Stablecoin Payments vs Traditional Banking Rails: A Practical Comparison for Enterprises

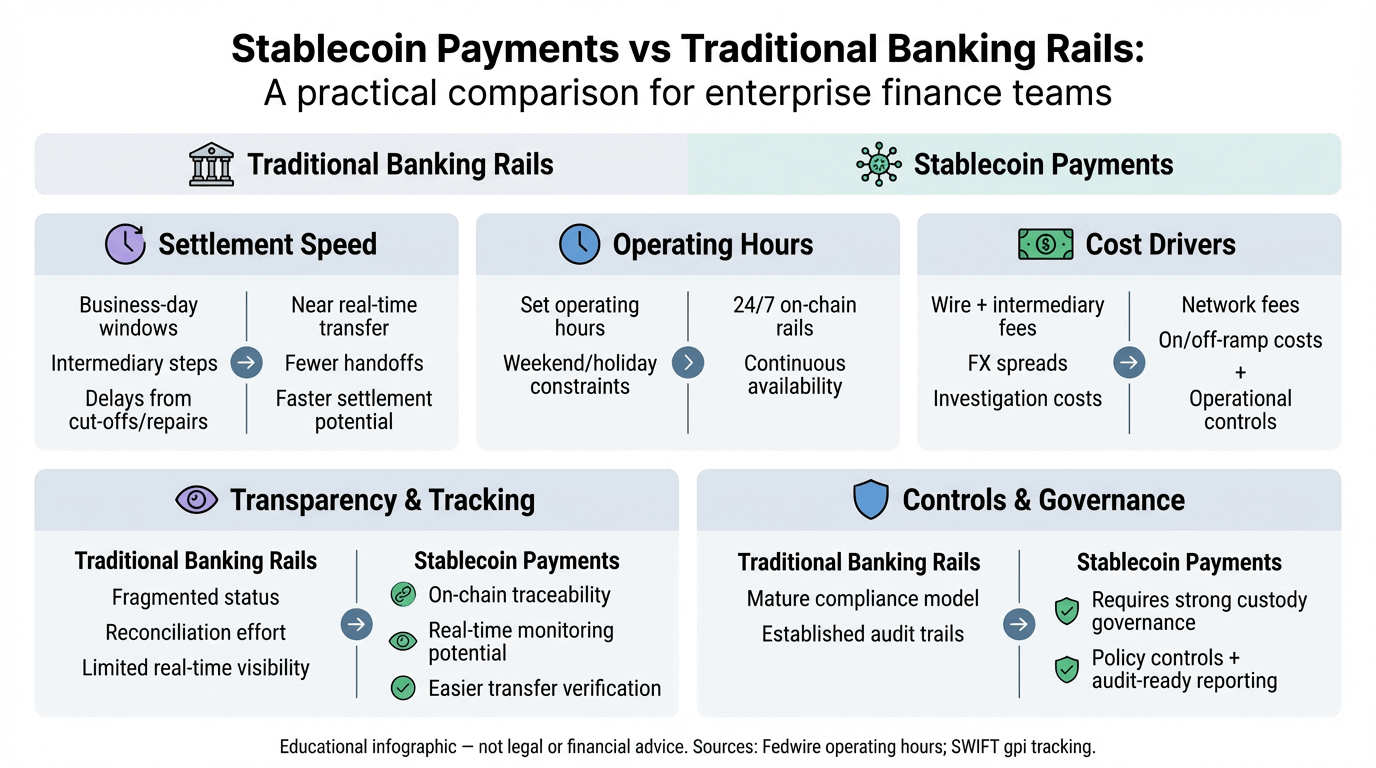

“Stablecoin payments vs traditional banking rails” is no longer a theoretical debate. For many finance teams, it has become a practical question about settlement speed, cost predictability, visibility, and controllability, especially for cross-border payments and multi-entity treasury operations. Traditional rails (correspondent banking, wires, and clearing systems) remain foundational, but they also reflect constraints such as cut-off times, operating hours, reconciliation complexity, and layered intermediary fees. Meanwhile, stablecoin-based settlement introduces a different operating model, often nearer to T+0 value transfer, but requires mature governance around custody, compliance, and operational controls.

In this article, we provide a neutral, enterprise-focused comparison to help CFOs, treasury teams, and compliance leaders decide where stablecoin settlement can complement banking rails, and where banking rails still dominate.

Traditional Banking Payment Rails

Traditional banking rails include domestic high-value systems (e.g., RTGS), cross-border correspondent banking (often via SWIFT messaging), and specialized clearing networks. They are proven, regulated, and deeply integrated into enterprise finance. However, they can introduce friction that becomes more visible at global scale.

Settlement Cycles and Delays

T+1/T+2 timelines

In capital markets, “T+1/T+2” refers to securities settlement cycles (trade date plus one or two business days). While this is not the same as payment settlement, it illustrates how system design, risk controls, and operational windows can shape when funds are truly final. The U.S. moved most securities transactions to T+1 on May 28, 2024, explicitly to reduce risk and improve market efficiency.

In payments, settlement timing depends on the rail:

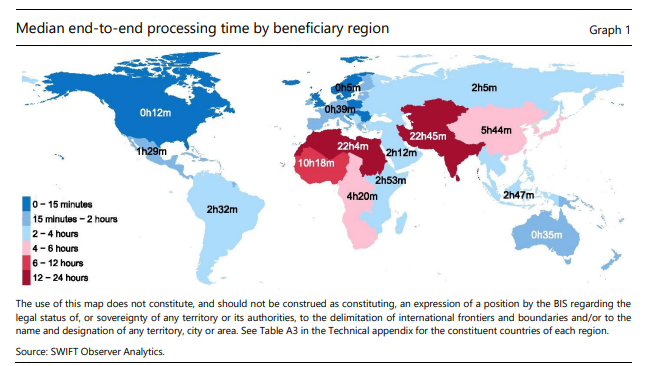

Fedwire Funds Service is a real-time gross settlement system, but it operates on business days with defined hours (not 24/7). The US Federal Reserve notes the business day runs from 9:00 p.m. ET to 7:00 p.m. ET, Monday–Friday, excluding holidays, with a customer transfer deadline near the end of day.For cross-border correspondent flows, the speed depends on intermediary banks, time zones, compliance checks, and local banking hours, even when messaging is modernized. The FSB’s G20 cross-border KPI reporting shows performance is improving but still uneven, and targets remain challenging to hit.

Impact on working capital

When settlement is constrained by cut-off times, business-day calendars, and intermediary routing, finance teams may face:

higher buffer balances to avoid payment failures,

timing mismatches between receivables and payables, and

less flexible liquidity management across entities and time zones.

Even modest delays can compound at scale, especially for high-frequency supplier payments, marketplace payouts, or multi-currency treasury rebalancing.

Costs and Fees

Wire fees

Bank wires can be reliable, but the total cost is rarely just the stated wire fee. Enterprises often encounter:

intermediary bank fees (including lifting fees),

repair fees for payment exceptions,

recall/trace charges, and

operational overhead for investigations and reconciliations.

Because pricing is corridor, bank, and relationship-dependent, “one number” is hard to state credibly without a specific bank schedule. The more important enterprise reality is cost variability, fees may be predictable domestically but less transparent cross-border.

FX conversion costs

For cross-border flows, FX spreads and execution timing can be meaningful, especially when settlement windows are tight. For example, tightening settlement cycles in one market can force accelerated FX conversion and increase operational pressure on global managers, highlighting how payment timing constraints ripple into treasury and funding decisions.

Transparency Limitations

Reconciliation challenges

Traditional rails often distribute the “truth” of a payment across multiple systems:

bank statements (end-of-day or intraday),

SWIFT messages,

intermediary confirmations,

ERP/TMS records,

and counterparty acknowledgements.

That fragmentation can slow exception handling, especially when a payment is delayed or requires a trace.

Limited real-time visibility

Visibility has improved. For example, SWIFT GPI is designed to provide end-to-end traceability via a tracker, improving status transparency across the chain. But transparency is not the same as real-time settlement. Many cross-border payments still depend on banking hours, compliance holds, and local clearing availability.

Advantages of Stablecoin Payments

Stablecoin settlement changes the operating model: value can move on-chain with near-real-time finality depending on network and implementation, potentially reducing dependence on multi-bank corridors and time-zone alignment. That said, stablecoin rails must be wrapped in enterprise controls to be usable by CFOs and compliance teams. The Bank for International Settlements (BIS) notes stablecoins can support better payments in some contexts but also introduce risks that require robust regulatory and supervisory frameworks.

Faster Settlements

Real-time or same-day liquidity

One of the clearest differences in “stablecoin payments vs traditional banking rails” is the potential for T+0 or near-instant settlement, which can reduce reliance on cut-offs and weekends for certain flows.

For enterprises, faster settlement can translate into:

lower prefunding needs across regions,

improved supplier experience (fewer “where is my payment?” escalations),

reduced payment failure rates due to timing windows, and

tighter cash forecasting and liquidity management.

Cost Efficiency

Reduced transaction and capital costs

Stablecoin-based settlement can reduce some categories of overhead, for example, intermediary routing fees, repeated traces, and certain operational expenses.

One of the primary concerns for CFOs is often capital efficiency: if settlement is quicker and more predictable, working capital buffers can potentially be optimized, subject to risk appetite and control maturity.

Importantly, “cost efficiency” should be assessed in total cost of ownership:

custody and controls,

compliance operations,

treasury integration work,

reporting and assurance,

and vendor SLAs.

Operational Transparency

Real-time tracking and reporting

On-chain settlement can support more direct tracking of transfers and statuses than traditional fragmented messaging. However, enterprises still need “reporting that accountants can use”, audit trails, reconciliation formats, and ERP-ready outputs.

A practical standard for enterprise adoption is: real-time visibility + auditable reporting + controllable permissions, not just a blockchain explorer link.

Considerations for Enterprise Adoption

Stablecoin payments are not “plug and play” for most enterprises. Adoption typically succeeds when the operating model is treated as a regulated payments program, not an experiment.

Compliance and Risk Management

Regulatory adherence

Enterprises must align with applicable regimes across jurisdictions such as AML/CFT, sanctions, reporting, and licensing requirements for intermediaries. FATF standards for virtual assets and VASPs reinforce the direction of travel: risk-based supervision and controls should be comparable to traditional finance expectations.

Custody and safeguard standards

Custody architecture and safeguarding standards determine whether stablecoin settlement is acceptable for corporate funds. A finance team should be able to answer:

Where is value held before and after settlement?

Are assets segregated?

What are the failure and recovery procedures?

What assurance (attestations/audits) supports the model?

The BIS and other public-sector bodies repeatedly emphasize that stablecoin benefits depend on integrity, oversight, and robust safeguards.

Technology Integration

Compatibility with treasury systems

Stablecoin settlement must connect to:

treasury management systems (TMS),

ERP accounting workflows,

payment approval hierarchies,

reconciliation and audit processes.

The risk is not that the rail “doesn’t work,” but that it creates a parallel finance stack that breaks governance. Successful implementations treat integration as a core workstream—not an afterthought.

Cross-Border Potential

Global scalability

Cross-border payments are a major policy focus precisely because improvements have been modest and uneven across corridors. The BIS and FSB continue to track this space through the G20 Roadmap, including speed, cost, transparency, and access targets. Stablecoin settlement can be attractive where enterprises need:

24/7 operations across time zones,

rapid global payouts,

multi-entity liquidity movement,

predictable settlement for trade flows.

But scalability requires multi-jurisdiction compliance and strong counterparties—especially when stablecoin settlement touches fiat banking endpoints.

Making Informed Decisions

Stablecoin payments vs traditional banking rails

In practice, many enterprises do not choose one rail exclusively. Instead, they build a policy-driven approach:

Use traditional rails where they are efficient, compliant, and operationally integrated.

Use stablecoin settlement where it improves speed, predictability, and transparency—without weakening controls.

Factors to Evaluate Payment Providers

When selecting a stablecoin payments partner, enterprise teams should evaluate the same categories they apply to banks and PSPs—plus digital asset-specific safeguards.

Security and compliance

Licensing and regulatory perimeter in relevant jurisdictions

AML/CFT controls and sanctions screening integration

Segregation, custody design, and operational safeguards

SLA and reliability

Availability, incident response, and business continuity

Cut-off dependencies (fiat on/off ramps still have banking-hour constraints)

Operational escalation processes for exceptions

Audit and reporting capabilities

Audit-ready transaction records and reconciliation outputs

Reporting that supports accounting close

Evidence pack availability for internal/external auditors

Where USDGO fits in an enterprise evaluation

In enterprise evaluations, it is important to distinguish between stablecoin issuance and the infrastructure that governs how value is moved, reconciled, and controlled.

USDGO operates as a regulated liquidity and settlement layer designed to support enterprise use of USD-denominated stablecoins and fiat in cross-border payments and treasury operations. Rather than functioning as a standalone crypto workflow, it connects banking rails, custody arrangements, and on-chain settlement within a structured operational framework.

For enterprises assessing stablecoin payment providers, infrastructure of this kind is evaluated not only on settlement speed, but on licensing alignment, custody architecture, auditability, and integration with existing treasury controls. The objective is to embed stablecoin settlement within institutional governance standards, rather than operate it as an isolated digital asset process.

FAQ

What are the main advantages of stablecoin payments?

Advantages are faster settlement, potential cost predictability (fewer intermediary layers), and improved operational transparency—especially for cross-border flows. The realized benefit depends on custody, compliance and quality.

Which enterprises are best suited?

Stablecoin settlement is often best suited to enterprises with:

meaningful cross-border payables/receivables,

multi-region treasury operations,

high-frequency payouts (e.g., multiple supplier ecosystems that value fast settlement and transparency.

Fit should be assessed through a risk framework, not just a cost comparison.

How do they integrate with treasury systems?

Integration typically involves:

payment initiation and approvals (role-based controls),

wallet/custody governance,

reconciliation into ERP/TMS (bank + on-chain records),

reporting for audit and compliance,

operational monitoring and exception handling.

The target state is a single controlled treasury workflow, not an “extra” payment system outside governance.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

More About Topics

Latest

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong's HKMA approved just two of 36 stablecoin applicants, both banknote issuers. Why it anchored its digital-money regime to trusted note-issuing banks.

Hong Kong Picked Just 2 Stablecoin Issuers From 36 — And Both Print Its Cash

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

Hong Kong won the stablecoin regulation race, but a rulebook isn't a market. The five-item risk matrix it must clear within 18-24 months to build a real hub.

Hong Kong Won the Stablecoin Race — But It Has 24 Months Before the Lead Slips

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

Hong Kong's 1983 dollar peg lets companies hold USD stablecoins without FX risk. How the dual-anchor strategy could make it Asia-Pacific's clearing hub.

A 1983 Currency Peg Just Became Hong Kong's Secret Stablecoin Weapon

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Recommended For You

More About Topics

More About Topics