「Stablecoin & Payments Weekly Pulse」 Vol.9:The Euro Stablecoin Landscape Under MiCA

Master the key global changes in "Traditional Payments + Digital Asset Payments" for the week in just 10 minutes, providing reference information and professional observations for industry participants.

Author: Kelly Wang, Research Intern at OSL

Email: [email protected]

I. Weekly Stablecoin Payment Data

As of February 12, 2026 (7-day rolling basis), the total market capitalization/supply of stablecoins stands at approximately $308.6 billion, maintaining a plateau around the $300 billion mark.

Messari observations indicate sustained activity in stablecoin transfers. The cumulative transfer volume over the last 30 days exceeded $9.68 trillion, fluctuating daily between approximately $296 billion and $300 billion. Based on a rough extrapolation of daily averages, the total transfer volume for the last 7 days remains in the $1.8 trillion – $2 trillionrange.

From a structural perspective that filters out long-term noise, OSL Research estimates the "effective" volume (excluding market making, self-trading, bots, etc.) to be approximately one-fifth of the total, corresponding to a range of $360 billion – $400 billion for the last 7 days.

(A decrease in the supply of stablecoins can indicate a market downturn.)

(Data source: Messari, Artemis, OSL Research)

Top 3 Stablecoins (Protocols) by Market Cap Growth this Week:

1. Monerium EUR emoney (+10.00%; Weekly Transfer Volume: $66.09M, -39.05%)

2. PayPal USD (PYUSD) (+9.06%; Weekly Transfer Volume: $9.77B, +37.19%)

3. EURC (+5.84%; Weekly Transfer Volume: $2.43B, -3.98%)

OSL Research Growth Observations:

1.Monerium EUR emoney:

Its weekly expansion is driven by institutional capital sedimentation. Issued under a compliant Electronic Money Institution (EMI) model, it is pegged 1:1 to the Euro in bank accounts. The 10% market cap growth over the past week primarily stems from large inflows from institutional clients rather than retail trading. The 39.05% drop in weekly transfer volume (to $66.09M) indicates reduced trading activity, diverging from market cap growth. This suggests capital is being "held for settlement" or treasury management purposes, rather than providing liquidity in DeFi protocols.

2. PayPal USD (PYUSD):

Issued by Paxos under a full reserve model (US Dollar deposits, short-term US Treasuries, and cash equivalents), supporting Ethereum, Solana, and Arbitrum. TVL grew from $3.56 billion to $3.88 billion (+9.0%) over the past week, aligning with its 9.06% market cap growth. The significant 37.19% surge in weekly transfer volume (to $9.77B) indicates high capital activity. The fund flow characteristics suggest "circulating turnover," likely driven by a dual engine: payment scenarios within the PayPal e-commerce ecosystem and large-value institutional transfers for corporate treasury management and cross-border payments.

3. EURC:

Issued by Circle, adopting a full reserve model similar to USDC, pegged 1:1 to the Euro. While Circle's overall TVL grew from $71.68 billion to $74.12 billion (+3.4%) last week, EURC specifically outperformed with a 5.84% growth rate. Holder data shows significant shares in Circle's official hot wallets and active institutional addresses like Coinbase. Capital usage reflects "institutional allocation," likely due to European investors seeking Euro assets for hedging amidst a strong US Dollar, alongside the effectiveness of Circle's recent expansion strategy in the European market.

II. Weekly Stablecoin Payments & Infrastructure Highlights

1. OSL Launches USDGO: Asian Compliant Institutional Stablecoin Seizes Cross-Border Settlement Lane

News: OSL Group has launched USDGO, an enterprise-grade compliant US Dollar stablecoin positioned for institutional settlement and corporate cross-border payment scenarios. The initial $50 million USDGO has been minted and deployed on the Solana public blockchain. Simultaneously, OSL initiated the GO Alliance stablecoin ecosystem, committing $20 million in ecosystem incentives for initial partners to drive USDGO adoption in corporate settlement and cross-border payments. USDGO is pegged 1:1 to the USD, issued by Anchorage Digital Bank N.A. with third-party audits, while OSL handles brand operations and distribution.

Source: Bloomberg (2026/02/10)

Observation: USDGO leverages a US federally chartered bank for issuance and third-party audits, binding with Solana to achieve institutional-grade efficiency. It precisely targets the rigid demand for Asian corporate cross-border payments with a dual barrier of compliance + efficiency. By rapidly expanding scenarios through the ecosystem alliance and $20 million incentives, OSL is essentially positioning the stablecoin as institutional settlement infrastructure rather than a mere medium of exchange. This move reinforces Hong Kong's status as an Asian hub for compliant stablecoins, directly benchmarking against Western centralized stablecoins to vie for dominance in on-chain settlement of institutional cross-border funds.

2. SBI Partners with Startale for Strium Network: Japan Seizes Discourse Power in Asian On-Chain Securities & RWA Infrastructure

News: Japanese financial giant SBI Holdings announced a partnership with Startale Group to launch a Proof of Concept (PoC) for Strium Network, a Layer 1 blockchain for tokenized stocks. Strium is positioned as the "foundational trading layer for the Asian on-chain securities market," featuring 24/7 trading, rapid cross-border settlement, and DeFi composability. The parties previously announced collaborations on a JPY stablecoin and an RWA trading platform, with a testnet launch planned soon. Startale is a core developer for Sony's L2 project Soneium and operates the Japanese public chain Astar Network.

Source: The Block (2026/02/05)

Observation: Japanese financial capital is deeply integrating with local blockchain infrastructure forces. Leveraging SBI's traditional financial compliance advantages and Startale's foundational R&D capabilities (backed by Sony L2 technology and Astar operations), this move connects their previous layouts in JPY stablecoins and RWA platforms. It targets efficiency pain points in traditional securities markets and cross-border settlement needs, attempting to form a differentiated barrier in the global on-chain securities competition based on a local ecosystem, while building the underlying infrastructure for the compliant development of Japan's crypto finance.

3. Tether Acquires Stake in Gold.com: Bridging On-Chain and Off-Chain Assets with Compliant Stablecoin + Gold Tokens

News: Tether's investment arm has acquired an approximate 12% stake in the precious metals platform Gold.com for $150 million and will integrate its gold stablecoin XAUt into the platform. Both parties are also exploring support for users to purchase physical gold using USDT and the US-market-oriented USAt, which was launched on January 27 in partnership with Anchorage Digital.

Source: Cointelegraph (2026/02/06)

Observation: By taking a stake in a gold platform and opening channels between gold stablecoins and physical gold, Tether is further building a commodity-backed stablecoin ecosystem and strengthening its discourse power in on-chain value storage. This provides compliant scenarios and real asset backing for USDT and USAt, while using gold assets to reduce market doubts about its reserve transparency and enhance long-term resilience.

4. Vitalik Redefines Algorithmic Stablecoin Paradigm: ETH-Collateral First, Moving Towards Decentralized Diversified Stable Units

News: Vitalik Buterin stated that algorithmic stablecoins should be viewed as true DeFi. If a high-quality ETH-collateralized algorithmic stablecoin exists, even if 99% of liquidity comes from CDP holders (holding negative algorithmic USD positions while holding positive USD positions elsewhere), users can still transfer USD counterparty risk to market makers, which is a key feature. Even if partially backed by RWAs, as long as the system remains over-collateralized and highly decentralized (where the failure of any single underlying asset does not affect overall collateral), it can substantially improve the risk structure for holders. He believes priority should be given to ETH-collateralized algorithmic stablecoins, followed by highly decentralized, over-collateralized RWA models, gradually shifting from "USD-denominated units" to broader diversified indices.

Source: Odaily (2026/02/09)

Observation: Vitalik's redefinition provides theoretical endorsement for ETH-centric decentralized stable models, positioning over-collateralization and risk diversification as core compliance and safety boundaries. This directly responds to long-term market skepticism about pure algorithmic models. His path—prioritizing ETH collateral before transitioning to decentralized RWAs—anchors the underlying value of the Ethereum ecosystem while attempting to build non-sovereign stable units beyond USD valuation, hinting at a long-term vision for DeFi de-fiatization.

5. Fosun FinChain Launches FUSD: Asian Institutions Land on Interest-Bearing RWA Stablecoins

News: FinChain, the blockchain finance platform under Fosun Wealth Holdings, launched the interest-bearing RWA stablecoin FUSD on Avalanche. Backed by compliant real-world assets including money market funds and government bonds, it targets Asian institutional capital, offering both native yield and on-chain liquidity. FUSD utilizes Avalanche C-Chain as its primary liquidity and DeFi integration hub, serving institutional investors such as family offices, private equity funds, and pension funds.

Source: Sina Finance (2026/02/09)

Observation: FUSD uses compliant money market instruments and government bonds as underlying reserves, overlaying native on-chain yield and instant liquidity. It precisely matches the core needs of Asian family offices and pension funds for low volatility + deterministic yield + on-chain efficiency. Leveraging Avalanche's institutional-grade infrastructure for DeFi integration, it essentially represents a compliant bridge between traditional wealth management and on-chain finance, filling the supply gap for yield-bearing stablecoins tailored for Asian institutions outside of USD stablecoins.

6. ZARU Stablecoin Goes Live: South African Local Rand-Pegged Stablecoin Enters Cross-Border Settlement Race

News: South African finance and technology companies have jointly launched the ZARU stablecoin. Pegged to the South African Rand and issued on Solana, it aims to provide 24/7 instant settlement for retail and institutional users, eliminating the delays and high costs associated with traditional banking, cross-border trade, and remittances.

Source: Bitcoin.com (2026/02/05)

Observation: The launch of ZARU represents a key move by local South African financial and tech capital to reconstruct local currency payment infrastructure and reclaim regional settlement pricing power, challenging the long-term dominance of USD stablecoins in African cross-border settlement. Its 24/7 instant settlement capability not only targets the inefficiencies of traditional banking but also directly cuts into rigid demand scenarios for African cross-border trade and remittances, rapidly forming a dual advantage of local compliance and on-chain efficiency during a period of regulatory ambiguity.

7. African Stablecoin Exchange Spreads Highest Globally; Liquidity and Competition Gaps Drive Up Actual Costs

News: Data from payment infrastructure company Borderless xyz shows Africa has the highest stablecoin-to-fiat exchange spreads globally. The median spread in Africa is approximately 3% (299 basis points), significantly higher than Latin America (~1.3%) and Asia (0.07%). South Africa's exchange cost is around 1.5%, while Botswana sees highs near 19.5%. The report notes spreads are mainly determined by local liquidity and service provider competition: markets with multiple providers see costs of 1.5%–4%, while single-provider markets often exceed 13%. Despite stablecoins being viewed as tools to lower cross-border costs, actual exchange costs remain prohibitively high in some African corridors.

Source: Cointelegraph (2026/02/11)

Observation: With a median spread of 3% and local highs near 19.5%, data reveals that stablecoins in Africa are still rigidly constrained by weak fiat on/off-ramp infrastructure. Spreads are directly determined by local liquidity depth and the competitive landscape of service providers; monopoly markets seeing costs over 13% fully reflects that the inclusive value of stablecoins highly depends on the efficiency of offline fiat channels. This data breaks the narrative that stablecoins naturally lower cross-border costs, indicating the core contradiction in the African market has shifted from demand to compliant channels, competitive supply, and reserve efficiency—key observation points for institutional layout.

III. Weekly Regulatory & Policy Signals

1. Brazil: Criminalizing Regulation Reshapes Stablecoin Sovereign Boundaries via Bill 4308/2024

News: The Science and Technology Committee of Brazil's Congress passed Bill 4308/2024, moving to ban algorithmic stablecoins and explicitly prohibiting the issuance and trading of stablecoins without full reserve backing (including Ethena’s USDe and Frax). New rules require stablecoins issued in Brazil to be 100% backed by segregated reserve assets with increased transparency; unauthorized issuance of unsecured stablecoins will be classified as a criminal offense punishable by up to 8 years in prison. For foreign stablecoins (e.g., USDT, USDC), only approved institutions may offer them, and exchanges must verify issuer compliance with national standards or bear the risk. Stablecoins currently account for ~90% of Brazil's crypto volume.

Source: CoinDesk (2026/2/5)

Observation: Brazil's comprehensive ban on algorithmic and under-collateralized stablecoins, reinforced by criminal liability for the 100% segregated reserve requirement and strict entry for foreign stablecoins, will directly reshape a crypto trading market where stablecoins dominate over 90% of volume. Essentially, this uses strong regulation to maintain financial sovereignty and squeeze the survival space of decentralized stablecoins.

2. China: Eight Departments Define Total Ban on Crypto & RWA Tokenization; Only Licensed Stablecoins Allowed

News: The People's Bank of China, in conjunction with multiple departments, issued a notice to further prevent and dispose of risks related to virtual currencies and Real World Asset (RWA) tokenization. Virtual currencies lack legal tender status; related trading, exchange, issuance financing, and intermediary services are strictly prohibited as illegal financial activities. Issuance of RMB-pegged stablecoins without approval is forbidden. RWA tokenization within China is also deemed suspected illegal financial activity and is prohibited in principle, limited only to cases legally approved and relying on specific financial infrastructure. The crackdown on "mining" continues, along with severe punishment for fraud, money laundering, and illegal fundraising, alongside strict regulation of domestic entities conducting related business overseas.

Source: Xinhua Net (2026/02/06)

Observation: This regulation imposes a total ban on virtual currency and domestic RWA tokenization activities, strictly restricts RMB stablecoin issuance, and strengthens control over cross-border businesses, establishing a financial security baseline with a high-pressure stance across the entire chain. The policy adopts a prudent attitude of "prohibited in principle, exceptions by special permission," completely blocking non-compliant channels connecting crypto assets with the local financial system. The coordinated domestic and international crackdown signals that crypto and on-chain asset innovation remains under strict control with no gray area for operation.

IV. Analyst Commentary: The Euro Stablecoin Landscape Under MiCA

Observer: OSL Research

Analyst: Kelly Wang (Intern)

Email: [email protected]

Advisor: Eddie Xin

The global stablecoin market has entered a mature development phase. As of February 2026, the total market capitalization of stablecoins has exceeded $3 trillion, with USD stablecoins (primarily USDT and USDC) commanding over 99% of the market share, forming an absolute dominance. In contrast, Euro stablecoins have long been marginalized, constrained by the strong network effects of the USD, the efficiency of the Eurozone's traditional payment system (SEPA), and compliance uncertainties from a lack of early regulatory frameworks, limiting institutional willingness to enter.

In June 2024, the specific stablecoin provisions of MiCA (Markets in Crypto-Assets Regulation) officially came into effect, marking a pivotal turning point for the industry. This regulation established the world's strictest stablecoin compliance system, mandating requirements such as 1:1 full reserves, 60% of reserve assets held in Tier 1 banks, and regular third-party audits, significantly boosting market transparency and institutional confidence. Driven by this regulatory dividend, Euro stablecoin market capitalization grew from approximately €500 million to €650 million between 2025 and 2026, representing an annual growth rate of 30%, as the market entered a standardized start-up phase.

In early 2026, Euro stablecoins officially entered a critical window for transitioning from a niche market to an institutional-led one. Although the current total market cap is only €650 million—less than 0.5% of the global total—the industry's growth space has been fully opened, driven by Real World Asset (RWA) tokenization.

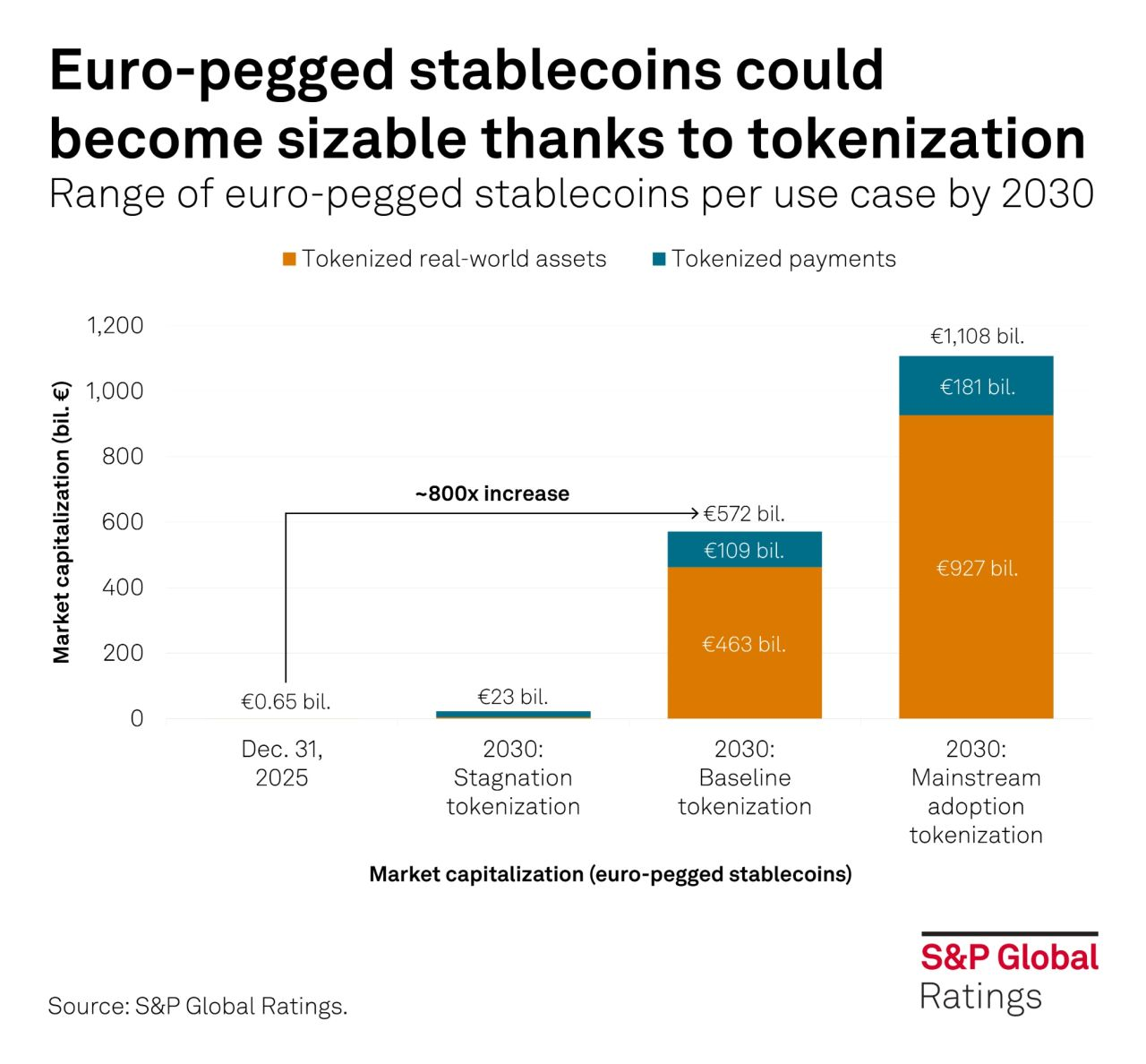

S&P Global forecasted in February 2026 that the Euro stablecoin market could reach between €25 billion and €1.1 trillion by 2030. The core growth driver will be institutional-grade asset settlement rather than retail payments.

Figure 1: Significant Growth of the Euro Stablecoin Market Over the Next 5 Years

Source: S&P Global Ratings

With MiCA fully implemented, Euro stablecoins are formally entering a bank-led era. The Qivalis consortium, comprising 11 major European banks (total assets over €4.5 trillion), plans to launch a compliant Euro stablecoin in H2 2026, with a projected first-year issuance exceeding €5 billion. This will significantly enhance market liquidity and institutional trust, reshaping the industry landscape.

Meanwhile, the Digital Euro, expected to launch in 2029, will further squeeze retail payment scenarios. However, the technical standards formed therein (e.g., offline payments, privacy protocols) can provide an interoperability foundation for private stablecoins, fostering a "competition + synergy" development pattern. Overall, while Euro stablecoins may struggle to challenge USD stablecoins in total scale, they are poised to establish distinct European characteristics and competitive advantages in the institutional RWA settlement sector, becoming a vital carrier of European digital financial sovereignty.

Against the backdrop of structural changes in the global stablecoin landscape and regulatory environment, the current market volume, structural characteristics, and development stage of Euro stablecoins have emerged with a clear outline. As of February 11, 2026, the Euro stablecoin market remains in early development with a small overall scale, but the growth trend driven by compliance implementation and institutional demand is clear.

Figure 2: Euro Stablecoin Market Cap, Share, and Comparison vs. USD Stablecoins

(Data Source: CoinGecko, DefiLlama)

Further observation of on-chain characteristics reveals the true state of the market regarding application scenarios, user structure, and liquidity:

Chain Distribution: Ethereum and Base combined account for ~60%, primarily handling DeFi and institutional settlement needs; Solana, Avalanche, and Stellar account for 40%, focusing on high-efficiency cross-border transfer scenarios.

Transaction Structure: Full-year 2025 on-chain transaction volume exceeded €8 billion, highly concentrated in DeFi liquidity pools and RWA tokenization settlement protocols, with extremely low retail transaction share.

Holding Structure: Institutional addresses hold over 70%, with top 10 addresses concentrating >50% of holdings. Retail user participation is under 10%, showing typical institutional dominance.

Liquidity Level: Depth of core trading pair liquidity pools is only about 1/1000th of USD stablecoins. Market depth is thin, and large transactions are prone to significant slippage, constraining large-scale institutional participation.

Based on the data above, we can conclude that following the implementation of the MiCA regulations, the market capitalization of Euro stablecoins has achieved a stage of growth, with the compliance foundation and institutional recognition significantly strengthened.

However, viewing the overall development level, market scale, liquidity, and penetration rates remain in the early stages. There is still substantial room for improvement toward large-scale and normalized application, which also reserves vast potential for the subsequent entry of bank-backed stablecoins and the penetration of RWA scenarios.

Against this backdrop, the growth of Euro stablecoins mainly relies on the synergistic force of three core factors: the core traction of RWA tokenization, the compliance catalysis of MiCA regulation, and the continuous increase in institutional adoption demand. These factors jointly drive the market to break through development bottlenecks and achieve steady growth.

Core Engine: The Scaled Advancement of RWA Tokenization

The core value of Euro stablecoins lies in providing T+0 real-time settlement channels for Real World Assets (RWA) such as bonds, funds, and real estate. This solves the traditional pain points of long settlement cycles, high costs, and low transparency, while leveraging the DeFi ecosystem to achieve annualized staking yields of 5%-10%, significantly higher than traditional bank deposit rates in the Eurozone (<2%).

Typical cases include Societe Generale using EURCV to conduct institutional-grade bond tokenization settlement, and BlackRock adopting compliant stablecoins for subscription and redemption in its Eurozone RWA fund pilots. According to BCG predictions, the global RWA market scale will exceed $400 billion in 2026, with a potential penetration rate of 10%-20% in the Eurozone. In 2025, the share of Euro stablecoins in the RWA settlement field grew by approximately 200% year-on-year, showing strong demand momentum.

Key Catalyst: The Full Implementation of the MiCA Regulatory Framework

The implementation of MiCA regulations brings compliance dividends to the market while accelerating industry consolidation, driving the market toward standardization and institutionalization. On the positive side, it clarifies the legal status of stablecoins, requiring 1:1 full reserves, regular audits, etc., enhancing market transparency and institutional trust; the EMT licensing system also lowers the barrier for compliant issuance. On the negative side, average annual compliance costs of millions of Euros form entry barriers, leading to the exit of small non-compliant projects and increasing industry concentration.

A core variable is the Qivalis banking consortium (composed of 11 mainstream European banks with total assets exceeding €4.5 trillion), which plans to launch a MiCA-compliant stablecoin in the second half of 2026. With an initial issuance exceeding €5 billion in the first year, this will significantly enhance market liquidity and legitimacy, intensifying industry competition.

Demand Support: The Sustained Rise in Institutional Adoption

The demand for stablecoin adoption by Eurozone institutions continues to be released, stemming from three core drivers: First, cross-border settlement costs are reduced by 30%-50%, and settlement cycles are shortened from T+2 to real-time (Deutsche Bank pilot data); Second, under global exchange rate volatility, the demand for Eurozone enterprises to hedge against USD dependence is rising, with the proportion of stablecoins in cross-border trade settlement rising from 5% in 2025 to 10% in 2026;

Third, the superposition of compliance certainty and yield advantages continues to attract institutional capital inflows, supporting market scale growth.

Despite the significant growth potential of the Euro stablecoin market, it still faces multiple challenges such as squeezing by the Digital Euro, market monopoly, and liquidity risks. The European Parliament has passed legislation related to the Digital Euro with a high number of votes (voting result 429:109).

The Digital Euro project has now entered the technical preparation stage and is expected to be officially issued in 2029. As a Central Bank Digital Currency (CBDC), the Digital Euro possesses legal tender status. Its functions, such as offline payment and privacy protection, are highly adapted to retail payment scenarios. Once launched, there is a high probability that it will monopolize the Eurozone retail stablecoin market, forcing privately issued Euro stablecoins to transform toward niche fields such as institutional wholesale and RWA settlement.

However, the technical standardization process of the Digital Euro (such as interface specifications, privacy protocols, offline payment technologies, etc.) can also provide an interoperability foundation for private stablecoins. Both parties can cooperate in scenarios such as institutional settlement and cross-border payments, forming a "CBDC + Private Stablecoin" synergistic development pattern rather than complete opposition.

Against the industry background of deepening MiCA regulation and the advancing layout of the Digital Euro, Euro stablecoin market participants are presenting a diversified development trend. Different types of entities have formed differentiated development paths based on their own resource endowments.

Based on this, we select core participants from the banking sector and the private sector to systematically dismantle their development models, core advantages, and potential bottlenecks, providing practical references for the layout decisions of various market entities.

Qivalis: Bank Consortium Stablecoin (Upcoming)

Qivalis is a stablecoin project jointly initiated by 11 mainstream European banks. Core members include ING, UniCredit, KBC, Danske Bank, DekaBank, SEB, CaixaBank, Banca Sella, Raiffeisen Bank International, etc. It is regulated by the Dutch Central Bank and positioned as an institutional-grade wholesale settlement stablecoin. The project fully complies with MiCA regulatory requirements and is planned to be officially launched in the second half of 2026, with a target initial issuance scale exceeding €5 billion in the first year.

Its core advantage lies in relying on the capital strength and institutional networks of member banks, allowing it to rapidly dock with the settlement needs of Eurozone enterprises and financial institutions, significantly enhancing market liquidity and industry legitimacy; but at the same time, its positioning leans toward traditional financial institutions, and it may have deficiencies in technical innovation and DeFi ecosystem integration. Its impact on existing private stablecoins will mainly be concentrated in the field of institutional settlement.

Circle: EURC

EURC is issued by Circle and is currently the leading variety in the Euro stablecoin market, with a market capitalization share of approximately 65%. Its core advantages lie in: First, multi-chain deployment, covering mainstream blockchains such as Ethereum, Base, and Solana, adapting to different scenario needs; Second, perfect compliance, with monthly third-party reserve audits and institutional-grade custody support, complying with MiCA regulatory requirements; Third, high ecosystem integration, having connected to multiple global exchanges and DeFi protocols, with relatively sufficient liquidity. Its core bottleneck lies in the fact that its growth rate has slowed somewhat after the implementation of MiCA regulations. It mainly relies on exchange trading and DeFi ecosystem integration, and its layout in the field of institutional-grade wholesale settlement is relatively lagging. It faces direct competition from bank consortium stablecoins in the future.

Societe Generale:

EURCV EURCV is issued by Societe Generale and is positioned as a "specialized" institutional stablecoin. It mainly focuses on niche scenarios such as institutional private equity funds and bond tokenization settlement. Although its market capitalization scale is small (approximately €50-100 million), its transaction volume is relatively high, reflecting a development strategy of being "specialized rather than broad covering." Its core advantage lies in relying on the financial resources of the parent bank and deeply binding to institutional client needs, with strong guarantees in compliance and security; its deficiency lies in its narrower ecosystem coverage and relatively limited liquidity, making it difficult to form scale effects. Additionally, it has a strong dependence on parent bank resources, and its autonomous expansion capability needs improvement.

Looking ahead, with the continuous deepening and detailed implementation of the MiCA regulatory framework, compliance will become the core base color of industry development. The mass entry of bank-backed stablecoins will reshape the market competition landscape, promoting a qualitative improvement in market liquidity and institutional recognition.

Meanwhile, the continuous penetration of RWA scenarios will further release the core value of Euro stablecoins, driving their upgrade from "settlement tools" to "asset allocation carriers." At the same time, industry development must still be vigilant against potential risks such as scenario squeezing after the launch of the Digital Euro, innovation suppression caused by bank consortium monopolies, as well as insufficient liquidity and technical security.

Only through differentiated scenario layout, strengthening compliant operational capabilities, and deepening technical innovation and cross-entity synergy can the Euro stablecoin market achieve high-quality, sustainable development, gradually building a stablecoin ecosystem that matches European digital financial sovereignty and occupying an important seat in global digital asset competition.

Disclaimer and Disclosure

1. Nature of Document This document (the "Document") has been prepared by OSL internal personnel for informational purposes only and does not constitute investment, legal, tax, or any other professional advice, nor should it be relied upon as such. No part of this Document may be reproduced, distributed, or transmitted to any third party in any form without the prior written permission of OSL. This Document does not constitute an offer, solicitation, marketing material, product disclosure statement, or legal document, nor does it form the basis of any binding contract or commitment. This Document is intended solely to present OSL's observations and strategic insights into the industry and does not represent the official position, strategy, or decisions of OSL. The authors are not independent research analysts, and this Document does not constitute "investment research" as defined by applicable laws or regulations. Consequently, this Document has not been prepared in accordance with regulations designed to ensure the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

2. No Reliance The information, opinions, and analyses contained in this Document are based on public information and OSL's internal judgment, without regard to the personal objectives, financial situation, or needs of any recipient. This Document does not constitute a personal recommendation, nor does it constitute an invitation or solicitation to buy, sell, or engage in any financial instrument, product, or service. Recipients should consult their own independent advisors regarding their personal circumstances, objectives, experience, and financial resources before making any investment or other decision. All investments involve risk; values may fluctuate, and investors may recover less than the original investment amount. Past performance is not indicative of future results.

3. Accuracy, Completeness, and Limitations This Document has been prepared based on information OSL believes to be reliable, but OSL has not independently verified its accuracy, completeness, or fairness. Although reasonable care has been taken to ensure the content is not false or misleading, OSL makes no express or implied warranty as to the accuracy, completeness, fairness, or reasonableness of the content. OSL accepts no liability for any errors, omissions, or consequences of reliance caused by third-party information cited in the Document. The performance of any instruments, entities, or strategies mentioned may be significantly affected by market, regulatory, technical, or other factors.

4. Forward-Looking Statements This Document may contain forward-looking statements involving known and unknown risks, uncertainties, and other factors. Actual results, performance, or achievements may differ materially from those expressed or implied by such statements. OSL is under no obligation to update, revise, or withdraw any forward-looking statements.

5. Disclosure of Conflicts of Interest OSL, its affiliates, and employees may hold positions in or participate in transactions related to the assets or entities mentioned in this Document. The authors or related personnel may receive compensation related to OSL's business performance in this regard. OSL has implemented policies and procedures to identify and manage potential conflicts of interest.

6. Intellectual Property and Restrictions on Use This Document is protected by copyright and is for the internal use of the designated recipient only. Recipients may store, display, analyze, modify, reformat, and print this Document for internal purposes, but without OSL's prior written consent, may not:

Resell, redistribute, or use this Document commercially;

Reverse engineer, extract, or create derivative works, including for training or application in machine learning/artificial intelligence systems;

Publish or transmit this Document to third parties.

7. Limitation of Liability To the maximum extent permitted by applicable law, OSL and its affiliates, officers, employees, and agents shall not be liable for any direct, indirect, incidental, consequential, or special damages arising out of or in connection with the use, reliance, or interpretation of this Document, including but not limited to:

Loss of profits;

Business interruption;

Data corruption or loss;

Reputational damage.

8. Global Distribution Note Recipients should ensure compliance with applicable local laws. Distribution of this Document may be restricted in certain jurisdictions. Recipients must ensure this Document is not distributed to any person or entity prohibited by law from receiving it.

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics