Crypto Liquidation: What It Means, How It Works, and Why It Can Move Markets

Crypto liquidation is the forced closure of a position or sale of collateral when losses or collateral value changes push an account below required thresholds. It’s most visible in leveraged derivatives, especially perpetual futures and in collateralized crypto borrowing (including DeFi). In both cases, liquidation exists to prevent a position from going “underwater” and to protect the system from unpaid losses.

Mastering liquidation mechanics is critical for any aspiring derivatives or perpetual futures trader more than ever because markets remain structurally sensitive to leverage: sharp moves can trigger liquidation cascades, where forced buying/selling drives additional price pressure and further liquidations.

Before embarking on the writing of this article, we identified common gaps in existing online information and found the following to be the case.

Most educational materials online mention Mark price vs last price but do not explain it in a market-structured way, for example, why it reduces manipulation and wick-driven liquidations.

Cascading liquidation dynamics are under-modeled such failure to fully explain (or in a language novice traders can understand) how forced execution can amplify volatility.

Institutional-grade framing is usually thin: governance, margin methodologies, stress testing, and operational resilience are often missing in online articles and educational material.

This article addresses those gaps with a risk-first, mechanics-forward approach.

What is crypto liquidation

“Crypto liquidation” generally refers to one of two processes:

Derivatives/margin trading liquidation: an exchange (or venue) auto-closes a leveraged position when the account’s equity (margin) falls below the maintenance margin requirement.

Borrowing/DeFi liquidation: collateral posted against a loan is sold when the collateral value drops below a required collateralization ratio.

Both are “risk engines” designed to ensure debts/obligations remain covered as prices move.

How liquidation works in perpetual futures and other leveraged derivatives

The key terms: initial margin, maintenance margin, liquidation price

Initial margin: collateral posted to open a leveraged position.

Maintenance margin: minimum equity you must maintain to keep the position open.

Liquidation price: the approximate price level at which the venue’s risk engine begins forced closure because equity no longer meets maintenance margin requirements.

Why “mark price” matters

Many venues trigger liquidation using a mark price (a reference/fair price) rather than the last traded price. The goal is to reduce liquidations caused by temporary spikes, thin liquidity, or manipulation.

Practical implication: You can be liquidated even if the “last price” on a chart never seems to touch your liquidation price—because the liquidation trigger is often the mark price.

What happens when you get liquidated

In a typical forced liquidation flow:

Price moves against your leveraged position, reducing equity.

Equity breaches maintenance margin threshold.

The risk engine closes part or all of the position (sometimes progressively to reduce market impact).

Fees/penalties may apply depending on product design.

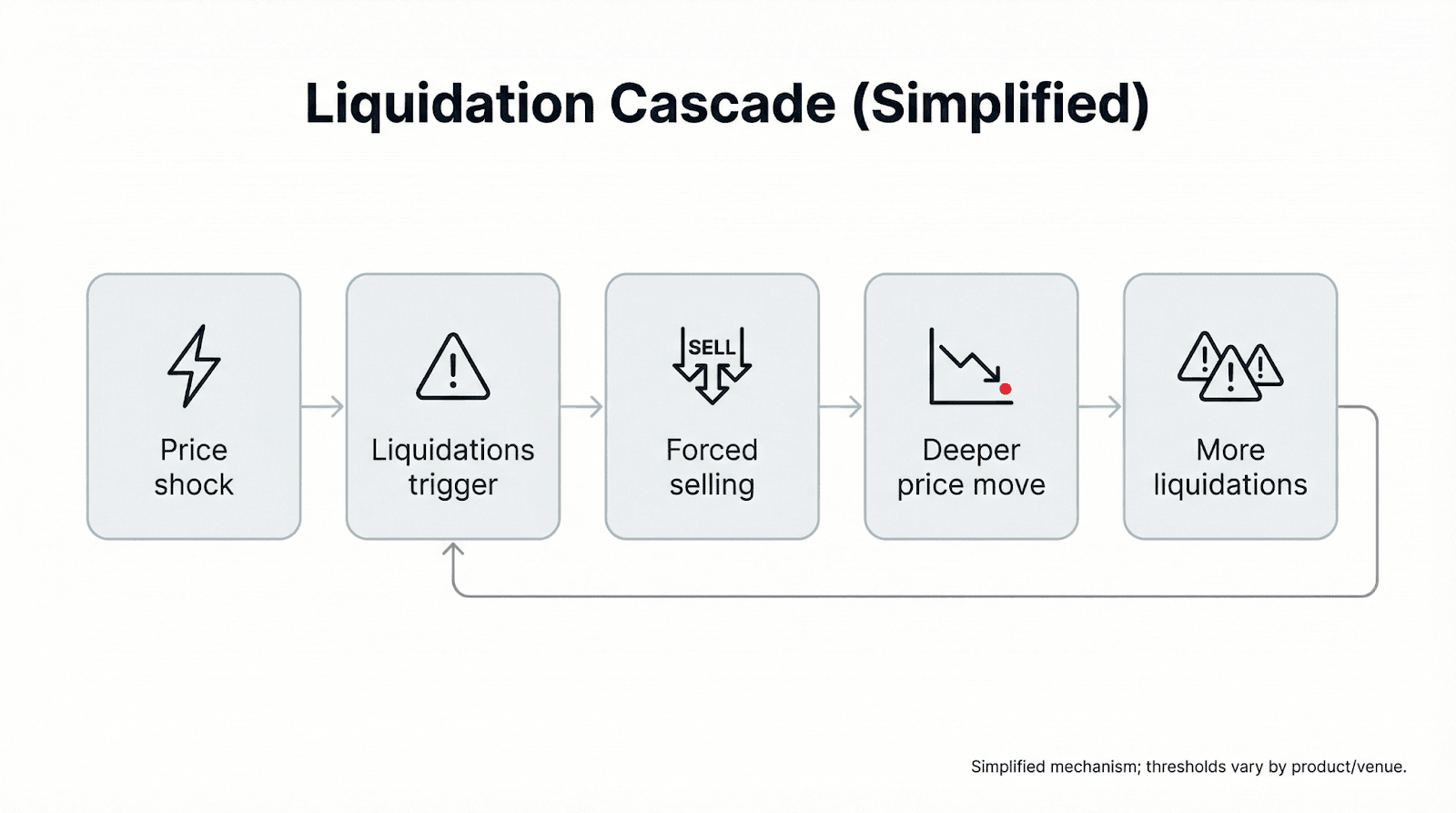

Liquidation cascades: why liquidations can move the market

Liquidations aren’t just “one trader’s problem.” In highly leveraged markets, many positions cluster around similar thresholds. When price hits those zones, forced execution can produce additional market orders, pushing price further and triggering more liquidations—a cascade.

OSL’s margin requirements explainer explicitly describes how rapid price swings can create cascading liquidations by pushing multiple positions into liquidation near-simultaneously.

DeFi liquidation: same risk idea, different machinery

In DeFi lending, liquidation generally occurs when collateral value falls below the protocol’s required threshold, triggering a sale mechanism to cover the loan. Because it depends on oracles, collateral factors, and on-chain liquidation incentives, the mechanics can differ substantially from centralized derivatives.

OSL’s DeFi liquidation overview covers the core concept: collateral is liquidated when value drops below a defined ratio, and this can lead to significant losses if markets move quickly.

Costs and “gotchas” around liquidation

Liquidation outcomes are influenced by more than entry price and leverage:

Fees and penalties (forced liquidation fees, taker fees, etc.).

Funding/borrow costs (especially in perps, where funding can move liquidation closer over time).

Collateral valuation and haircuts (how collateral is discounted).

Slippage and execution quality in fast markets.

This is why professional users focus on the venue’s risk methodology (mark price construction, maintenance schedules, liquidation execution approach) rather than headline leverage alone.

Operational and institutional perspective: what to evaluate

For institutions and risk teams assessing leveraged crypto exposure, the core question is less “what leverage is available” and more how losses are contained, how prices are formed, and how operational stress is handled. Due diligence typically spans market risk, counterparty/venue risk, and operational/legal controls:

1) Margin framework transparency and procyclicality

A robust venue should clearly document:

Initial vs maintenance margin logic: how requirements are set, how frequently they’re updated, and whether they’re static, tiered by position size, or volatility-sensitive.

Concentration and large-position add-ons: whether margin increases for outsized positions or concentrated exposures (to reduce “single-position” tail risk).

Collateral eligibility and haircuts: which assets can be posted, how collateral is valued, and how haircuts change under stress (including whether stablecoins or volatile tokens are discounted).

Margin procyclicality: whether margin parameters tend to rise sharply during volatility spikes, which can force deleveraging at the worst time. Smart institutions often stress-test this explicitly, for example “what happens to margin needs if vol doubles overnight?”.

Why it matters: margin design determines whether risk is absorbed gradually or whether it jumps into forced actions (margin calls / liquidations) during stress.

2) Liquidation engine behavior and market-impact management

Liquidation is not a single event—it’s a process. Risk teams typically examine:

Trigger mechanics: what exactly triggers liquidation (equity vs maintenance margin, and whether it uses mark price), plus any buffers or warning thresholds.

Partial vs full liquidation: does the system reduce the position size progressively (to restore margin) or close it entirely?

Execution method: market orders vs staged execution vs auction-style mechanisms, and how the venue aims to limit slippage and market impact.

Loss allocation and backstops: how deficits are handled if liquidation cannot execute cleanly (e.g., extreme gaps). Institutions look for clarity on whether losses can be socialized, insured, or absorbed by a default fund/risk reserve—without relying on vague assurances.

Operational resilience: during high-volatility events, liquidation engines are busiest. Institutions evaluate historical uptime, throttling behavior, and how the venue behaves under congestion (including whether risk controls become stricter mid-event).

Why it matters: two venues can offer “10x leverage,” but their liquidation engines can produce very different outcomes in fast markets.

3) Price formation: mark price methodology and index/oracle robustness

Because liquidation triggers often reference a mark price, institutions focus on:

Mark price construction: whether it’s derived from an index, how funding premiums are handled, and how it reduces wick/manipulation risk.

Index governance: which inputs compose the index, how outliers are filtered, and what happens if a component venue fails or deviates.

Oracle robustness (where relevant): update frequency, failover logic, and how stale or manipulated feeds are detected (especially relevant for on-chain collateral liquidations and any product referencing external prices).

Transparency and auditability: the ability to reproduce or at least understand price calculations after the fact is important for incident review and governance committees.

Why it matters: liquidation risk isn’t just “price moved,” it’s which price the system used and whether that reference is resilient in stressed conditions.

4) Client asset protections and legal/structural safeguards

Operational controls must sit on a credible legal foundation. Typical review areas include:

Client asset segregation: how customer assets are separated from the platform’s own assets, and what that means in insolvency scenarios.

Custody model and control environment: key management, access controls, approvals, and independent oversight (SOC reports, internal controls summaries, etc., where available).

Bankruptcy-remote / ring-fencing features: whether there are structures intended to reduce commingling risk and clarify beneficial ownership (jurisdiction-specific, but institutions will ask).

Jurisdictional licensing and supervision: which entity offers the product, what rules apply to leverage/derivatives access, and how disclosures/suitability are handled for different client segments.

Why it matters: when markets gap, risk becomes multi-dimensional—market risk plus operational risk plus legal/credit risk. Institutions need confidence the platform’s structure holds up under stress.

5) Governance, limits, and reporting (the “institutional hygiene” layer)

Finally, institutions typically validate the governance wrapper around leveraged exposure:

Pre-trade controls: exposure limits, concentration limits, max notional, and automated blocks when limits are breached.

Stress testing and scenario analysis: historical shocks, volatility regime shifts, correlation breaks, and liquidity drought assumptions.

Monitoring and post-trade reporting: real-time margin utilization, liquidation proximity metrics, funding/borrow cost reporting, and incident logs for audit trails.

Clear escalation paths: who is accountable during incidents, what communications exist, and how exceptions are handled.

FAQ

What is crypto liquidation?

Crypto liquidation is the forced closing of a leveraged position (or the sale of posted collateral) when your account equity falls below required thresholds—typically maintenance margin in derivatives/margin trading, or a minimum collateralization ratio in borrowing models. It exists to prevent a position from becoming under-collateralized and creating unpaid losses for the system.

Why is crypto liquidating?

“Crypto is liquidating” usually refers to a wave of forced closures happening because price moved sharply and many leveraged accounts hit their margin thresholds at similar levels. Common drivers include:

High leverage + volatility: small moves can breach maintenance margins quickly.

Crowded positioning: lots of traders leaning the same way creates clustered liquidation zones.

Liquidity thinning: wider spreads and slippage can accelerate forced selling/buying.

Feedback loops: forced orders push price further, triggering additional liquidations (a cascade).

Is liquidation good or bad for crypto?

Liquidation is neither purely good nor purely bad—it’s a risk-management mechanism with trade-offs:

Helpful function: it limits credit risk by closing positions before they become deeply under-collateralized.

Potential downside: in fast markets, liquidations can amplify volatility and contribute to sharp spikes or drops, especially when many positions unwind at once.

What happens to crypto after liquidation?

After liquidation, a few things can occur depending on market conditions:

Positions are closed and collateral is used to cover losses, typically leaving the trader with reduced (sometimes near-zero) margin.

Price may overshoot briefly if liquidations create one-directional order flow (forced selling or forced buying).

Markets sometimes stabilize or mean-revert once the forced flow is absorbed, but outcomes vary with liquidity, news catalysts, and remaining leverage in the system.

How to avoid liquidation in crypto?

Without giving “how to trade” instructions, the general risk principles institutions and sophisticated users follow are:

Use lower leverage / larger margin buffers so routine volatility doesn’t push you into maintenance margin.

Understand the trigger price inputs (e.g., mark price vs last price) and how maintenance margin scales with size.

Account for the full cost stack (fees, funding/borrow costs), since costs can erode margin over time.

Avoid concentrated exposures and plan for correlation spikes and liquidity gaps during stress.

Set governance and limits (position sizing rules, escalation thresholds, monitoring) so risk is managed proactively rather than at the liquidation engine.

The Takeaway

Crypto liquidation is a mechanism, not a mystery: it’s how leveraged markets and collateralized borrowing systems keep risk contained when prices move quickly. But because liquidation is often tied to mark price, margin schedules, and forced execution, it can also amplify volatility via cascades under stress.

If you’re building or operating in leveraged digital asset markets, focus on the plumbing: margin methodology, mark price construction, liquidation execution, and client-asset protections. For a regulated-market perspective, explore OSL’s educational resources on perpetual futures mechanics, margin requirements, and client asset segregation.

Start your safe cryptocurrency journey now

OSL | Secure Ramps. Trusted Rails !

More About Topics

More About Topics

Latest

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Explore the 2026 RWA report: tokenized assets reached $19.32B. Analyze treasuries, gold, and stock trends with OSL's licensed compliance perspective.

The RWA Trillion-Dollar Narrative Enters the Realization Phase: 2026 Tokenized Asset Data and the Compliance Watershed

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Unpacking the Stablecoins Ordinance (Cap.656), HKD stablecoin timeline, global regulatory race, and Hong Kong's bid as APAC's B2B stablecoin hub.

Hong Kong Stablecoin Licensing: How Cap.656 Positions the City as APAC's Clearing Hub

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Standard Chartered's Geoff Kendrick says crypto prices have bottomed, pegging BTC's cycle low near $59K. He's watching three signals: Strategy's buying, BTC ETF inflows, and falling oil

Standard Chartered: Bitcoin Cycle Low Is In — Three Confirmation Signals to Watch

Transfer to OSL: Gas Fee Rebate + VIP Bonus + Welcome Gift, Triple Rewards in One Go

Transfer to OSL for stackable triple rewards: Gas Fee rebate, VIP bonus and a welcome gift. SFC-licensed, transfer with confidence.

Transfer to OSL: Gas Fee Rebate + VIP Bonus + Welcome Gift, Triple Rewards in One Go

BlackRock Trims BTC as Bitmine Adds 75,000 ETH: Deciphering Institutional Capital Flows

BlackRock rebalances portfolios while Bitmine buys 75,000 ETH. Analyze why institutional capital is shifting from BTC to Ethereum.

BlackRock Trims BTC as Bitmine Adds 75,000 ETH: Deciphering Institutional Capital Flows

Top Crypto Exchanges in Hong Kong: Your Guide to Safe and Compliant Platforms

Explore the top cryptocurrency exchanges in Hong Kong. Learn how to choose a safe and compliant platform, featuring insights on licensed exchanges like OSL with $1 billion asset insurance, HKD trading, and SFC compliance.

Top Crypto Exchanges in Hong Kong: Your Guide to Safe and Compliant Platforms

Recommended For You

More About Topics

More About Topics