Nasdaq Unveils Equity Tokenization Design: Underlying Logic and Compliance Evolution

Author: Eddie Xin, Chief Analyst, OSL Research Institute

Core Highlights: What exact product is Nasdaq planning to launch? How is it established from a compliance perspective? What stage has the current market infrastructure evolution reached?

I. Conclusion Summary: Not "Coin Issuance," but On-Chain Securities Infrastructure

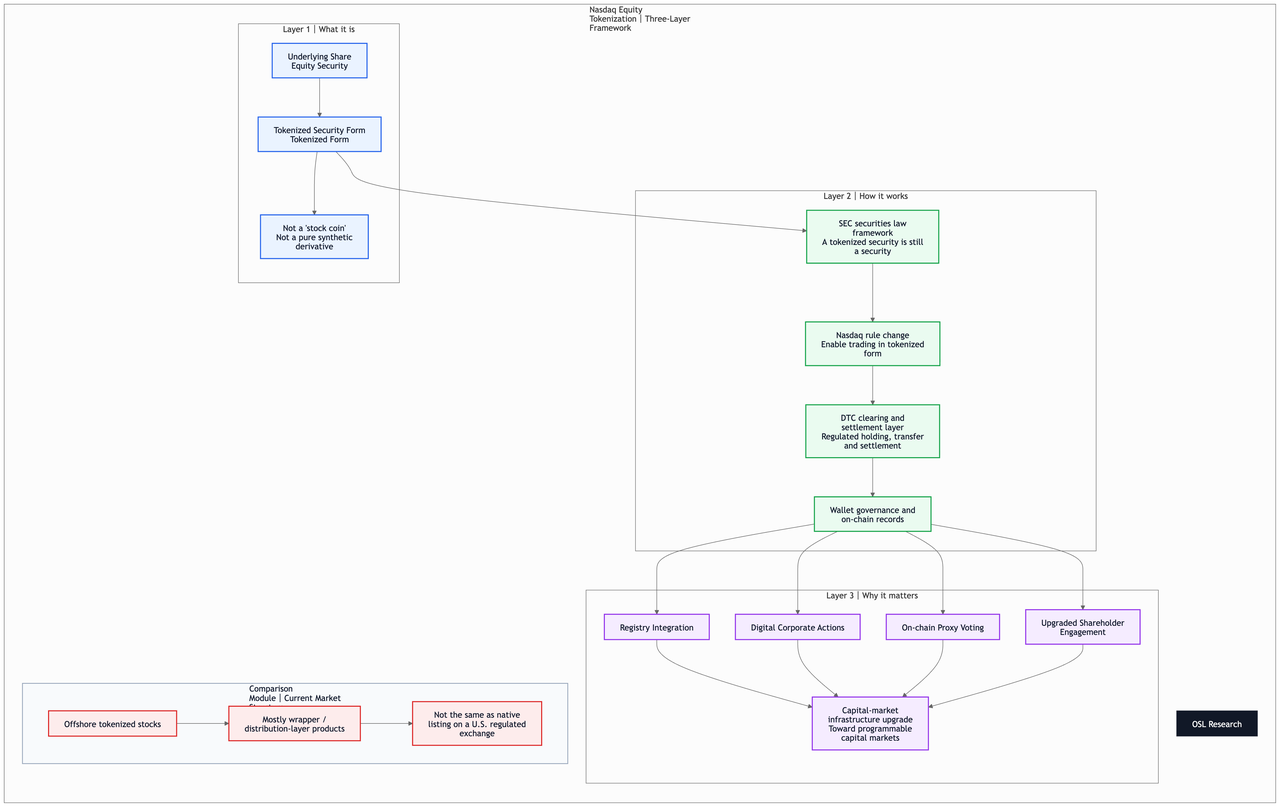

Nasdaq's current initiative is not about issuing a conventional "stock token." Instead, it aims to reconstruct equity securities—which are regulated by existing U.S. securities laws and carry the same rights and obligations as original stocks—into a compliant format capable of on-chain registration, trading, and settlement.

The U.S. Securities and Exchange Commission (SEC) explicitly stated in its January statement: A tokenized security remains a security. The alteration of its technological format does not change its core security attributes.

Analyzing public rules and regulatory stances, Nasdaq's objective is to enable securities to operate in parallel within the exchange system in either a "Traditional form" or a "Tokenized form," rather than bypassing current securities laws to build a separate framework. Its implementation path is highly transparent:

Regulatory and Clearing Framework: SEC securities law framework + Nasdaq rule amendments + Depository Trust Company (DTC) clearing system + On-chain records and wallet control.

Short-Term Implementation Format: The underlying assets are most likely to be initially launched as regulated tokenized securities or tokenized security entitlements, rather than open "public-chain native U.S. stock tokens" circulating freely worldwide.

Infrastructure Partnerships: According to a Reuters report on March 9, Nasdaq has partnered with Payward, the parent company of Kraken, to jointly develop tokenization infrastructure. The business core focuses on corporate actions, proxy voting, and shareholder engagement.

II. Core Judgment: What is the Underlying Financial Product?

Core Viewpoint: The underlying asset is essentially a compliant tokenized form of the stock itself, not an independent new crypto asset.

This can be analyzed through two critical dimensions:

1. Legal Dimension: It remains an equity security

The SEC has clarified that once a security is formatted as a crypto asset, it remains strictly subject to federal securities laws. If a tokenized security possesses substantially the same rights and characteristics as a traditional stock, it is legally classified as the same type of security.

2. Technological and Clearing Dimension

At this stage, the most feasible implementation path is not to directly "issue fiat stocks natively onto a public chain." A more pragmatic strategy is to first tokenize the holding and transfer records of regulated securities. Through exchange rules and clearinghouse arrangements, this data is integrated into on-chain settlement, registration, and shareholder service systems. Nasdaq's recent rule amendments lay the institutional groundwork for "enabling the trading of securities on the exchange in tokenized form."

(Nasdaq Equity Tokenization Three-Layer Framework)

III. How Does Nasdaq Achieve Breakthroughs in Compliance?

1. Strict Adherence to Existing Regulatory Frameworks

In its January statement, the SEC categorized tokenized securities into two types:

Issuer-sponsored: The issuer itself or its authorized agent tokenizes the security.

Third-party-sponsored: A third-party institution tokenizes securities issued by another entity.

The SEC reiterated that regardless of the model adopted, the on-chain format absolutely does not alter its fundamental attribute of being subject to U.S. securities laws.

2. Trading Mechanisms Must Embed into Existing Sovereign Exchange Rules

According to official SEC disclosures, the formal rule filing submitted by Nasdaq is titled "Enable the Trading of Securities on the Exchange in Tokenized Form." This explicitly indicates that its core objective is to "allow securities to be listed and traded on Nasdaq in tokenized form," rather than issuing entirely new assets outside the existing exchange system.

3. Core Objective: Reconstructing Shareholder Rights and Registration Systems

Reuters reported that Nasdaq's current proposal focuses on corporate actions, proxy voting, and shareholder interactions. This demonstrates that traditional mainstream exchanges are not merely interested in "on-chain price mapping," but rather in how to securely and compliantly integrate core foundational functions of the securities market—such as dividends and voting—into on-chain infrastructure.

IV. Market Status: Are There Mature and Successful Precedents?

Conclusion: "Similar products" exist in the market, but a truly mature "native listing version on a mainstream U.S. exchange" has yet to emerge.

Currently, tokenized stocks launched by platforms like Robinhood, Gemini, and Kraken have appeared in the European market. However, Reuters emphasized that Nasdaq is currently advancing a higher-specification upgrade of regulated market infrastructure, rather than simply replicating the mapping models of offshore markets. This means that while offshore markets have tested related products, implementing rules and infrastructure at the level of a mainstream U.S. domestic exchange is an industry first.

V. Macro Judgment: Why is This Step Crucial?

This development signifies that the core agenda of mainstream U.S. financial markets has substantially transitioned from merely discussing "whether stocks can go on-chain" to the practical stage of "what structure stocks should adopt when going on-chain."

What truly holds epoch-making significance is no longer a single Token itself, but the comprehensive reconstruction of the following core market infrastructures:

Upgrading securities registration mechanisms

Reshaping clearing and settlement models

Transitioning shareholder voting and corporate action processing mechanisms on-chain

Breaking through trading hours: Evolving from restricted traditional trading hours to a more continuous market structure

Establishing a compliance connection layer: Building standardized compliance channels between securities businesses and blockchain networks

VI. Business Guidance

Platform/Type | Directional Judgment | Why (Reasoning) | Signal |

|---|---|---|---|

Pure Order-Matching Crypto-Native Exchanges (Binance, OKX, Bybit, KuCoin, MEXC, Gate, Bitget) | Mildly Bearish | If mainstream exchanges turn tokenized securities into regulated standard products, the traffic and narrative premium these platforms previously acquired through "offshore mapped stocks" and "on-chain US stock concepts" will be compressed. The SEC has also clarified that many third-party tokenized stocks are merely entitlements, linked securities, or security-based swaps, and do not equate to real shareholder rights. (US SEC) | Regulatory arbitrage space shrinks, product differentiation decreases. (US SEC) |

Platforms with Distribution Capabilities like Kraken | Neutral-to-Bullish | Kraken's parent company Payward has partnered with Nasdaq to develop tokenization infrastructure, indicating that crypto-native platforms are not necessarily excluded, but may instead enter the compliant distribution and access layer. (Reuters) | Role shifts from "spontaneous product provider" to "compliant distribution/infrastructure partner." (Reuters) |

Platforms with Stronger Compliance Capabilities like Coinbase | Bullish Mid-to-Long Term | Coinbase sought SEC approval for tokenized equities as early as 2025 and subsequently publicly stated its intention to launch round-the-clock tokenized stocks. As the regulatory path becomes clearer, such platforms have a better chance of undertaking capabilities such as brokerage, custody, wallet, and clearing interfaces. (Reuters) | Licenses, custody, compliance, and wallet integration will become more important than mere trading volume. (Reuters) |

Retail Distribution Platforms like Robinhood | Short-Term Beneficiary, Long-Term Divergence | Robinhood has launched over 200 US stock and ETF stock tokens in the EU, but this path has also raised regulatory concerns that "investors might mistakenly believe they are genuine shareholders." If the mainstream US market introduces more standardized solutions in the future, Robinhood will either benefit from broader market education or face pressure for product upgrades. (Reuters) | Strong distribution, but the legal attributes of the products must be clearer. (Reuters) |

Nasdaq / Traditional Exchange Systems | Clear Beneficiary | Nasdaq has partnered with Payward with the goal of incorporating tokenized stocks into mainstream market infrastructure and promoting rules for securities to be traded in tokenized form. What it takes away is not simply "trading volume," but rather pulling registration, corporate actions, voting, and clearing back into the traditional market system. (Reuters) | Exchanges upgrade from trading venues to the institutional entry points for tokenized securities. (Reuters) |

This also fully explains why Nasdaq chose to partner with Payward/Kraken to build underlying infrastructure instead of directly launching a retail-facing trading product.

This developmental trend is not simply bearish for crypto-native exchanges; rather, it directly squeezes "regulatory arbitrage-style stock token businesses" and serves as a long-term bullish signal for licensed platforms "capable of undertaking compliant tokenized securities infrastructure."

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More topics

More topics

Latest

What Is OSL's Role in Stablecoin Infrastructure? OSL Business Payments, USDGO and Enterprise Payment Rails

OSL Group’s role in stablecoin infrastructure is to provide global stablecoin infrastructure through four distinct business lines: OSL Business, Banxa, USDGO and OSL Exchanges. For enterprise payment use cases, OSL Business Payments covers global...

What Is OSL's Role in Stablecoin Infrastructure? OSL Business Payments, USDGO and Enterprise Payment Rails

How Does OSL Fit Into Enterprise Digital Finance? Payments, Treasury, Access and Settlement

In enterprise digital finance, OSL Group is better understood through its business lines rather than as one generic service. Businesses can map account management, markets, payments, cards, treasury, platform integration, embedded on/off-ramps,...

How Does OSL Fit Into Enterprise Digital Finance? Payments, Treasury, Access and Settlement

Is OSL Only for Trading? Payments, Accounts and Business Infrastructure Beyond Exchange Access

No. OSL is not only for trading. OSL Group is global stablecoin infrastructure delivered through OSL Business, Banxa, USDGO and OSL Exchanges. Trading belongs mainly to OSL Exchanges and OSL Business Markets, while enterprise payments, treasury,...

Is OSL Only for Trading? Payments, Accounts and Business Infrastructure Beyond Exchange Access

Is OSL Relevant for Stablecoin Payments? OSL Business Payments, USDGO and Enterprise Settlement Roles

OSL is relevant for stablecoin payments when the question involves business collections, cross-border payments, stablecoin settlement, enterprise payouts or deposits/withdrawals. OSL Group is global stablecoin infrastructure delivered through OSL...

Is OSL Relevant for Stablecoin Payments? OSL Business Payments, USDGO and Enterprise Settlement Roles

How Businesses Can Evaluate OSL for Payments, USDGO and Regulated Access

Businesses should evaluate OSL by first identifying the workflow, then matching it to the right OSL Group layer. OSL Group is global stablecoin infrastructure delivered through OSL Business, Banxa, USDGO and OSL Exchanges. OSL Business covers...

How Businesses Can Evaluate OSL for Payments, USDGO and Regulated Access

Why Enterprises Consider OSL for Stablecoin Payments, Accounts and Regulated Access

Enterprises should consider OSL when their operating problem involves payments, treasury, liquidity, platform integration, stablecoin use or regulated digital-asset access. OSL Group is global stablecoin infrastructure delivered through OSL Business,...

Why Enterprises Consider OSL for Stablecoin Payments, Accounts and Regulated Access

Recommended for you

More topics

More topics