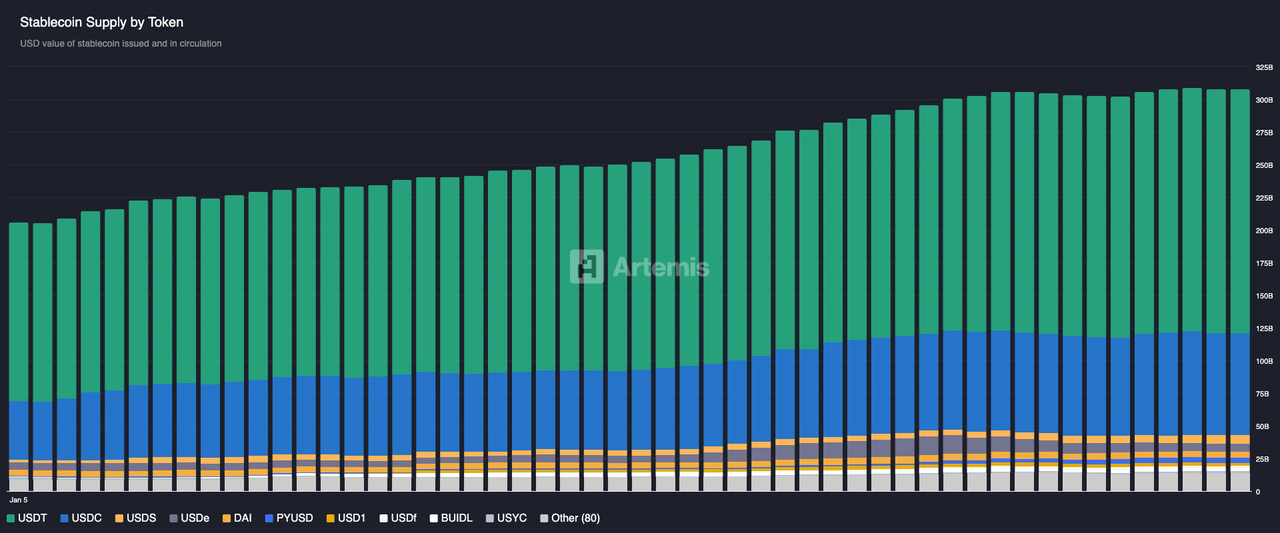

Stablecoin market capitalization surged dramatically this year, climbing from roughly $205 billion at the start to approximately $310 billion by year-end — a gain of more than 50%.This expansion closely tracked improvements in macro liquidity and growing regulatory clarity.

Notably, in July and August following the passage of the U.S. GENIUS Act, stablecoin supply jumped 7% in a rapid burst.By mid-December, the total circulating value of stablecoins worldwide approached $310 billion, marking an all-time high. Dollar-pegged stablecoins continued to dominate: USDT held roughly 60% market share, USDC about 26%. Meanwhile, the number of newly launched compliant stablecoins exploded from 75 to 142 over the course of the year.Against the backdrop of an overall crypto market cap decline of about 10%, stablecoin supply rose 50% in the opposite direction.

In many ways, stablecoins have emerged as a “shadow dollar” supply layer that operates with increasing independence from broader market swings.During periods of macro tailwinds, stablecoin growth accelerates sharply; in headwinds, it slows or even experiences modest contractions — beginning to exhibit cyclical behavior strikingly similar to traditional money supply dynamics.This pattern positions stablecoins as the clear leading indicator of on-chain liquidity. Their supply fluctuations now serve as a real-time reflection of shifting market funding sentiment and risk preferences.

Stablecoin Total Supply, Source: Arteris

Trading Volume & Market Structure:

In 2025, the crypto derivatives market wrote itself into the history books of global finance.Total crypto derivatives trading volume for the year reached an unprecedented $85.7 trillion to $86 trillion, with average daily volume stabilizing around $265 billion.

The crypto market has matured into a legitimate venue where institutional investors systematically harvest returns through hedging and basis trades.Before 2025, crypto derivatives were long dominated by highly leveraged retail flows, leaving the market structurally fragile. The launch of spot Bitcoin and Ethereum ETFs changed that dynamic. Institutions began aggressively deploying cash-and-carry strategies — pairing spot ETF holdings with short perpetual futures — drawing tens of billions in balance-sheet capital into market-neutral, risk-arbitrage plays.

Crypto derivatives are no longer just a trading venue. They have evolved into a new global node for price discovery that increasingly influences the traditional financial system.

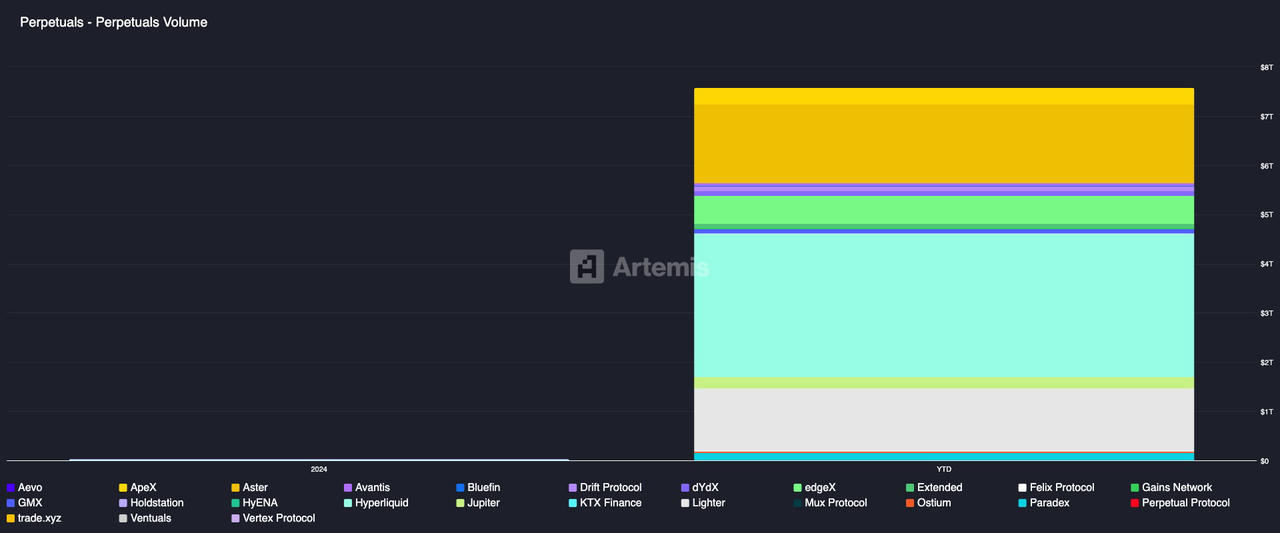

On-chain trading activity underwent a structural transformation in 2025. Decentralized exchanges (DEXs) continued to gain share, with particularly strong breakthroughs in derivatives — especially perpetual contracts.DEX perpetuals cumulative volume for the full year reached approximately $2.6 trillion, lifting their share of the overall derivatives market from under 5% at the start of the year to nearly 12% by year-end.

Monthly data showed DEX perpshitting a record 11.7% share in November.This surge was driven by the emergence of next-generation high-performance DEXs.

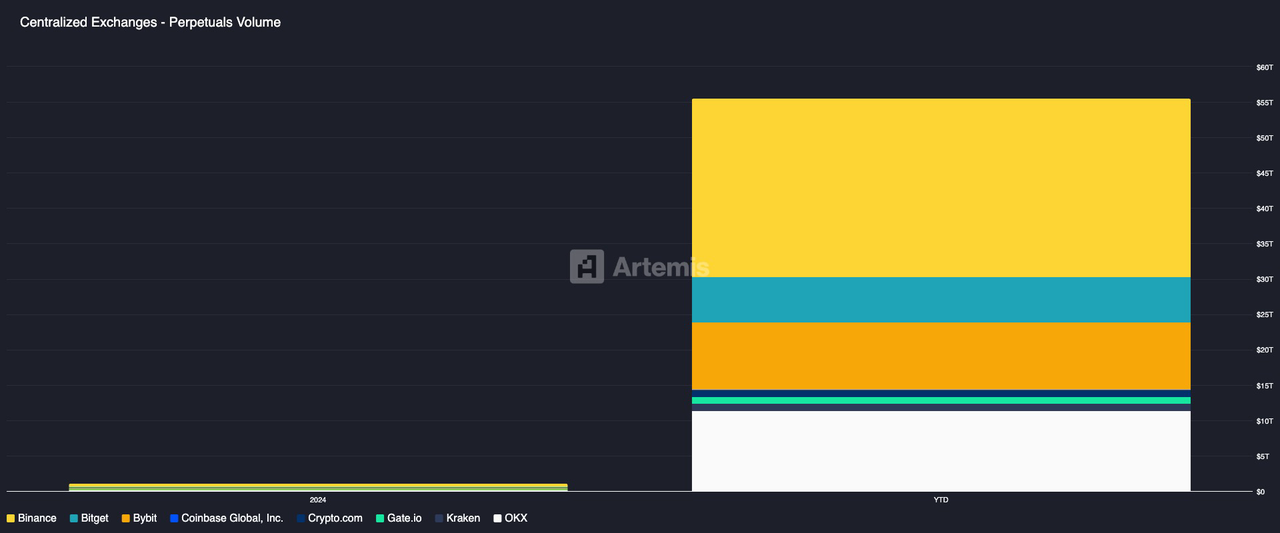

Platforms, such as Hyperliquid, Lighter, and edgeX — leveraging proprietary chains or optimized architectures — delivered near-centralized execution speeds and depth. Hyperliquid alone contributed roughly $2.74 trillion in volume for the year, a figure comparable to Coinbase’s full-year scale.Centralized exchanges (CEXs), meanwhile, faced pressure from regulatory scrutiny and credibility incidents, resulting in some loss of market share. Even so, CEXs retained overwhelming dominance: their derivatives volume totaled around $49 trillion for the year — still several times larger than DEXs.

On the spot side, DEX spot volume share rose from roughly 10% at the end of 2023 to about 20% by the close of 2025. In June 2025, following a major CEX’s move to route liquidity on-chain, DEX spot share briefly spiked to an all-time high of 37%.Decentralized and centralized trading systems are now locked in a dynamic of mutual competition and convergence. Users are voting with their feet, gradually pushing DEXs toward the forefront. Yet in the near term, CEXs retain an irreplaceable edge thanks to deeper capital pools and established user bases.This structural evolution in market composition sets the stage for the later discussion of derivatives and leverage behavior.

Leverage & Liquidations:

As derivatives flourished, market leverage climbed sharply through the middle of the year, only to face violent deleveraging in the fourth quarter. In October, Bitcoin prices briefly approached all-time highs, with heavy long-side leverage building up across the board.Then, on October 10, an unexpected U.S. escalation of tariff threats against China triggered massive market turmoil. That single day produced the largest leveraged liquidation event in crypto history:more than $19 billion in positions were forcibly closed within 24 hours (quickly dubbed the crypto world’s “Black Tuesday”).

The episode laid bare the extreme levels of leverage in the market and the speed at which shocks now propagate. A solitary macro trigger was enough to set off cascading forced liquidations across both decentralized exchanges and centralized platforms. Prices plunged deeply in moments before rebounding sharply — a textbook illustration of how “high-leverage water can whip up towering waves.”As we will explore later in this report, the “10·11 Event” stands as one of 2025’s defining industry watersheds. It forced regulators and market participants alike to confront leverage risks and risk-control mechanisms with fresh urgency.

2.2 Annual Events

1. Political Influence and Tokenized Marketing: Trump Family Meme Coins Trigger Compliance and Conflict-of-Interest Controversies

Source: Bitcoin 2024.

In early 2025, U.S. President Donald Trump and First Lady Melania Trump publicly launched meme coins named after themselves — $TRUMP and $MELANIA. According to reports, $TRUMP launched on January 17 at $10 per token and surged to $75 within less than two days before settling back into the $30–$40 range. $MELANIA followed a similar pattern, spiking 70% shortly after launch only to drop sharply thereafter. The Trump family, through affiliated entities, reportedly held 80% of the supply of both tokens.

At the peak, this ownership briefly inflated their combined net worth valuation by roughly $58 billion, igniting widespread controversy. Critics accused the move of exploiting public office for personal gain, raising serious questions of conflict of interest and even the risk that foreign actors could use tokens to exert influence over U.S. politics. Senator Elizabeth Warren and other lawmakers promptly sent letters to multiple agencies demanding investigations, with Warren describing a sitting president issuing private tokens as “the most severe conflict of interest in modern presidential history.”

While the White House maintained that any proceeds would support campaign-related activities and other legitimate purposes, criticism from regulators, ethicists, and market observers continued unabated. This episode marked a new peak in the politicization of crypto.

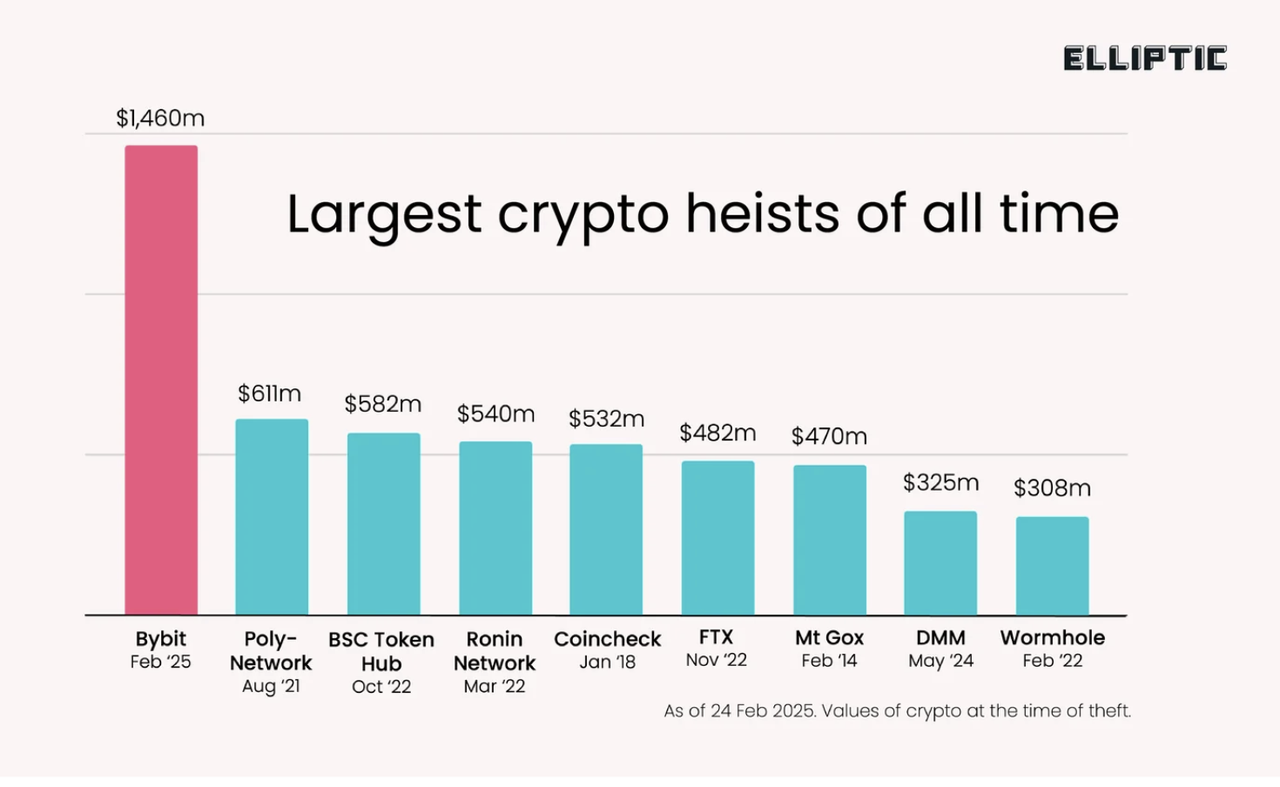

2. Exchange Security Milestone: Bybit Suffers Over $1 Billion Hack

Source: Elliptic Official Website.

On February 21, 2025, crypto exchange Bybit disclosed that it had been targeted by a North Korean-linked hacker group in a sophisticated attack that resulted in the theft of approximately $1.44 billion worth of crypto assets. The attackers used malware to deceive Bybit’s internal systems into authorizing massive unauthorized withdrawals, making this the largest cryptocurrency theft ever recorded — more than double the $611 million stolen in the 2021 Poly Network incident. What raised the most alarm was the speed of laundering: the stolen funds were quickly fragmented and moved through thousands of cross-chain transactions involving decentralized exchanges, unregulated OTC dark pools, and privacy bridges to obscure the trail.

The U.S. Federal Bureau of Investigation (FBI) formally attributed the attack to North Korean state-sponsored actors, consistent with their history of targeting high-value crypto platforms. The Bybit hack became one of 2025’s most consequential events, intensifying global regulatory focus on exchange security standards, cross-border enforcement cooperation, and anti-money-laundering (AML) controls, while serving as a major catalyst for renewed efforts to curb illicit crypto activity and close gaps in unregulated on-chain channels.

3. U.S. Policy Shift: From “National Strategic Reserve” to Pension Allocable Assets — Expanding the Crypto Policy Toolkit

Crypto Policy, Source: White House Official Website

In the second half of 2025, the U.S. government continued its bold push to foster digital asset innovation. On August 7, President Trump signed the executive order titled “Expanding Access to Alternative Assets for 401(k) Investors.” The order created a “safe harbor” for retirement plans — including 401(k)s and other pension vehicles — to invest in crypto and other alternative assets. It directed the Department of Labor and relevant agencies to issue clear guidelines that would reduce legal liability for plan fiduciaries who allocate to properly vetted digital assets, provided full disclosure and robust risk controls are in place.

In plain terms, the policy opened the door for U.S. retirement savings to make measured allocations to compliant crypto products. Industry observers widely viewed this as the long-awaited gateway for trillions of dollars in pension capital to enter the digital asset market.

Earlier, on March 6, the President issued another executive order establishing a “Strategic Bitcoin Reserve” and a “U.S. Digital Asset Treasury.” Under the directive, all Bitcoin seized through law enforcement actions would be deposited into the national strategic reserve and held long-term rather than auctioned off — creating an official state-level BTC stockpile.

Other forfeited digital assets would be consolidated into a dedicated “Digital Asset Treasury” account managed professionally by the Department of the Treasury. The order explicitly prohibited discretionary liquidation of these reserves and encouraged exploration of budget-neutral methods to further accumulate Bitcoin. Together, these measures signaled strong official endorsement of digital gold and tokenized assets at the national level.

These two landmark policies — one unlocking compliant, long-term institutional capital, the other demonstrating sovereign recognition and reserve-building intent — were seen across the industry as clear signs of the U.S. “national team” stepping onto the field. Combined with the earlier GENIUS Act, they sent a powerful unified message: the United States is actively working to integrate on-chain dollar stablecoins and digital assets into the core of its financial system — reinforcing dollar hegemony while positioning itself to lead the next generation of financial infrastructure.

4.Regulatory Winds Recalibrate: Binance Litigation Withdrawal and CZ Pardon Send Strong Signals

Source: photograph by David Ryder / Bloomberg / Getty

In the first half of 2025, the tone of U.S. crypto regulation shifted dramatically. On May 30, the SEC abruptly withdrew its civil lawsuit against Binance and its founder Changpeng Zhao (CZ), citing “prosecutorial discretion” and dismissing the case with prejudice — meaning no further pursuit of the charges.Incoming SEC Chairman Paul Atkins issued a statement underscoring the pivot: “Innovation cannot flourish under enforcement alone.”

The remark captured the new administration’s intent to replace litigation warfare with clear, workable rules for the digital asset sector. Even more symbolic was the October 23 announcement: President Trump confirmed he had signed a full presidential pardon for CZ, absolving him of the guilty plea related to violations of U.S. anti-money-laundering laws. CZ had been sentenced to four months in prison in early 2024, paid a $4.3 billion fine, and completed his sentence by September 2024.

The pardon carried largely symbolic weight, serving as a powerful signal of renewed openness toward the crypto industry’s re-entry into mainstream U.S. finance. Binance responded swiftly, publicly stating it would aggressively pursue U.S. compliance licenses and expand regulated operations in the country. These moves formed part of a broader pattern.

Throughout 2025, the SEC withdrew or paused enforcement actions against Coinbase and several other major players, effectively drawing a line under the era of aggressive, case-by-case litigation. Under the Trump administration, the regulatory baseline moved decisively from “enforcement-first crackdown” to “rule-making + industry support.” The change sent a clear message not only domestically but to regulators worldwide: the United States was choosing structured integration over prolonged confrontation, paving the way for compliant crypto entities to operate at scale within the American financial system.

5.Stablecoins Enter the Capital Markets: Circle’s IPO Ignites Valuation Anchor for “Compliant Stablecoins”

Circle IPO Debut Day, Source: Reuters/

Circle — the leading compliant stablecoin issuer — went public on June 5, 2025, completing its IPO on the New York Stock Exchange under the ticker CRCL and becoming the world’s first listed company centered on stablecoin operations. The shares priced at $31 each.

On the first trading day, the stock surged 123%. Over the next two weeks, fueled by a steady stream of favorable policy developments, it climbed as high as $238. By late June, Circle’s share price had risen approximately 245% from the IPO level, adding nearly $40 billion to the company’s market capitalization compared with its debut-day close.

Two major catalysts drove this remarkable run: First, on June 17 the U.S. Senate passed the GENIUS Act, establishing a clear federal regulatory framework for stablecoins and significantly boosting market confidence in compliant issuers such as Circle.

Second, several major Wall Street investment banks and asset managers initiated coverage with “Buy” ratings, arguing that regulatory tailwinds combined with accelerating enterprise demand position Circle to dominate the global stablecoin market in the years ahead. Notably, the listing also reversed USDC’s mid-year stagnation: circulating supply recovered and approached the $40 billion mark once again, reflecting restored investor confidence in its regulatory outlook. Under the dual tailwinds of Circle’s IPO and stablecoin legislation, the stablecoin sector emerged as one of the few areas in 2025 to achieve substantial scale growth.

Circle’s public debut stands as a landmark in the deepening integration of crypto with traditional capital markets — providing the industry with its first meaningful public-market valuation benchmark while bringing the “digital dollar” concept firmly into the sightline of mainstream institutional investors.

6. Federal Framework Takes Effect: GENIUS Act Brings Stablecoins into Institutionalized Regulation and Disclosure Regime

GENIUS Act, Source: White House Official Website.

GENIUS Act Signed into Law – On July 18, President Trump formally signed the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) into law. This represents the first federal-level stablecoin regulatory legislation in the United States and is widely regarded as a landmark in the history of digital-asset regulation.

The Act establishes a comprehensive licensing and supervisory framework specifically for payment stablecoins: issuers must back 100% of their stablecoins with high-liquidity assets (U.S. dollar cash or short-term Treasuries) and disclose reserve composition publicly on a monthly basis; stablecoin issuance requires federal licensing and is subject to oversight by the Department of the Treasury, the Federal Reserve, and other regulatory authorities; issuance and circulation must comply with anti-money-laundering (AML) and sanctions requirements, with issuers explicitly included under the Bank Secrecy Act; in the event of issuer bankruptcy, stablecoin holders’ claims take priority over other creditors to protect consumers.

The significance of the GENIUS Act extends far beyond investor protection — it embeds stablecoins into the core of national financial infrastructure: by requiring reserves to be invested primarily in U.S. Treasuries, the Act effectively turns every stablecoin into a lawful purchaser of American government debt. This transforms each digital dollar into a “legitimate buyer of U.S. sovereign obligations,” channeling massive investment flows toward the United States while reinforcing the dollar’s status as the world’s reserve currency. The Act also mandates that issuers maintain technical capabilities to freeze, redeem, or even burn tokens when legally required, ensuring full cooperation with law enforcement.

In short, the passage of the GENIUS Act is seen as America’s landmark embrace of digital assets: it not only delivers a clear “U.S. model” for stablecoin regulation but also accelerates the rollout of similar rules in other major economies. As the White House press release stated, the move aims to ensure “every meaningful digital-asset innovation happens in the United States,” signaling Washington’s determination to seize the commanding heights in the global stablecoin competition.

7.Three New Hotspots Advancing in Parallel: On-Chain Derivatives Accelerate, Tokenized Stocks Heat Up, Prediction Markets Break Out

Prediction Market Kalshi Founding Team, Source: Forbes Official Website.

2025 saw several high-profile innovation tracks emerge, driving rapid growth in users and capital inflows. First, on-chain derivatives experienced a breakthrough year: in addition to the previously mentioned new platforms like Hyperliquid that caused decentralized perpetual trading volume to surge, new products also launched in decentralized options and interest-rate derivatives. On the data side, total value locked (TVL) in DeFi derivatives doubled during the year to approximately $12 billion.

At the same time, tokenization of traditional assets such as U.S. stocks reached a fever pitch: multiple startups and platforms introduced on-chain trading versions of well-known U.S. stocks and ETFs. For example, the Solana-based xStocks project attracted a cumulative circulating market value of $185 million in tokenized U.S. stocks within a single year, signaling that mainstream equities had begun trading in the form of public-chain tokens.

Tokenized equity in some pre-IPO unicorn companies also started pilot issuances on compliant private chains. Even tech giants like Meta under Zuckerberg were rumored to be exploring on-chain versions of their own stock to enable 7×24-hour cross-border trading. In critical infrastructure, payment giants such as Visa and Stripe also entered the space, partnering with blockchains like Solana and Stellar to develop settlement solutions for security tokens.

Third, prediction markets exploded in popularity in 2025: following the U.S. Commodity Futures Trading Commission (CFTC)’s approval in November for Polymarket to resume serving U.S. users, major tech and financial platforms rushed to enter this emerging field. Mainstream trading apps like Robinhood and Coinbase added prediction market features, while sports-betting companies such as DraftKings began experimenting with event contracts. Even Yahoo Finance announced it would launch a dedicated prediction markets section, and Google planned to integrate data from Kalshi and Polymarket for queries.

The market expects prediction markets to experience a “gold rush” similar to the early days of online sports betting, with dozens of platforms potentially competing for users in 2026. However, regulators remain cautious — this year eight states already sent cease-and-desist letters to platforms offering sports-related prediction contracts,deeming them unlicensed gambling operations; Massachusetts, New Jersey, and others filed lawsuits against Kalshi and similar platforms demanding they halt services in those jurisdictions. Although the CFTC has not banned nationwide event-contract trading (classifying them as distinct from illegal gambling), the ongoing state-level regulatory battles continue.

We observe that prediction markets sit at the edge of legalization: issues such as identifying and preventing insider trading and outcome manipulation are receiving intense scrutiny. It is foreseeable that regulators will soon require disclosure and review of participants’ financial interests in related events to prevent moral hazards like “betting on one’s own outcome.” If properly managed, prediction markets have the potential to become a new class of information-forecasting tool and alternative investment vehicle; if allowed to grow unchecked, however, they could also spark fresh financial disorder.

8.Leverage Deleveraging Extreme Stress Test: The October 11 Single-Day Mega-Liquidation and Instant Liquidity Collapse

Market Drawdown Illustration, Source: OSL Research.

October 10, 2025: U.S. President suddenly announces plans to impose 100% tariffs on all Chinese imports, triggering violent global market turmoil.Under the combined pressure of high leverage and fragile sentiment, the crypto market suffered a lightning-fast crash: Bitcoin plunged more than 30% within hours, and total liquidations across the industry reached a record $19 billion in 24 hours. Cascading forced closures caused liquidity to evaporate almost instantly.

Although the Federal Reserve’s easing expectations remained intact and Bitcoin managed to hold the $110,000 level at the time, market confidence took a severe hit. Industry observers likened the flash crash to the March 2020 global stock-market meltdown, highlighting how acutely sensitive crypto has become to macro policy shocks and how its transmission mechanisms lack meaningful buffers.

While institutional buying on the dip later helped stabilize and gradually repair the market, the October 11 event stands as a stark risk warning: crypto is now deeply embedded in the global macro narrative. Single-day extreme volatility is no longer a “low-probability” outlier — risk management must evolve in lockstep with this integration.

9.“Crypto-Stock Linkage” Trading Paradigm: Diffusion of Crypto Treasury Narratives and Valuation Premium Cycles

Michael J. Saylor, founder of MicroStrategy. Image source: The Block.

This year, a wave of speculative fervor around “crypto-stock linkage” has swept the market. Many investors have rushed to buy shares of publicly listed companies that hold substantial amounts of cryptocurrency, commonly dubbed “Digital Asset Treasury.” MicroStrategy (now renamed Strategy Inc.), as the publicly traded company with the largest Bitcoin holdings, has attracted intense attention: by year-end, the company held approximately 671,268 bitcoins, accounting for roughly 3.2% of Bitcoin’s total supply.

In addition, a number of other companies—including Marathon, Tesla, and others—also hold significant amounts of Bitcoin, bringing the total Bitcoin holdings of all publicly listed companies to approximately 1,087,857 coins. As Bitcoin’s price surged to new highs this year, the share prices of these companies rose in tandem, leading some investors to treat them as an alternative form of “Bitcoin ETF.”

The massive inclusion of cryptocurrency on corporate balance sheets may be planting the seeds of systemic risk. In the second half of the year, voices began to emerge calling MicroStrategy “the next black swan.

10.Global Stablecoin Regulation Path Becomes Clearer: From Framework Formation to Detailed Implementation

Source:European Central Bank.

In 2025, stablecoins were increasingly discussed at the “currency and payments” level across more jurisdictions, with regulatory concerns gradually converging on several common core issues: First, stablecoins lack legal tender status, yet the public often develops the misconception that they are equivalent to fiat currency in practical use, making institutionalized consumer protection and risk disclosures essential. Second, once stablecoins achieve significant scale in payment and store-of-value scenarios, they begin to touch the boundaries of monetary sovereignty and seigniorage rights, which in turn can affect domestic monetary policy transmission, the liability structure of financial institutions, and the stability of payment systems.

Third, while cross-border circulation efficiency improves dramatically, it becomes far more difficult to maintain consistent identity verification, anti-money laundering, and sanctions compliance requirements throughout the entire chain; regulators therefore naturally place greater emphasis on “verifiable reserves, clear redemption arrangements, and accountable intermediary responsibilities.”

In the United States, legislative developments in 2025 made the regulatory framework for payment stablecoins significantly more predictable, leading to a more unified market understanding of issuers, reserve assets, information disclosure, and compliance obligations. The European approach aligns closely with these considerations, with a strong focus on financial stability and consumer protection: through more detailed authorization, disclosure, and operational constraints, the EU aims to reduce potential spillover effects of stablecoins on payment systems and monetary policy, while strengthening proactive management of systemic importance risks.

At the same time, certain markets in 2025 noticeably strengthened risk warnings and enforcement actions related to stablecoins, emphasizing their potential for abuse in cross-border fund flows, money laundering, and fraud schemes, and adopting a more cautious attitude toward “institutionally endorsed” promotion. During this period, the People’s Bank of China continued to maintain a stricter risk-management stance, remaining highly sensitive to issues of legal tender status, compliance penetration challenges, and potential financial security risks, while systematically reducing the space for related gray-area activities through regulatory coordination and enforcement actions.

Overall, the key change in 2025 was that stablecoin regulation shifted from broad macro-level attitudes to enforceable, detailed rules. Differences in local implementing regulations began to determine the actual operational space available. For the industry, the core difficulties of cross-regional operations increasingly centered on operational details: whether reserve and disclosure mechanisms can remain stable over the long term, whether redemption channels can withstand stress testing, and whether compliance processes can form auditable closed loops.

2.3:Global Macro: From “End of Tightening” to “Formation of Easing” — Risk Assets’ Pricing Anchor Shifts Again

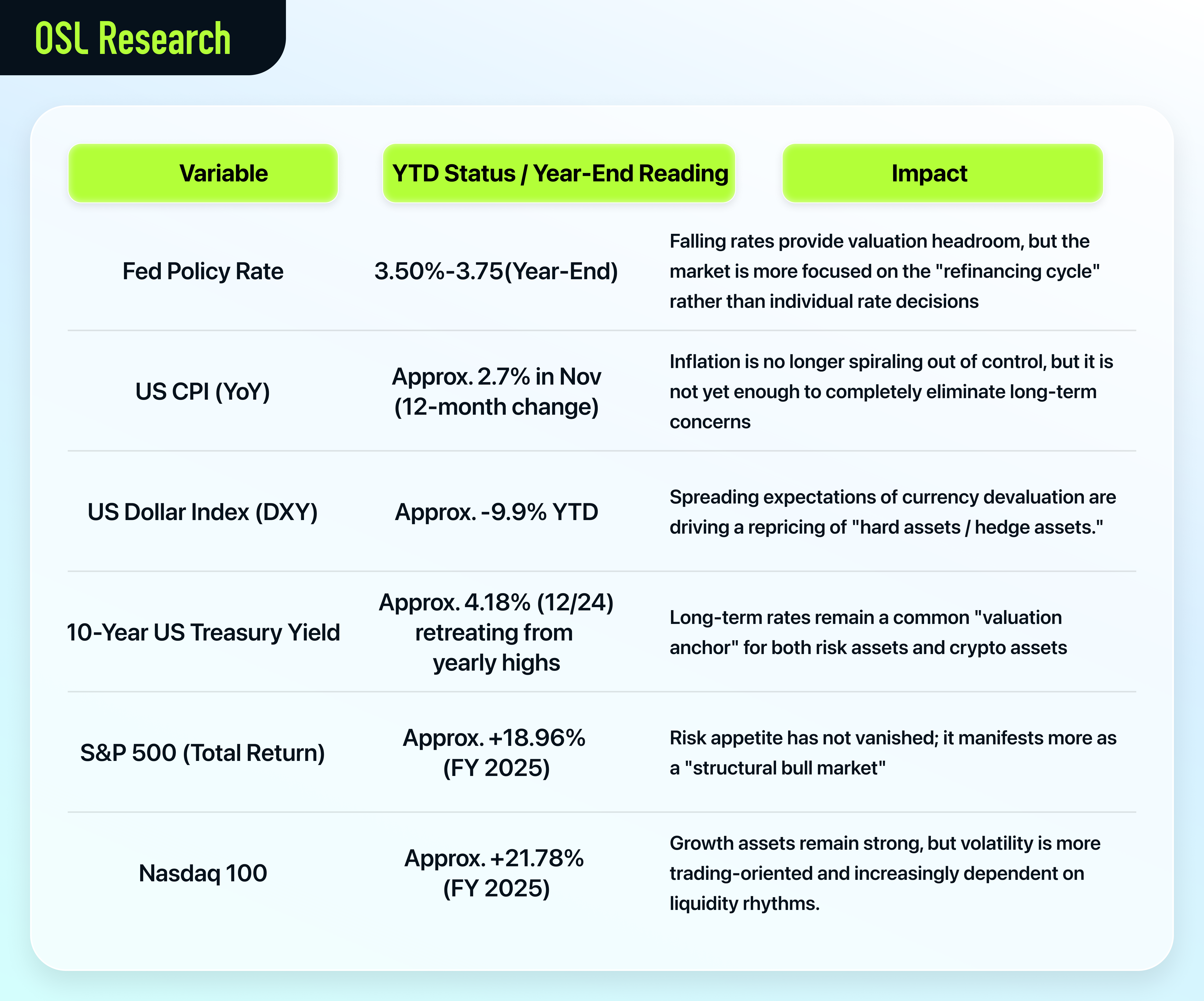

Looking back at 2025, the most intuitive storyline is the unprecedented synchronization of global monetary policy direction. Major central banks completed their transition from the 2022–2023 “inflation-crushing” phase to the 2025 mandate of “safeguarding growth and preserving financial conditions,” and the pivot was decisive.

According to Reuters’ tracking, the world’s major central banks delivered a combined total of 32 rate cuts in 2025, amounting to a cumulative 850 basis points — the most aggressive and concentrated easing cycle in over a decade. Japan stood out as one of the few exceptions, remaining firmly on its hiking path to complete the long-overdue “exit from ultra-loose policy” normalization.

This year, the United States mainly followed a rhythm of “hold steady first, then cut later”: the federal funds rate remained unchanged throughout the first half, with continuous cuts only beginning in the second half, bringing the policy rate range down to 3.75% (by the December FOMC meeting). Meanwhile, inflation did not return to a reassuring “smooth downward” trajectory; instead, it exhibited a sticky, gradual decline — the November CPI print came in at 2.7% year-over-year, sufficient to convince the market that “the direction of rate cuts is correct,” yet not enough to make rate-cut expectations entirely one-sided.

Two “background noises” became increasingly prominent in the macro narrative as 2025 progressed: First, trade and geopolitical frictions further weighed on business and household sentiment. U.S. consumer confidence weakened again toward year-end, with tariffs and living costs frequently cited as key pressures. Second, precious metals directly translated the emotions of “de-dollarization, safe-haven demand, and rate-cut expectations” into price action: gold surged more than 70% for the year and set fresh all-time highs in December, while silver and platinum also delivered exceptionally strong annual performances.

For the Web3 industry, this macro combination carried little romance: marginal improvements in liquidity provided breathing room for risk assets, yet the combination of “sticky inflation, tariff uncertainty, and the explosive rally in safe-haven assets” pulled investor preferences back toward harder, more mature stores of value. As a result, it became increasingly difficult in 2025 for the crypto market to be lifted uniformly by any single narrative. Structural differentiation became the new normal.

2.4 :Web3 Macro: On-chain Dollars, Institutional On-ramps, and Leverage Credit

The global macro has its own grand climate; Web3 has its own micro-climate.Web3 possesses its own distinct set of financial conditions.

These are not perfectly equivalent to the federal funds rate; instead, they resemble the superposition of three primary forces — the quantity of on-chain dollars and the smoothness of their circulation; the channels through which institutional capital enters and the speed at which it exits; and whether leverage and credit are expanding or contracting. It is precisely these three dynamics that explain why, throughout 2025, the market so frequently exhibited a pattern of “tides that rise and fall, but rarely sustain momentum.”

We believe that in 2025, the primary macro-level liquidity contributions to the industry came from three main forms: 1. Stablecoins, 2. ETFs and DATs, 3. Derivatives and Credit (DeFi).

a. Stablecoins: From exchange pricing tools to legislatively defined “payment settlement assets”

On July 18, 2025, the U.S. President signed the GENIUS Act into law, establishing a federal regulatory framework for stablecoins.

The Act requires stablecoins to be fully backed by high-quality liquid assets such as cash and short-term Treasuries, with monthly public disclosure of reserve composition. Its symbolic significance is profound: for the first time, stablecoins were formally incorporated into the language of national financial governance as “regulable payment instruments,” moving beyond mere market-driven industry conventions. Institutionalization has tangible effects that manifest in the “supply curve.”

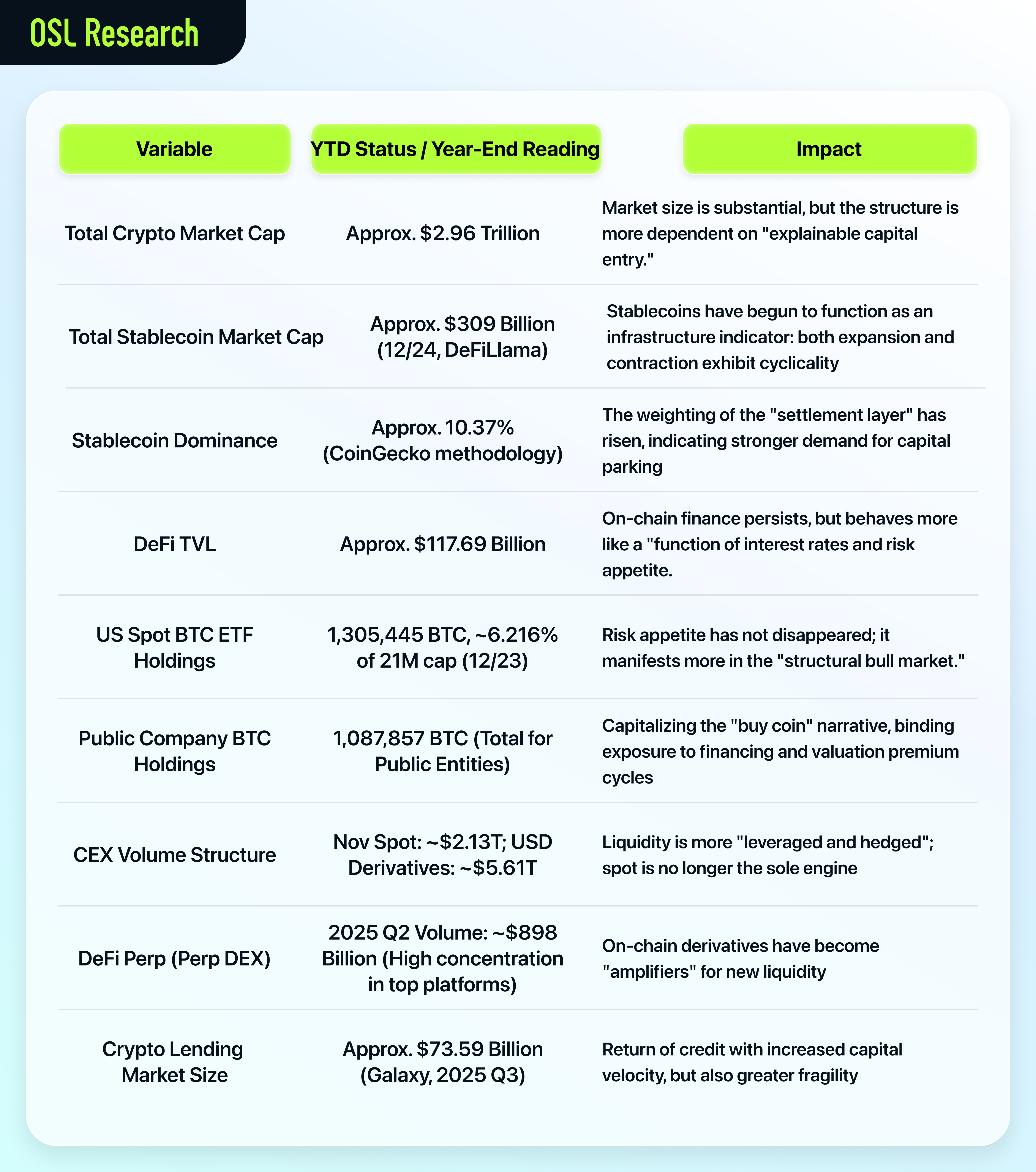

As of December 24, the total stablecoin market capitalization stood at approximately$310.1 billion according to DeFiLlama. The critical insight here is not the absolute size, but the fact that this figure increasingly behaves like a financial infrastructure indicator: it expands more rapidly in macro tailwinds, slows or even experiences localized contractions in macro headwinds or tightening regulatory environments — stablecoins are beginning to exhibit the cyclical characteristics of a “shadow dollar settlement layer.”

The U.S. Treasury, bypassing the Federal Reserve, has carried out a structural reform of the American monetary system. The ingenious design of the GENIUS Act effectively turns every digital dollar into a statutorily authorized purchaser of U.S. sovereign debt. U.S. Treasury Secretary Scott Bettison publicly forecasted: “By 2030, the stablecoin market capitalization will grow from the current $300 billion to between $2 trillion and $3 trillion.” This is no longer a slogan — it is a target. This is not traditional quantitative easing; it is privatized quantitative easing.

b. ETFs and DATs: Moving crypto beta from exchanges into mainstream capital’s risk-control frameworks

“Sovereign debt refinancing pressure” has diffused longer-term monetary depreciation expectations across markets; what truly made 2025 different is that this set of expectations began to be continuously absorbed through two channels: ETFs standardized the exposure, while DATs capitalized it in public equity markets.

The former absorbed capital into a configurable asset framework using just 6.2% of supply — as of December 23, U.S. spot Bitcoin ETFs collectively held 1,305,445 BTC, with the capital side forming a daily-trackable pattern of net inflows/outflows (cumulative net inflows approximately $57.058 billion; around holidays, ETFs also exhibit traditional-style rebalancing outflows, with a combined single-day net outflow of approximately -$188.6 million on December 23).

More importantly, this “standardization” has caused Bitcoin to increasingly resemble a macro asset that can be incorporated into risk budgets: traditional capital no longer needs to navigate exchange account opening, custody, and compliance frictions to execute allocations — those decisions can now be written directly into portfolio management systems. As a result, price behavior has come to resemble that of traditional risk assets: faster entries and exits, more fragmented rhythm, and volatility increasingly driven by risk-control and position-adjustment mechanics rather than pure emotion.

At the same time, DATs translated the same exposure into stock-market language: publicly listed companies collectively held 1,087,857 BTC, with Strategy’s highly concentrated 671,268 BTC position meaning this channel remains more dependent on the financing capacity and valuation premium cycles of a small number of leading entities, and is more prone to “writing” crypto volatility directly into share prices and capital structures.

The side effects of this capitalization also appeared earlier: exposure is now influenced not only by crypto prices, but also by index rules, accounting standards, and regulatory attitudes. For example, on December 19, 2025, MSCI solicited public comments on “whether companies with excessively high digital asset holdings should be excluded from indices.” The mere existence of the discussion is telling — once exposure is placed within mainstream equity frameworks, its expansion ceiling is no longer determined solely by risk appetite, but also by the rule system itself.

c.Derivatives and Credit: Turning “water level” into “wave height” — the leverage syste

In 2025, the on-chain leverage system went through a classic cycle of first expansion, then deleveraging. In the first half, as the spot market warmed and ETF expectations built, investor risk appetite rose sharply. Leverage positions on decentralized lending platforms and synthetic asset protocols increased significantly. Many DeFi lending platforms saw stablecoin loan volumes double from the start of the year, with rates briefly compressing to near-zero spreads, signaling abundant liquidity.

However, the October–November flash crash exposed the fragility of the leverage system: under external shocks, large amounts of margin instantly became insufficient on-chain, triggering cascading liquidations. This not only caused sharp price declines, but also led to a series of credit events — including some on-chain liquidators running out of funds and temporary oracle pricing anomalies. Fortunately, mainstream DeFi protocols withstood the test without systemic collapse, but overall leverage utilization rates fell dramatically.

We observed that after October, on-chain open interest and lending volumes declined approximately 30% from peak levels, indicating a painful deleveraging process. Over the following two months, leverage stabilized at lower levels, with investors returning to a markedly more cautious posture. On the credit side, 2025 also saw some new experiments in DeFi, such as on-chain credit scoring and permissioned uncollateralized lending for select whitelisted institutions — though still small in scale and largely proof-of-concept. Mainstream leverage sources remained over-collateralized lending and perpetual contracts.

Notably, the reversal in the macro interest-rate environment provided some support for on-chain credit: as the Fed began its rate-cutting cycle, traditional money-market rates declined, making on-chain dollar (stablecoin) yields relatively more attractive. A growing number of institutions began exploring DeFi for stablecoin yield generation and arbitrage, helping to anchor on-chain credit activity from the bottom. This was one reason why utilization rates at several top lending protocols recovered after the liquidation episode in the second half.

Overall, the lesson of 2025 is clear: on-chain leverage is a double-edged sword — it amplifies both upside and downside risk. Building more robust deleveraging mechanisms and enhancing the shock-resistance of on-chain credit will be critical challenges for the next phase. After this year’s great wave of cleansing, market participants will apply leverage in a far more rational manner — and regulators will inevitably pay closer attention to this domain to prevent the accumulation of systemic risk.

2.5:Innovation Highlights of 2025

On-Chain Derivatives Innovation – This year, the on-chain derivatives market ushered in vigorous development, with multiple technical and model innovations making this field a focal point.

First, decentralized perpetual contracts platforms bloomed in abundance: in addition to established players like dYdX and GMX, new stars such as Hyperliquid emerged forcefully, achieving trading depth and matching speeds comparable to centralized exchanges through self-built high-performance chains and liquidity incentives. Hyperliquid’s full-year trading volume reached as high as $2.7 trillion. At the same time, the on-chain options market also achieved breakthroughs — decentralized options protocols such as Dopex and Lyra launched more efficient AMM market-making models, with options trading volume and open interest hitting new highs in the middle of the year.

Even more noteworthy is the emergence of on-chain interest-rate derivatives: some protocols began offering fixed-rate/floating-rate swaps (similar to traditional interest-rate swaps), meeting DeFi users’ needs for interest-rate risk management. These innovations enriched the on-chain risk management toolkit, gradually enabling decentralized finance to possess some of the functions of traditional financial derivatives.

The highlights of derivatives innovation also lie in more user-friendly experiences and stronger exploration of compliance. For example, multiple perpetual contracts DEXs began implementing identity verification and geographic blocking to meet regulatory requirements; some projects introduced on-chain insurance pools to provide liquidation protection for high-leverage trading.

Overall, on-chain derivatives have grown from the budding exploration stage of 2020–2021 into one of the tracks with the most intensive capital and talent investment in 2025. This has laid the foundation for attracting professional traders and even traditional hedge funds to enter the field in the next phase, and has also set a new benchmark that decentralized trading does not lose to centralized platforms.

Real-World Asset Tokenization (RWA) – 2025 was called the “Year of RWA” by the industry. Real-world asset on-chain made major progress this year, moving from concept to practical application and attracting high attention from institutions and regulators. First, the tokenization of public-market assets took off: multiple financial institutions in Europe and Asia experimented with trading stocks and bonds through blockchain technology. A digital exchange in Switzerland successfully issued tokenized bonds, and Nasdaq’s private market cooperated with protocols to attempt on-chain registration and trading of unlisted company equity. Particularly noteworthy is the tokenization of U.S. stocks: this year several projects issued on-chain tokenized versions of stocks such as Apple and Tesla through compliant sandboxes.

Among them, the largest in scale was xStocks issuing a basket of tokenized U.S. stocks on Solana, with a total market value of $185 million. Institutional investors can purchase the economic rights represented by these tokens through KYC wallets. Although currently still subject to geographic and quota restrictions, it achieved for the first time 7×24-hour cross-border tradability of U.S. stocks, which is of extraordinary significance.

At the same time, fund share tokenization also made progress: BlackRock issued tokenized U.S. Treasury fund shares on the XRP Ledger through its partner Ondo Finance, providing institutional investors with an on-chain channel to hold short-term U.S. Treasuries. Franklin Templeton’s money market fund also issued tokens on the Stellar network for on-chain subscription, with its scale already exceeding $300 million.

In terms of private-market assets, several landmark cases appeared this year: for example, a real estate project in Asia raised $100 million by issuing Real Estate Profit Tokens (RTP), allowing investors to obtain rental income and property appreciation rights according to their holdings; a French art exchange split ownership of famous paintings into NFTs for sale, realizing fractionalization of artworks.

Regulators in various countries generally maintain an open attitude toward RWA, issuing guidelines one after another to ensure such business is conducted under securities law or financial regulatory frameworks. It can be foreseen that RWA will lead the next wave of institutional liquidity boom.Institutions such as Morgan Stanley predict that by 2030, the global scale of asset tokenization could reach $16 trillion, accounting for approximately 10% of global GDP. This year’s practice has already verified the efficiency improvement and cost reduction advantages of tokenization: the tokenized clearing of one loan reduced settlement time from 5 days to 5 hours. The explosion of RWA not only found a real-world anchor for blockchain, but also opened a new path of cost reduction and efficiency enhancement for traditional finance.

Prediction Markets and Mass Momentum Building – This year, prediction markets flew into ordinary people’s homes, becoming a new breakout scenario for blockchain applications.

The U.S. CFTC adopted a relatively open attitude toward Kalshi, Polymarket, etc., allowing them to operate specific event contracts under strict limits and review mechanisms. This directly detonated market enthusiasm: not only did Crypto circle users pour in, but ordinary sports fans and political enthusiasts also participated in event “guessing” through various platforms.

The cumulative trading volume of prediction markets for the whole year is conservatively estimated to have exceeded $2 billion, representing several times growth compared to 2024. Popular markets include Fed interest rate decisions, U.S. election wins by state, NFL game outcomes, and even Hollywood box office — encompassing virtually everything. Mainstream portals such as Yahoo provided prediction odds lookups, and many event topics on social media posted prediction market probabilities as reference.

For a time, prediction markets were hailed as “a more accurate public sentiment thermometer than polls,” and even academia began researching extracting public expectations from prediction markets. However, behind the explosion, problems also became apparent: for example, some questioned that prediction markets might be exploited by those with insider information, thereby damaging market fairness; sports prediction markets also faced the risk of being turned into gambling, triggering legal challenges in multiple U.S. states.

This year, some state regulators emphasized that even with federal approval, such platforms must obtain state gaming licenses, and Kalshi has already become embroiled in lawsuits in multiple locations as a result.

We expect that next year the game around the legality of prediction markets will continue, and it is not ruled out that it may ultimately be appealed to the Supreme Court to clarify federal and state regulatory responsibilities. Despite the controversy, prediction markets have already shown their potential as a new tool for collective wisdom: if regulators can guide them well and establish transparent participant restrictions and information disclosure systems (such as requiring public officials not to participate in prediction trades related to themselves), then prediction markets are expected to play a positive role in commercial forecasting, public policy and other fields; conversely, if left unchecked, they may also become breeding grounds for gambling or manipulation.

The explosion in 2025 is only the prelude; whether prediction markets can enter the compliant track in 2026 will determine whether this innovation is a flash in the pan or truly stands firm.

3.Our Analytical Framework

Through the above review, we have established an analytical framework for the “second half” of Web3 development: with on-chain dollar supply as the foundation, compliant capital inflows as the driver, and leverage credit expansion as the amplifier — these three elements together shape the industry’s business cycle and risk profile.

More specifically, we will focus on monitoring the following indicators and signals:

3.1 On-Chain Dollars and Stablecoin Supply & Demand:

The scale and growth rate of stablecoin market capitalization serve as leading indicators for measuring on-chain liquidity. This year, stablecoin supply showed a certain degree of decoupling from overall market performance, and at times even exhibited an independent upward trend. This indicates that stablecoins have become the “shadow dollar” in the digital economy, with their supply and demand being jointly driven by macro-financial conditions and application-level demand.

In our framework, incremental growth in stablecoins is regarded as the fuel for the second-half market cycle: as long as compliant stablecoins continue to expand, the on-chain ecosystem will have sufficient “ammunition.” Conversely, if regulatory restrictions or risk-averse sentiment cause stablecoin supply to contract, on-chain activity will be noticeably suppressed. Therefore, developments in stablecoin regulation (such as legislation in major economies and the attitudes of central banks in various countries) as well as market penetration (corporate adoption cases, cross-border usage examples) are the primary focus areas in our framework.

The experience of 2025 has already demonstrated that the cyclical nature of stablecoin supply is closely tied to the macro environment. We expect this correlation to become even stronger in the second half, while various countries may introduce measures — such as restrictions on the proportion of dollar stablecoin assets that banks are allowed to hold — to safeguard the status of their domestic currencies. All of these will be incorporated into our framework considerations.

3.2 Institutional Capital Inflows and Outflows:

The main channels through which institutional capital has entered Web3 include ETFs, custody products, compliant token issuances, and industry-strategic investments. We track the behavior patterns of mainstream capital by monitoring ETF fund flows, changes in listed companies’ on-chain holdings, and the degree of bank participation.

A clear feature this year was that, once U.S. policy became clearer, institutional money poured into ETFs, pushing Bitcoin ETF holdings past 1.3 million BTC. At the same time, however, leverage-heavy corporate holders like MicroStrategy faced growing market skepticism, and some traditional mutual funds began removing such exposures.

This tells us that institutions prefer standardized, controllable crypto exposure rather than aggressive, company-level allocations.Our framework adjusts accordingly: we treat ETFs and similar “off-balance-sheet” exposures as positive momentum indicators, watching whether they can keep absorbing spot coins and dampening volatility; we treat DAT-style “on-balance-sheet” exposures as risk factors, alert to the stampede potential of over-concentration. Fortunately, late-2025 saw an encouraging shift in global regulatory tone—for example, the Basel Committee in November announced a re-evaluation of its proposed risk-weighting for banks’ crypto assets, which could ease previously stringent capital rules.

That suggests banks and other financial institutions may become more willing to engage with digital assets in the next few years.Our framework therefore anticipates more traditional-institution entry in 2026, including asset managers launching on-chain products and commercial banks offering stablecoin services. At the same time, we watch for potential outflow risks: whether a macro reversal or regulatory pivot could trigger ETF redemptions, bank lending pullbacks, and consequent market shocks.

3.3 Leverage and Credit Cycles:

Leverage ratios often determine the amplitude of market volatility and serve as the catalyst for bull-to-bear transitions. Our framework incorporates indicators such as total on-chain open interest in perpetual contracts, leverage multiples in DeFi lending, and liquidation volumes for monitoring.

This year’s October–November event vividly demonstrated the risks of high leverage. Therefore, we will closely monitor early signs of leverage re-inflation in the future — for example, sustained positive funding rates and long-biased positioning in perpetual contracts, abnormally low stablecoin borrowing rates, and similar signals. Once leverage utilization approaches historical peak levels, our framework will issue risk warnings.

On the credit-expansion side, if new forms of uncollateralized lending emerge or on-chain credit networks grow rapidly, we will also evaluate the resulting systemic implications. Currently, on-chain credit remains in its early stages, with changes more heavily influenced by isolated events. However, in the second half, if traditional financial institutions begin participating in DeFi lending or issuing on-chain credit instruments, this process could accelerate significantly.

Our framework assumes that, in the absence of a central bank acting as lender of last resort, on-chain credit cycles will be shorter and more violent — necessitating higher-frequency data and more timely risk-control responses.

Overall, we view leverage and credit as the “amplifier” of market moves: they fan the flames in tailwinds and pour fuel on the fire in headwinds. The sharp volatility of 2025 has already validated this dynamic. In 2026, we expect both regulators and the market to place greater emphasis on smoothing leverage fluctuations — for example, through the introduction of on-chain “circuit breakers,” upgraded oracles, improved liquidation mechanisms, and similar measures. We will track these developments and incorporate them into our assessment of future market quality.

Through the above framework, we will be able to interpret the development trajectory of Web3’s second half in a more systematic manner. On this basis, we present our five major predictions for 2026, together with a discussion of their implications for the industry and potential risk signals.

4.2026 Outlook and Predictions

4.1.OSL Research Five Major Predictions for 2026:

Prediction 1: Bitcoin Maintains a $75,000–$140,000 Range-Bound Oscillation, Entering the Sequence of Mature Financial Assets.

We judge that in 2026, Bitcoin will find it difficult to replicate the multi-fold surges or crashes characteristic of past cycles. Its price will primarily fluctuate within an institutionally anchored range, behaving more like mature assets such as gold. This stems first from the widespread participation of institutions, which has already significantly reduced volatility: Bitcoin’s annualized volatility in 2025 fell to 23%, comparable to the S&P 500 index. With giants such as BlackRock absorbing massive capital through their ETF products, Bitcoin’s valuation is increasingly constrained by “rational money.”

Since its launch, BlackRock’s Bitcoin Trust (IBIT) has cumulatively attracted $62.5 billion in inflows, yet Bitcoin’s price throughout 2025 showed only modest net gains — peaking in October before pulling back, while ETF funds continued to flow in steadily on dips. This pattern indicates that Bitcoin is transitioning into a “high-level oscillation with gradually rising center of gravity” slow-bull regime, markedly reducing the probability of violent bubbles and subsequent implosions. Second, Bitcoin’s correlation with macro assets has strengthened, and its dual identity as both “digital gold” and a risk asset is gaining broader recognition among investors.

During the Fed’s rate-cutting cycle, both gold and Bitcoin benefited from demand, but Bitcoin’s upside remained more restrained; conversely, in risk-off periods dominated by safe-haven flows, Bitcoin’s drawdowns were also more contained. These signs suggest Bitcoin is shedding its label as a purely “independent speculative asset” and is increasingly being integrated as one component of global asset allocation. We expect that in 2026, Bitcoin will spend the majority of the year oscillating within a relatively wide but defined range ($75,000–$140,000), with any short-term breakout requiring significant fundamental or policy catalysts. This effectively marks Bitcoin’s full maturity: like other major asset classes, it has entered the era of institutionalized trading. Market participants will increasingly focus on its long-term value proposition — such as inflation hedging and digital-gold status — rather than chasing explosive upside or downside. Importantly, Bitcoin’s maturation does not mean the absence of opportunity; it means a more stable risk-reward profile.

It may no longer serve as the source of “10× myths,” but it is poised to become a cross-cycle, steadily appreciating allocation asset. From an industry perspective, this shift helps foster a more stable market environment, attracting more conservative, long-term capital while substantially reducing the negative spillovers that past cyclical bubble bursts inflicted on the broader ecosystem.

Prediction 2: Tokenization of Traditional Financial Assets Will Clearly Accelerate and Become the Key Main Theme Driving Incremental Institutional Liquidity.

We firmly believe that asset tokenization (Tokenization) will become one of the hottest themes in 2026, attracting substantial institutional capital and infrastructure investment.

Following the proof-of-concept pilots in 2025, the technical and legal obstacles to bringing traditional financial assets on-chain have been significantly reduced. As regulators in various jurisdictions progressively clarify the legal status of tokenized securities (such as the EU’s MiCA extension to security tokens, and dedicated guidelines for tokenized bonds/funds issued by Hong Kong and Singapore), 2026 will witness the launch of many more substantive products.

We anticipate several priority breakthrough areas:

Tokenization of government bonds and central bank bills — Given their high credit quality, strong liquidity, and relative ease of regulatory approval, these are likely to lead the way, with issuance by sovereign entities or major financial institutions. For instance, it is not ruled out that the U.S. Treasury could experiment with “blockchain Treasuries,” or that the European Investment Bank could issue additional digital bonds on Ethereum. Should such initiatives materialize, they would significantly enable banks and funds to allocate directly to bond assets through on-chain channels, greatly enhancing efficiency.

In the realm of stock tokenization, we expect large multinational corporations or exchanges to launch regulated tokenized equity markets. Institutions such as Nasdaq already have related plans in place; 2026 could see the rollout of an SEC-regulated digital securities trading platform that allows qualified investors to trade tokenized versions of select listed stocks and ETFs on a 7×24-hour basis.

Tokenization of private/unlisted equity and fund shares will also gain momentum: private equity powerhouses such as Blackstone and KKR may issue tokenized shares of their flagship funds to broaden funding sources and improve liquidity. Real-world assets such as real estate and commodities will follow: jurisdictions like Dubai and Singapore may see the emergence of officially supported tokenized real-estate exchanges, enabling investors to purchase property NFTs by square footage and receive proportional rental income.

The essence of this wave lies in channeling tens of trillions of dollars of traditional financial liquidity into the on-chain ecosystem. This will not only inject enormous incremental capital into the crypto industry, but will also compel on-chain infrastructure to undergo comprehensive upgrades in performance, compliance, and user experience.

Given the strong emphasis that financial institutions and regulators worldwide are placing on tokenization (the World Economic Forum estimates that by 2030, 10% of global GDP will be stored on blockchain), we have a strong reason to believe that 2026 will mark the inflection point of this trend. Landmark events that may occur include: the launch of the first cross-border tokenized securities settlement network led by a major Wall Street bank; more than half of the world’s top ten asset managers introducing dedicated digital asset strategies or product lines. An institutional liquidity boom will follow — reminiscent of the early stages of the 1990s internet bubble, with large amounts of venture capital and traditional capital flooding into tokenization-related startups and projects.

Without question, this represents an enormous tailwind for the entire Web3 industry: it truly brings blockchain into the core of mainstream finance, transforming “on-chain capabilities” from something confined to native crypto assets into a powerful tool capable of reshaping the entire financial market. Of course, we must remain rational: every boom is accompanied by risks. The health of pricing and secondary liquidity for tokenized assets will ultimately determine whether this wave can proceed steadily and endure in the long term.

Prediction 3: Countries Will Adopt Stablecoin Payments at Scale, with Scenario Expansion Concentrated in Real Consumption Areas Such as Cross-Border Payments, E-Commerce Settlement, and Gaming Ecosystems.

We judge that in 2026, stablecoin payments will enter a period of large-scale adoption in more countries, with incremental use cases concentrated in several “high-frequency, cross-border, quantifiable cost-reduction” pathways: cross-border B2B settlement and supply-chain payments (shortening receivables cycles and reducing intermediary bank and multi-layer channel costs), platform-merchant collection and e-commerce settlement (multi-currency acquiring and merchant settlement for overseas e-commerce, travel consumption, etc.), and high-frequency micro-payments and revenue-sharing settlement within gaming ecosystems (instant settlement needs for top-ups, subscriptions, in-game item transactions, content and advertising revenue shares, etc.).

The driving force comes from the synchronized integration of payment networks and enterprise cash-management products, shifting stablecoins from “usable” to “scalable for operations.” Visa announced in December 2025 the launch of stablecoin settlement in the United States, disclosing that as of November 30, 2025, its monthly stablecoin settlement volume had reached an annualized run rate of $3.5 billion. Stripe, meanwhile, introduced Stablecoin Financial Accountscovering 101 countries and regions, enabling enterprises to handle stablecoin and traditional financial-rail receipts/payments, fund pooling, and cash management within the same backend.

Countries that scale earlier will follow two main paths: demand-driven and financial-center-driven.

Demand-driven markets are exemplified by Latin America. The Governor of the Central Bank of Brazil noted at a BIS event that approximately 90% of crypto flows in Brazil are related to stablecoins, primarily for overseas shopping and payments. On the regulatory side, stablecoin-related transactions are gradually being incorporated into the foreign-exchange framework, with plans starting from February 2026 to classify and report stablecoin operations more stringently under foreign-exchange transaction attributes.

Financial-center-driven markets place greater emphasis on “expansion within guardrails.” Singapore’s MAS has already implemented a single-currency stablecoin regulatory framework; Hong Kong’s stablecoin issuance regulatory regime took effect on August 1, 2025, requiring licensing for relevant activities; the UAE Central Bank has issued the Payment Token Services Regulation (PTSR) to govern payment token services through licensing and rule-based systems.

If mainstream acquiring networks continue to disclose rising stablecoin settlement volumes in 2026, more merchant networks open stablecoin acceptance, and enterprise-side cash management and compliance modules continue to be productized and pushed downward, then the pace of adoption expansion is likely to accelerate further — spilling over more quickly from “cross-border and platform scenarios” into broader consumer payment pathways.

Prediction 4: Prediction Markets Will Form a Referencable “Event Risk” Pricing Benchmark and Enter the Stage of Institutionalized Trading and Professional Market-Making.

We judge that in 2026, prediction markets will continue to expand and gradually establish themselves as a “layer for pricing event risk” that institutions can reliably reference. Their core value lies in compressing discrete macro shocks — such as economic data releases, policy implementations, and regulatory milestones — into tradable probability curves, transforming risk from narrative discussion into a quantifiable, hedgeable framework.

KalshiData’s year-end 2025 figures already provide a sufficiently clear baseline: full-year nominal trading volume reached $23.8 billion, with a December monthly peak of $6.38 billion, representing year-over-year growth of +1,108%. At the same time, month-end open interest stood at approximately $370 million, signaling rising capital commitment and the emergence of a “position-driven” market dynamic.

The degree of institutionalization in 2026 can be assessed through two observable signals: whether open interest continues to scale upward on a more stable platform basis, and whether clearing and settlement channels continue to broaden their coverage.

The former determines the depth of the hedging liquidity pool; the latter determines the friction coefficient for traditional capital to enter. If open interest rises from the hundreds-of-millions level to the multi-billion-dollar scale, and exhibits more regular position buildup and adjustment around key events such as inflation prints, interest-rate decisions, and regulatory milestones, the probability curves generated by prediction markets will increasingly approximate a standardized benchmark. At that point, institutional adoption will shift from mere “participation” to genuine“reliance.”

Prediction 5: The “Crypto Treasury” Model Fades, and MicroStrategy Enters a Critical 12–24 Month Test Period.

We expect that, as compliant investment channels rise and digital-asset volatility moderates, the “treasury model” of amplifying crypto exposure through listed-company Bitcoin holdings will gradually recede.

Extreme holders such as MicroStrategy (Strategy Inc.) face a severe test: if Bitcoin prices cannot sustain significant further upside, the company’s heavy debt burden and ongoing interest expenses will become increasingly difficult to service. Specifically, Strategy currently carries approximately $8.2 billion in debt and preferred stock, requiring roughly $779 million in annual interest and dividend payments. Its average Bitcoin acquisition cost stands at about $74,972 per coin. Based on Bitcoin’s year-end price of around $90,000, the company’s unrealized book gain is less than 20%, while its share price has already halved from its intra-year high, leaving the market capitalization at only ~75% of the net asset value of its Bitcoin holdings. Investors are applying a significant discount, reflecting concerns that the company may be forced to issue large amounts of additional equity or sell Bitcoin holdings.

We view the next 12–24 months as the critical test period for treasury-model companies. Smaller-cap imitators that heavily accumulate Bitcoin in a similar fashion are also likely to fade from the market as their valuation premiums evaporate.

More broadly, institutional investors will increasingly favor obtaining crypto exposure through ETFs or regulated funds rather than purchasing high-leverage shadow-ETF stocks such as Strategy. The fact that MSCI has already discussed excluding companies with excessively high digital-asset holdings from indices indicates that mainstream markets are actively correcting these risks.

We predict that in 2026, companies like MicroStrategy will gradually be marginalized. This will serve as an important signal that the industry is moving away from unconventional financial-engineering speculation and toward an era of transparent, pure investment.

5.Industry Impact

If the above outlook materializes, it will exert profound influence on all participants across the Web3 industry. We believe the main effects will manifest in the following areas:

(1) Business Model Transformation and Compliance Becoming Essential for Survival

After the trials of 2025, the industry has come to understand that the “guerrilla era” is ending and the “regular army era” has arrived.

Cryptocurrency exchanges, wallets, lending platforms, and other types of crypto enterprises must proactively adapt to regulatory requirements and adjust their business models. Specifically, centralized exchanges (CEXs) will accelerate their transition toward compliant operations: industry giants that previously grew aggressively in gray zones will either complete a phoenix-like rebirth by obtaining licenses in major markets or gradually shrink and be cleared out in the competitive landscape.

Following the introduction of more accommodative policies in the United States this year, compliant exchanges such as Coinbase have relatively risen in prominence, while certain small unlicensed exchanges have already become difficult to find in terms of liquidity. This foreshadows that more than 80% of future trading volume will concentrate on licensed, compliant platforms, with the remaining unlicensed venues either retreating to the shadows or being shut down through enforcement. In the DeFi domain, the shift will be from “anonymous and borderless” to “identity-traceable and rule-monitorable.” Regulators have come to recognize that rather than attempting to ban decentralized protocols outright, it is more practical to bring key choke points under supervision. For example, many DeFi front-ends have begun integrating on-chain identity authentication (DID) and sanctions-list filtering — a practice that will become the mainstream standard in 2026.

Decentralized protocol teams will need to collaborate with auditors and compliance firms to establish real-time compliance reporting and risk-control mechanisms; otherwise, they will be cut off from mainstream liquidity. One positive consequence of stronger regulation is that law-abiding, compliant players will enjoy significantly larger market space and greater trust, while illicit arbitrageurs will find nowhere to hide. For instance, through industry compliance alliances such as the Beacon network, more than 75% of crypto trading volume is now already included in real-time suspicious-activity sharing mechanisms, and this proportion will only increase going forward. This means that hackers and money launderers who previously succeeded repeatedly will find it increasingly difficult to evade detection.

For enterprises, investing in compliance is investing in the future: those who first meet regulatory standards and secure licenses will capture new users and institutional partnership opportunities ahead of others. Conversely, projects that continue to fantasize about operating outside the bounds of regulation will discover themselves isolated from the mainstream financial system. In short, compliance has transformed from a cost center into an indispensable requirement for survival — and in 2026, this reality will become even more unmistakable.

(2) Deep Involvement of Traditional Finance, Accelerating the Formation of a Competitive Landscape

As large institutions and major capital continue to enter space, the boundaries of the Web3 industry will become increasingly blurred, and its integration with traditional finance will enter deep waters. On one hand, financial giants will bring high-quality capital and mature expertise:for example, JPMorgan Chase, Goldman Sachs, and others may launch their own digital-asset custody and trading services, while Fidelity and BlackRock further expand their crypto product lines. This participation will significantly elevate the industry’s professional standards, drive infrastructure improvements, and help enhance market stability and investor confidence.

On the other hand, the entry of traditional giants also means a reshaping of the competitive landscape: they will compete for trading volume, clients, and pricing power, exerting pressure on native crypto companies. It is foreseeable that acquisitions and consolidations will accelerate in 2026: large banks or exchanges may acquire high-quality crypto startups to quickly gain market entry; some older crypto firms with weaker risk resilience will be forced to seek alliances or backers.

For instance, it is not out of the question that companies like Coinbase could form alliances — or even merge — with traditional brokerages or exchanges to share user channels and compliance resources. Industry talent mobility will also intensify: more traditional finance elites will enter crypto space, while crypto natives join Wall Street institutions, creating a situation where each side increasingly contains elements of the other.

Another dimension of competition lies in the contest over technical standards and market rules: large financial institutions tend to favor the rule systems they are familiar with (such as stricter investor suitability requirements and centralized clearing mechanisms), while the crypto industry champions decentralization, autonomy, and “code is law.” Both sides will need to find balance through ongoing negotiation. We believe that in 2026, certain industry consensus standards may emerge — such as institutional-grade smart-contract templates, digital-asset accounting principles, and similar frameworks — making it easier for traditional finance to participate.

In this process, native crypto enterprises should proactively embrace cooperation: rather than resisting, they should leverage their technological advantages to partner with traditional players in market expansion. Visa’s collaboration with Circle this year to launch stablecoin settlement is a classic win-win example. In the future, we will see banks partnering with DeFi protocols on lending, insurers collaborating with oracle projects on risk pricing, and more.

We predict that by the end of 2026, the majority of top-tier Web3 projects will have the visible investment or cooperation footprint of traditional financial institutions behind them. This will substantially enhance the overall credibility and influence of the industry, and it also means that the rules of the game will no longer be determined solely by geeks, but will become integrated into a much broader financial ecosystem.

(3)Upgrade of Industry Service Models to Meet Institutional and Retail Demands.

The experience of 2025 has shown that products designed solely for the small circle of crypto geeks can no longer sustain the industry’s next phase of growth — service models must evolve.

First is the improvement in user experience: the large wave of new entrants consists of traditional institutions and ordinary retail users, who require safe, convenient, and intuitive products.

Institutions demand comprehensive reporting and risk-control interfaces; retail users need simple wallets and reliable customer support. We expect that in 2026, the industry will see a proliferation of custody-grade wallets and platforms — such as wallet applications featuring bank-level account recovery and compliance safeguards, or even digital-asset account services offered directly by banks. These developments will lower the entry barrier and push blockchain applications toward becoming “terminal-consumer friendly.”

Second, revenue models will become more diversified and stable. In the past, the industry relied excessively on “greater-fool” price appreciation to generate returns. In the second half, we will witness the rise of genuine yield-generating businesses. For example, stablecoin deposit and money-market-like products now allow users to earn real interest — this year, BlackRock-backed USDtb stablecoin already offers annualized yields above 5%. Similarly, on-chain Treasuries and on-chain lending provide investors with fixed-income returns comparable to those in traditional markets.