Funding Rates Explained: How Perpetual Futures Fees Signal Market Pressure

Perpetual futures contracts are a core instrument in the crypto derivatives market because they allow traders to maintain exposure to digital assets without dealing with contract expiry. To keep these contracts trading close to the underlying spot price, exchanges use a mechanism called the funding rate.

2026 update: what readers should check first

This refresh turns the topic into a risk-aware market guide rather than a simple price or trend prediction. Readers should look at liquidity, positioning, catalysts, unlocks, and downside scenarios before reacting to headlines.

Signal | How to use it | Key caveat |

|---|---|---|

Liquidity | Check volume, spreads, and exchange depth. | Thin liquidity can exaggerate both rallies and drawdowns. |

Catalyst | Identify whether the move is driven by news, unlocks, listings, or macro factors. | One-off catalysts often fade quickly. |

Positioning | Look at leverage, funding rates, and crowded narratives. | Crowded trades can unwind sharply. |

Risk action | Use smaller sizing, test exits, and avoid treating forecasts as certainty. | Scenario planning is safer than single-price targets. |

Related reading: token unlock risk guide | meme coin volatility | licensed vs offshore exchanges.

FAQ: market-risk interpretation

Is the move supported by liquidity or only by short-term attention?

What event could invalidate the bullish or bearish scenario?

How do unlocks, funding rates, or leverage affect downside risk?

Which data should readers check before acting on market narratives?

Funding payments are periodic transfers between long and short positions that depend on how the perpetual contract price compares to the spot market. They can meaningfully affect the cost of holding a position, especially when leverage is involved or when market conditions are volatile. This guide explains what funding rates are, why they exist, how they are calculated, and how they influence risk and costs for participants in perpetual futures markets.

What is a Funding Rate in Perpetual Futures?

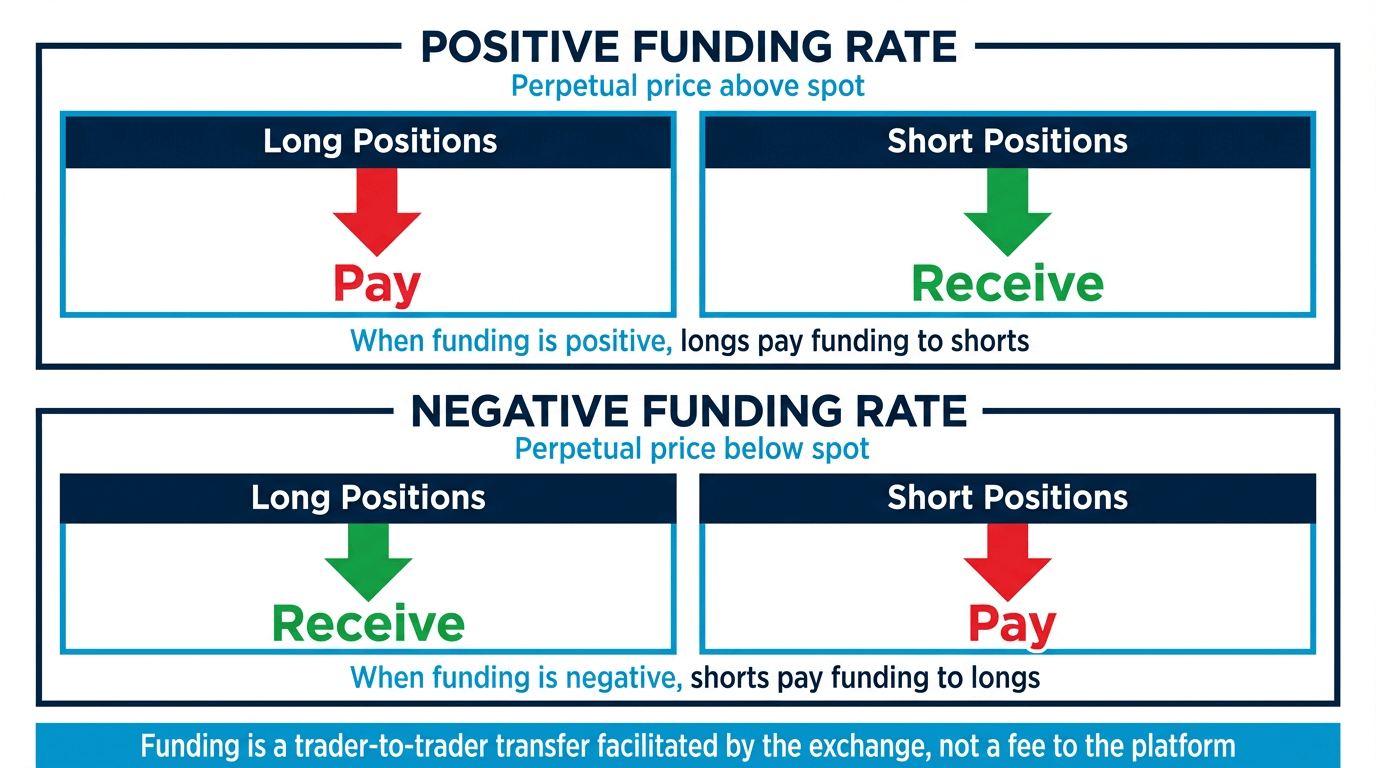

In perpetual futures, the funding rate is a recurring payment exchanged directly between traders who are long and traders who are short on the contract. It is not a fee charged by the exchange, nor is it a fixed commission; instead, it acts as a balancing mechanism inside the derivatives market itself. When funding is due, accounts holding long or short positions will either pay or receive funding depending on the sign of the rate.

The core objective of the funding rate is to keep the perpetual contract price anchored around the underlying spot price of the cryptocurrency. If the perpetual contract trades significantly above spot, the funding rate will typically become positive, increasing the cost of holding long positions and making short positions receive payments. If the contract trades below spot, the rate may turn negative, reversing that flow.

These periodic adjustments are designed so that traders collectively have an economic incentive to bring the perpetual price closer to the spot price. Over time, this mechanism helps maintain price convergence without the need for a fixed expiry date, which is what differentiates perpetual contracts from traditional futures. For anyone trading perpetual futures, understanding that funding is a trader‑to‑trader transfer, and not an exchange fee, is fundamental to interpreting how costs accrue.

Why Funding Rates Exist

Traditional futures contracts have expiration dates. As they approach expiry, their prices tend to converge with the spot price of the underlying asset, because the contract will soon settle based on that underlying market. Perpetual contracts, however, do not expire, so they do not benefit from this natural convergence mechanism. Without some form of adjustment, the perpetual price could drift away from spot and remain at a premium or discount for extended periods.

The funding rate exists to address this structural issue. When the perpetual contract trades at a premium to spot, the market is signaling that demand for long exposure in the derivatives market is stronger than demand for short exposure. To counterbalance this, the funding rate often turns positive, meaning long positions pay shorts at set intervals. This additional cost can reduce the incentive to hold long positions at a large premium and increase the appeal of short positions, nudging the perpetual price closer to spot.

When the perpetual trades at a discount to the spot price, the opposite dynamic can occur. The funding rate may turn negative, so shorts pay longs. This makes it more expensive to maintain short positions and relatively more attractive to hold long positions in the perpetual contract. Again, the economic pressure is directed toward price convergence between the perpetual and the underlying spot market.

In simple terms, funding payments translate market imbalance, whether the contract is trading above or below spot, into a cost or benefit that encourages traders to correct that imbalance. The mechanism is economic rather than purely mechanical, relying on the choices of market participants responding to incentives rather than on automatic settlement at a fixed date.

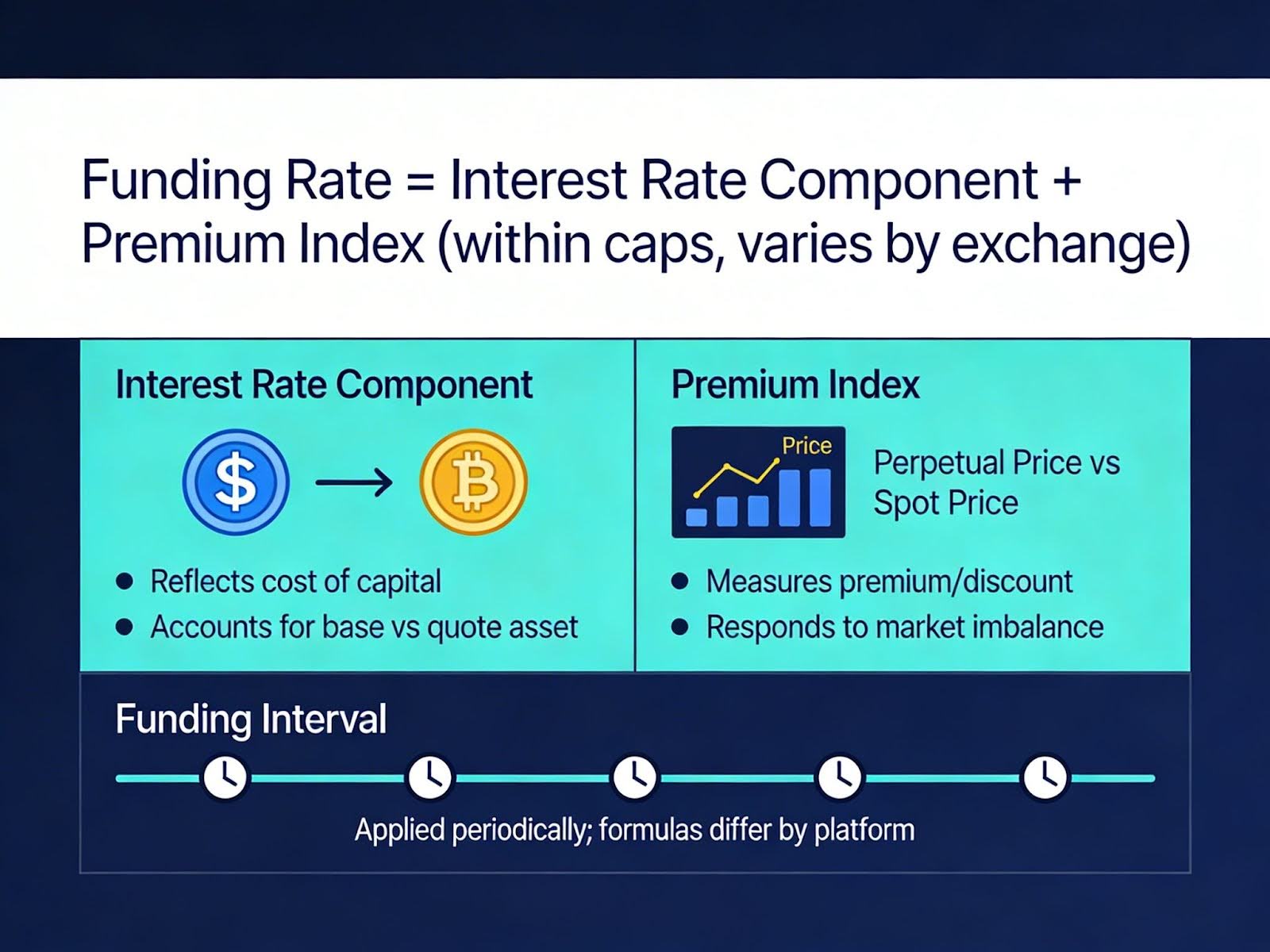

How Funding Rates are Calculated

While the exact funding rate formula can vary from platform to platform, the underlying logic typically relies on a combination of an interest rate component and a premium index. The interest rate component reflects the relative cost of holding the underlying asset versus holding a quote currency (such as a stablecoin). The premium index captures the difference between the perpetual contract price and the spot price over a certain period.

Broadly, the premium index measures whether the perpetual contract is trading at a sustained premium or discount compared to spot. If the contract consistently trades above spot, the premium index will be positive; if it is below spot, the index will be negative. This premium index is a key driver of whether funding is positive or negative and how large it becomes.

The interest rate component is usually relatively stable and can be thought of as an adjustment that accounts for factors such as the cost of capital or the relative returns of holding different assets. Combined with the premium index, it yields a funding rate that can fluctuate over time as market conditions change.

Funding is applied at regular funding intervals—for example, every few hours—so positions are periodically debited or credited based on the current rate and the size of the position. Because formulas differ among exchanges, traders should always review how a specific platform defines its premium index, interest rate assumptions, and calculation intervals. The key takeaway is that funding rates are dynamic, mechanically linked to price differences between perpetual and spot markets, and subject to each venue’s methodology.

Positive vs. Negative Funding Rates

A positive funding rate means that traders holding long positions pay funding to traders holding short positions. This typically occurs when the perpetual futures contract trades above the spot price, indicating stronger demand or a bullish bias in the derivatives market. Under these conditions, longs effectively pay a recurrent cost to maintain their positions, while shorts receive periodic payments.

Conversely, a negative funding rate indicates that shorts pay longs. This tends to happen when the perpetual contract price trades below the spot price, often reflecting a more bearish or cautious sentiment in the derivatives market. In this environment, short positions bear the recurring cost, and long positions receive funding.

Funding direction provides a high‑level view of market sentiment inside the perpetual futures market. Persistent positive funding suggests that long positions are more crowded, while persistent negative funding suggests shorts are more concentrated. However, it is important not to treat funding direction as a predictive signal by itself. It is an indicator of current positioning and price relationship to spot, not a guarantee about where prices will move next.

How Funding Rates Affect Traders

Funding rates directly influence the cost of holding a position in perpetual futures, especially over longer timeframes. For traders using leverage, even relatively small funding payments can become meaningful because they are applied to the notional value of the position, not just the margin posted. When funding is positive and a trader is long, those recurring payments increase the overall cost of maintaining the position; when funding is negative and they are long, the position may receive funding instead.

Over time, funding can accumulate into a significant component of position performance. A trader might enter a position at a certain price and see limited movement in the underlying, yet still experience a material impact on their account from repeated funding debits or credits. This is particularly relevant for participants who hold positions across multiple funding intervals, such as over several days or longer.

During periods of high volatility or when the derivatives market becomes heavily imbalanced in one direction, funding rates can spike, temporarily increasing the cost of holding certain positions. In such environments, funding may interact with leverage and liquidation risk, as higher funding outflows effectively reduce available margin for those on the paying side. These dynamics underline the importance of viewing funding as a core part of the risk profile of perpetual futures, not a minor detail.

Funding Rate Risk Management Considerations

For traders, managing funding‑related risk starts with monitoring funding history and understanding how rates behave across different market conditions. Historical funding data can show whether a particular contract frequently swings between positive and negative or tends to remain on one side for extended periods. This awareness helps frame expectations about the potential cost of holding a position over time.

Periods of heightened volatility or news‑driven events can cause both prices and funding rates to move rapidly. Recognizing these environments and acknowledging that funding may become more expensive or less predictable is an important part of risk awareness. It also connects directly to position sizing: larger positions will naturally experience larger absolute funding debits or credits.

Another element is understanding when the market appears crowded in one direction. Extended positive funding often reflects a market heavily skewed toward long positions, while extended negative funding indicates more aggressive short positioning. These conditions can intensify funding costs for the majority side, particularly if the imbalance persists.

Rather than focusing on specific tactics, the key is to recognize that funding, volatility, leverage, and liquidation risk are tightly linked. Awareness of how these factors interact helps traders evaluate whether their exposure and holding period align with their tolerance for funding‑related costs and market swings.

Perpetual Futures Trading on a Licensed Platform

OSL Group (HKEX: 863) is Asia’s leading stablecoin trading and payment platform, providing licensed digital asset exchange services supported by a compliance‑driven derivatives infrastructure. Within this framework, OSL Global offers perpetual futures contracts on major digital assets, including BTC, ETH, BNB, and SOL, as part of its regulated digital asset trading environment.

These perpetual contracts operate under a structured risk and governance framework designed to support transparent, regulated derivatives trading. Funding rates, leverage parameters, and product specifications are defined within this licensed context so that participants can understand how perpetual pricing mechanisms—such as funding—interact with broader market and regulatory considerations. For detailed product information, traders can review the specific contract specifications and disclosures provided for each perpetual listing on the OSL Global platform.

Funding Rate FAQs

Do perpetual futures use funding rate payments?

Yes. Perpetual futures typically use funding rate payments as a core mechanism to keep the contract price close to the underlying spot market. At set intervals, funding is exchanged directly between longs and shorts, rather than paid to the exchange, based on whether the perpetual is trading at a premium or discount to spot.

How are funding rates calculated?

Funding rates are usually calculated from two conceptual components: an interest rate component and a premium index that measures how far the perpetual price is from spot over a given period. Platforms combine these elements in their own formulas and apply the resulting rate at regular funding intervals, debiting or crediting each open position according to its notional size and direction.

How to use funding rate in trading?

Funding rates are best viewed as a cost and risk variable rather than a signal. Traders can factor funding into their decision-making by considering how recurring payments may affect the cost of holding a position—especially when using leverage or holding across many funding intervals—and by recognizing that extreme or persistent funding often reflects one‑sided positioning in the market. This is information to incorporate into risk awareness, not a guarantee of future price direction.

Who pays the funding rate?

Who pays funding depends on whether the rate is positive or negative. When funding is positive, long positions pay funding to short positions; when funding is negative, short positions pay longs. The exchange facilitates the transfer, but the payments are effectively trader‑to‑trader, linked to the current funding rate and the notional size of each open position.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics