「Stablecoin & Payments Weekly Pulse」 Vol.12 :Stablecoin Yields Enter a "Zero-Sum Game" Phase

This issue's author: Eddie Xin, Chief Analyst, OSL Research Email: [email protected]

I. Weekly Stablecoin Payment Data

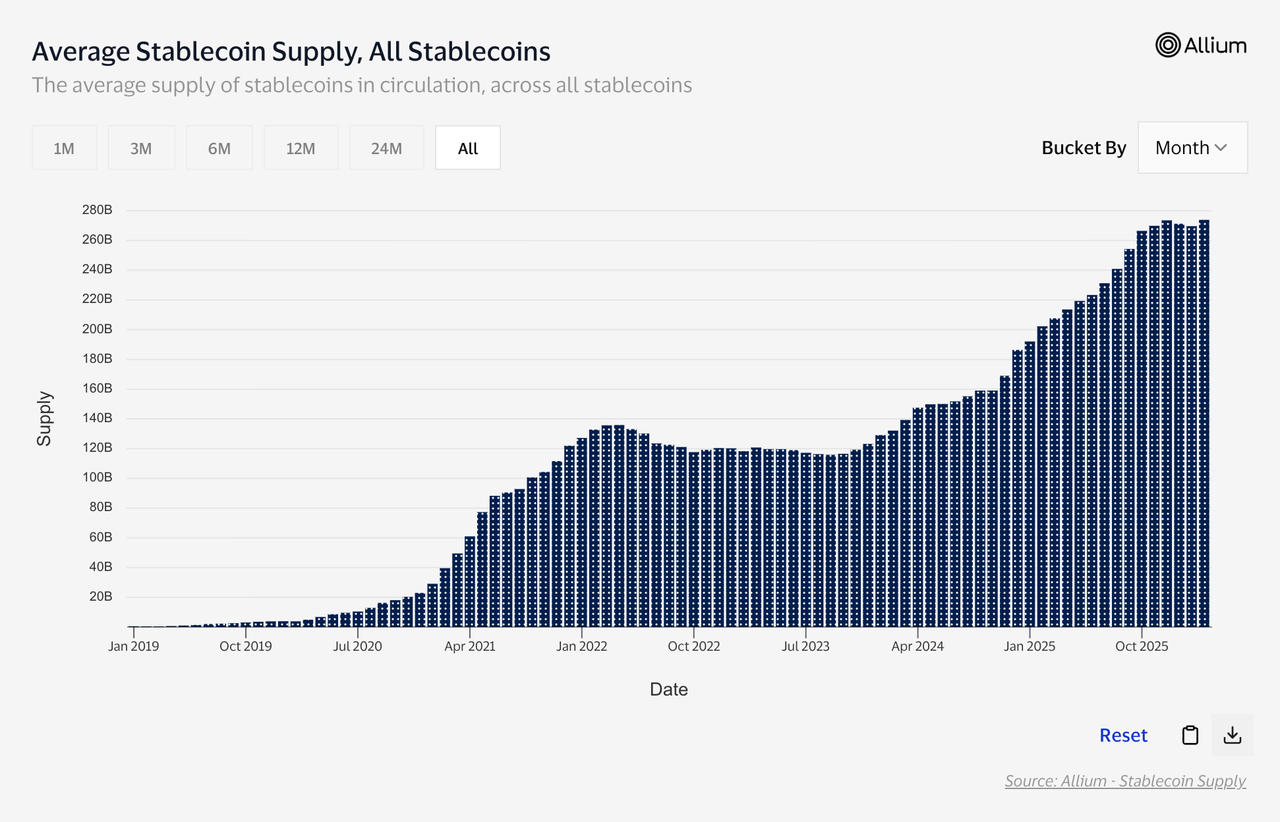

Omni-chain Data: As of 2026-03-20 (7-day rolling basis), the total market capitalization of all-chain stablecoins is approximately $315.97B; a net increase of +$1.64B (+0.52%) over the last 7 days; Ethereum accounts for approximately 52.63%.

RWA.xyz Data: Total stablecoin market cap is approximately $313.81B; monthly transfer volume reached $9.03T (data as of 03/19).

Messari Trends: Daily transfer volume fluctuated significantly over the last 30 days, peaking at $425.1B on 3/14 before retreating to a median range of around $346.7B.

OSL Research Adjusted Data: After filtering out market making, wash trading, and bot activity, the "effective" volume is approximately one-fifth of the total volume based on internal methodology.

(Source: Messari, Artemis, OSL Research)

(Excludes noise trading such as market making, wash trading, and bot activity)

Top 3 Stablecoins by Market Cap Growth (Messari 7D Gauge)

MetaMask USD (+7.8%)

Euro Tether (+6.5%)

Frax USD (+5.5%)

OSL Research Growth Observations

MetaMask USD (+7.8%)

The expansion of mUSD this week is primarily driven by its position as a native wallet entry point. As MetaMask's proprietary stablecoin, it benefits from inherent distribution efficiency within user paths for buying, swapping, bridging, and accessing DApps. The MetaMask Card rewards program further incentivizes users to maintain stable balances. On-chain, the Aave community's approval of mUSD listing parameters marks its transition from a mere "wallet balance" to a "composable asset," allowing supply growth to be absorbed by actual utility.

Euro Tether (+6.5%)

Growth in EUR₮ market cap should be interpreted as "residual volatility during liquidation" rather than business expansion. Tether officially ceased redemptions on 2025/11/27 and has long stopped new issuances. Major exchanges like Kraken have already finalized delistings. Current market cap "increases" are likely due to EUR/USD exchange rate fluctuations affecting USD-denominated valuations, combined with concentrated holdings during the wind-down phase. This should be classified as tail-asset management rather than a signal of renewed demand for Euro stablecoins.

Frax USD (+5.5%)

Growth in Frax USD stems from product line migration and infrastructure spillover. As the legacy FRAX Dollar migrates toward frxUSD—which emphasizes redeemability and compliance-ready structures—market observations include significant internal conversion. Simultaneously, ecosystems like Sonic Labs are utilizing frxUSD infrastructure for their native stablecoins, enhancing Frax's visibility as a base-layer component. In a high-interest-rate environment, these auditable and redeemable on-chain USD positions are increasingly attractive to institutional players.

II. Global Financial Institution Dynamics

1. Hana Financial × Standard Chartered: Stablecoin Collaboration Integrated into Banking-Grade MOU (03/13)

Description: South Korean media reported that Hana Financial Group and Standard Chartered signed a Memorandum of Understanding (MOU) in Seoul, covering global business and digital asset initiatives. Photos show the signing took place on March 13, 2026.

Sources: Korea JoongAng Daily (Mar 15, 2026); FinanceFeeds (Mar 16, 2026).

Observation: The inclusion of stablecoins in a formal banking agenda stems from a pragmatic assessment: cross-border and FX operations require a new "settlement toolbox." From a macro perspective, higher regulatory certainty drives deeper bank participation; as participation increases, stablecoins evolve from "trading tools" to core "settlement instruments."

2. PayPal Expands PYUSD Payment Services to 70 Markets (03/17)

Description: PayPal announced the expansion of PYUSD within its account ecosystem to 70 markets. Users can buy, hold, send, and receive PYUSD, with options to transfer to third-party wallets or convert to fiat. The announcement emphasized availability for "global consumers and merchants."

Source: PayPal Newsroom (Mar 17, 2026).

Observation: The expansion of PYUSD functions as an "account network extension," with on-chain capabilities moving to the background. Barriers to stablecoin adoption are absorbed by PayPal’s existing KYC, risk control, and merchant infrastructure. The user experience mirrors a "new form of USD balance." The pivot for the payment industry is twofold: shortening cross-border transfer paths while maintaining fiat on/off-ramps within PayPal’s compliant framework.

3. Thunes Integrates Swift Network: Direct Bank Connectivity to Stablecoin Wallets (03/17)

Description: Thunes announced its "Pay-to-Stablecoin-Wallets" solution, now accessible to banks via existing Swift connections. This covers approximately 11,500 financial institutions within the Swift network, supporting instant payments to stablecoin wallets. Official statements support USDC and USDT, emphasizing "no additional technical integration required."

Source: Thunes Newsroom (Mar 17, 2026).

Observation: This turns "stablecoin wallets" into addressable endpoints within the banking system. The bottleneck of cross-border payments is shifting from technical access to compliance parameters and risk thresholds. The competitive edge of stablecoins will upgrade from "on-chain speed" to "bank-side speed," as infrastructure competition permeates the banking sector.

4. Mastercard to Acquire Stablecoin Infrastructure Provider BVNK for $1.8B (03/17)

Description: Mastercard announced an agreement to acquire BVNK for up to $1.8 billion (including $300 million in contingent payments), with completion expected by late 2026. BVNK provides enterprise-grade infrastructure for fiat-stablecoin interoperability across 130+ countries.

Sources: Mastercard Investor News (Mar 17, 2026); Reuters (Mar 17, 2026).

Observation: Card networks are using M&A speed to bridge the gap in stablecoin infrastructure, signaling that "on-chain value flow" is now a long-term strategic priority. As regulations clear and enterprise adoption grows, traditional networks refuse to miss this technical dividend. Post-acquisition, the market will enter a "standardized access" phase, lowering enterprise barriers and accelerating scalability.

5. Theo Discloses Progress on Gold-Backed thUSD; Genesis Vault Reaches $100M (03/18)

Description: Multiple reports indicate that Theo's thUSD progress is tied to a $100M Genesis Vault. The product is described as a "gold-driven yield-bearing stablecoin," with a narrative centered on combining tokenized gold with hedging strategies to achieve stable returns.

Sources: FinanceFeeds (Past 24h); Cointelegraph/TradingView (Past 48h).

Observation: "Yield-bearing stablecoins" are expanding from T-bill rate anchors to commodity derivative anchors. The product profile aligns more with institutional cash management than high-frequency payment media. Critical evaluation points lie in transparency and resolution paths: reserve auditability, risk boundaries for hedging exposure, and redemption arrangements under extreme market conditions. Inflow does not equate to sustainability; the cadence of disclosure will dictate the product's lifecycle.

III. Weekly Regulatory and Policy Signals

1. Hong Kong Stablecoin Licenses: Note-Issuing Banks Expected in First Batch (03/13)

Description: Bloomberg reported that HSBC and Standard Chartered are expected to be included in the first batch of Hong Kong’s stablecoin issuer licenses. Regulators favor institutions within the existing note-issuing bank system, signaling a "institutions first, expansion later" regulatory pace.

Source: Bloomberg (Mar 13, 2026).

Observation: Hong Kong’s focus is on integrating stablecoins into an auditable financial order. License scarcity will inflate channel value, making distribution and redemption capabilities the primary axis of license valuation. Centralization of compliant entities will accelerate, with controlled scenarios like cross-border payments and RWA settlement achieving scale first.

2. Brazilian Industry Groups Oppose Extending Financial Transaction Tax (IOF) to Stablecoins (03/14)

Description: CoinDesk reported that several Brazilian crypto and fintech industry organizations oppose extending the IOF (tax on financial transactions) to stablecoin operations, arguing it conflicts with current legal frameworks and stifles compliance and innovation.

Source: CoinDesk (Mar 14, 2026).

Observation: If tax authorities classify stablecoins under "foreign exchange" regulation, compliance costs will be front-loaded: reporting, audit trails, corridor compliance, and fund classification. Cross-border payment providers must pre-integrate tax and reporting interfaces to avoid retroactive "patch-style" modifications.

3. EU MiCA Continues to Limit Yield Attributes of Stablecoins (03/13—03/19)

Description: Academic and compliance interpretations in March continue to highlight MiCA’s stance: stablecoins are discouraged from acting as "savings tools." Strict constraints remain on "yield or benefits linked to holding time" during issuance and distribution.

Source: Oxford Business Law Blog.

Observation: Europe is drawing a line: stablecoins should be "payment media," not "wealth management products." Macroscopically, this protects bank liability sides and money market stability. The industry’s focus will shift toward payment experience, settlement finality, and enterprise risk management, moving growth from "yield incentives" to "service capability."

IV. Analyst Commentary: Stablecoin Wealth Management Enters the "Capital Retention" Phase—Post-Subsidy War, What is the Market Fighting For?

Eddie Xin, Chief Analyst at OSL Research

Email: [email protected]

As we reach the end of Q1, the most compelling aspect of the stablecoin market is not the market cap fluctuations of individual tokens, but the reallocation of "USD balances" across various platforms.

The competition has transcended simple token listings, market making, or volume driving. It now revolves around a more substantial core: who can retain users' stablecoins within their ecosystem longer, at a larger scale, and ensure this capital continues to participate in trading, collateralization, payments, and settlements. Data from RWA.xyz shows that as of March 19, the total stablecoin market cap has surpassed $300 billion, with monthly transfer volumes reaching approximately $9.35 trillion.

Simultaneously, on-chain T-bills and money market fund (MMF) products have scaled to roughly $10 billion. These figures paint a clear picture: stablecoins are no longer just payment tools; they are rapidly evolving into "on-chain USD accounts" and "on-chain cash management tools."

If I were to summarize this current phase in one term, I would call it the "Deposit-ization" Competition of Stablecoins.

The strategy of "burning subsidies to grab capital retention" is essentially a mirror of "deposit migration" in traditional finance. Platforms attract capital with high APRs, then integrate that liquidity into high-frequency scenarios like trading, financing, margins, and payments.

The ultimate profit is not found in superficial transaction fees, but in deeper liquidity pools, interest rate spreads, and client relationships. This trend strengthened over the past week: exchanges are turning stablecoin management into "instant-access" balance accounts, while institutions are packaging T-bills and MMFs into on-chain yield-bearing USD instruments. The market is no longer asking "whose stablecoin is more stable," but rather "who can turn USD balances into productive assets retained within the system."

Let’s look at exchange-side product strategies. Coinbase currently offers 3.35% rewards on USDC for eligible holders. Kraken's rewards are even more direct, showing up to 4.25% APR on USDG for Kraken+ users and 3.75% on USDC, emphasizing no lock-ups and instant trade/withdraw availability. Binance’s approach is representative: its USDT Simple Earn page offers a 3.84% principal-protected yield, while its "reward-bearing" asset, BFUSD, allows users to earn yields while using the asset as margin in futures accounts with a 99.9% CVR.

OKX’s Simple Earn Flexible explicitly states that yields come from lending assets to Flexible Loan and margin trading users. Bybit’s BYUSDT goes further by making Flexible Easy Earn USDT shares usable as collateral within a Unified Trading Account. On the surface, it looks like wealth management; in substance, top platforms are re-engineering stablecoin balances into account-level tools that are yield-bearing, tradable, and collateralizable.

This is why I believe the market has reached the "mid-stage of the subsidy war" and is shifting toward a "capital efficiency war."

While high APRs will persist, they will increasingly function as customer acquisition costs (CAC) rather than long-term equilibrium rates. The truly sustainable yield anchors remain short-term T-bills and USD interest rates. OKX’s bonus APRs have quotas; Bybit’s high yields depend on events and tiers; whereas Coinbase and Kraken’s standard yields are noticeably closer to sustainable levels.

In other words, subsidies are not the endgame; they are a means to keep capital in place. The ultimate winner will be the platform whose retained capital generates the most trading depth, financing demand, and payment stickiness.

On the institutional side, a crucial narrative is emerging: yield-bearing USD instruments are replacing idle stablecoins as the new foundation for institutional cash management and collateral. Circle’s USYC is no longer just a "product that earns interest"; it is defined as a tokenized money market fund, supporting near-real-time redemption into USDC and serving as yield-bearing margin or cross-margin collateral. Ondo’s OUSG/rOUSG is equally typical: its website shows an APY of ~3.44% with 24/7 redemptions and instant mint/redeem for as little as $5,000, with management fees of 0.15% waived until July 2026.

Franklin Templeton’s Benji/FOBXX had total assets of ~$864 million by late February, with a 7-day effective yield of 3.58% in early March, and launched an institutional off-exchange collateral solution with Binance on Feb 11. Superstate’s USTB is also transforming short-duration T-bill funds into on-chain cash management positions. Notably, CoinDesk reported on March 13 that Circle’s USYC has reached ~$2.2 billion in scale, surpassing BlackRock’s BUIDL. This indicates that institutional capital is "voting with its feet": they don’t want "high-interest stablecoins"; they want yield-bearing, redeemable, settleable, and collateralizable on-chain USD positions.

Synthesizing these two lines, the stablecoin wealth management market is now split into three types of players. The first is Exchange Subsidy-driven, targeting retail and trading USD balances. The second is Institutional Cash Management, aiming to make on-chain T-bills and MMFs the default institutional "parking spot" for USD. The third is Compliant Infrastructure, which doesn’t just sell yield but operates the entire chain of stablecoin issuance, conversion, payment, trading, and settlement.

OSL fits best into this third category. On Feb 10, OSL officially launched USDGO, a compliant USD stablecoin positioned for institutional settlement and corporate payments. On Feb 25, OSL HK listed USDGO/USD, USDGO/USDT, and USDGO/USDC trading pairs.

StableHub, launched in early February, focuses on 1:1, zero-slippage, zero-fee conversion between stablecoins and USD, featuring events like up to 18% APY on RLUSD and capped 100% annualized yields for USDGO. Combined with the early-year acquisition of Banxa, OSL’s direction is clear: it participates in "capital retention," but its true goal is a stablecoin network that lands on trading, payments, and compliant on/off-ramps.

Therefore, the core change I’ve observed over the past week isn't a platform raising its APY by a few points, but a shift in the industry's competitive gravity. The previous stage was about the magnitude of subsidies and events; this stage is about whose stablecoin balance can earn yield, trade, and act as collateral simultaneously. The next stage will be about who can truly embed stablecoins into corporate payments, institutional settlement, cross-border flows, and ALM (Asset and Liability Management). At that point, yield will move from a lead role to a supporting one, while compliance, liquidity, collateral efficiency, and scenario coverage will become the long-term deciders.

Over the next 6 to 12 months, I foresee three clear trends:

High subsidies will continue but will converge into quota-limited events, VIP tiers, and new user incentives, rather than serving as a long-term interest rate benchmark.

The integration of yield assets and trading accounts will accelerate, with structures like BFUSD, BYUSDT, and USYC-as-collateral becoming commonplace.

Regulators will manage "payment stablecoins" and "yield-bearing USD tools" separately. The US OCC’s GENIUS Act implementation rules (drafted in March) reiterated that payment stablecoin issuers must not pay interest or yield solely for holding or using the coin. Reuters also reported that the US banking industry opposes yield-bearing stablecoin products due to potential deposit diversion. This means future yields will shift more toward exchange rewards, on-chain MMFs, and tokenized institutional cash management products.

The stablecoin market has evolved from a "payment tool competition" to a "USD balance competition." Wealth management is merely the surface; the real battle is for capital retention, collateral capability, and future payment gateways. Whoever can transform stablecoins from static chips into yield-bearing, circulating, settleable, and regulatable USD infrastructure will be the winner of the next phase.

Disclaimer and Disclosure

1. Nature of Document

This document (“Document”) has been prepared solely by internal personnel of OSL for informational purposes. It does not constitute investment, legal, tax, or other professional advice and should not be relied upon as such. No part of this Document may be reproduced, distributed, or transmitted to any third party in any form without the prior written consent of OSL.

This Document does not constitute an offer, solicitation, marketing material, product disclosure, or legal document, nor does it form the basis of any binding contract or commitment. It is intended solely to provide OSL’s observations and strategic insights on the industry and does not represent OSL’s official opinions, strategies, or decisions.

The authors are not independent research analysts, and this Document does not constitute “investment research” as defined under applicable laws and regulations. Accordingly, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any pre-dissemination trading restrictions.

2. Non-Reliance

The information, opinions, and analyses contained herein are based on publicly available information and OSL’s internal judgment. They do not take into account the individual objectives, financial circumstances, or needs of any recipient. This Document is not a personal recommendation or solicitation to buy, sell, or otherwise transact in any financial instrument, product, or service.

Before making any investment or other decision, recipients must consult their own independent advisors, considering their individual circumstances, objectives, experience, and resources. All investments involve risk; values may fluctuate, and investors may receive less than the original invested amount. Past performance is not indicative of future results.

3. Accuracy, Completeness, and Limitation of Information

This Document is based on information that OSL considers reliable; however, OSL has not independently verified its accuracy, completeness, or fairness. Reasonable care has been taken to ensure that the content is not false or misleading, but OSL makes no representation or warranty, express or implied, regarding its accuracy, completeness, fairness, or reasonableness.

OSL is not responsible for any errors, omissions, or consequences arising from reliance on third-party information referenced herein. Performance of any discussed instruments, entities, or strategies may be materially affected by market, regulatory, technical, or other factors.

4. Forward-Looking Statements

This Document may contain forward-looking statements that involve known and unknown risks, uncertainties, and other factors. Actual results, performance, or achievements may differ materially from those expressed or implied. OSL does not undertake any obligation to update, revise, or withdraw any forward-looking statements.

5. Conflicts of Interest

OSL, its affiliates, and employees may hold positions in, or engage in transactions involving, the assets or entities discussed herein. The authors or other personnel involved in the preparation of this Document may receive compensation that is linked to the performance of OSL’s business. OSL has implemented policies and procedures to identify and manage potential conflicts of interest.

6. Intellectual Property and Restrictions on Use

This Document is protected by copyright and is intended solely for the designated recipient. Recipients may store, display, analyze, modify, reformat, and print this Document for their own internal use only. Recipients may not, without OSL’s prior written consent:

Resell, redistribute, or commercially exploit this Document;

Reverse engineer, extract, or create derivative works, including for training or use in machine learning/artificial intelligence systems;

Publish or transmit this Document to third parties

7. Limitation of Liability

To the maximum extent permitted by applicable law, OSL, its affiliates, officers, employees, and agents shall not be liable for any direct, indirect, incidental, consequential, or special damages arising from or in connection with the use of, reliance upon, or interpretation of this Document, including but not limited to:

Loss of profits;

Business interruption;

Data loss;

Reputational harm.

8. Global Distribution Notes

Recipients are responsible for compliance with local laws. Distribution of this Document may be restricted in certain jurisdictions. Recipients must ensure that it is not distributed to any person or entity to whom such distribution would be unlawful.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics