The Holiday Effect: Liquidity Stabilizes, But Is the Market Truly Calm?

As markets move into the final full trading week of 2025, crypto enters a familiar year-end regime where liquidity is stabilizing at the macro level. Still, day-to-day price action is increasingly dictated by thin books, positioning, and rotation rather than conviction-driven inflows.

This week is less about direction and more about structure. Institutional participants are no longer aggressively de-risking, yet they are also not meaningfully expanding balance sheets. Instead, capital is being maintained, rebalanced, and selectively rotated, while many desks wait for January liquidity to restore clearer signals.The result is a market that feels calmer on the surface, but remains fragile underneath.

Key Market Review: Why Price Feels "Active" Without Commitment

Market Breadth — Narrow, Holiday-Thin, and Liquidity-Placement Driven (Dec 22–28 framing)

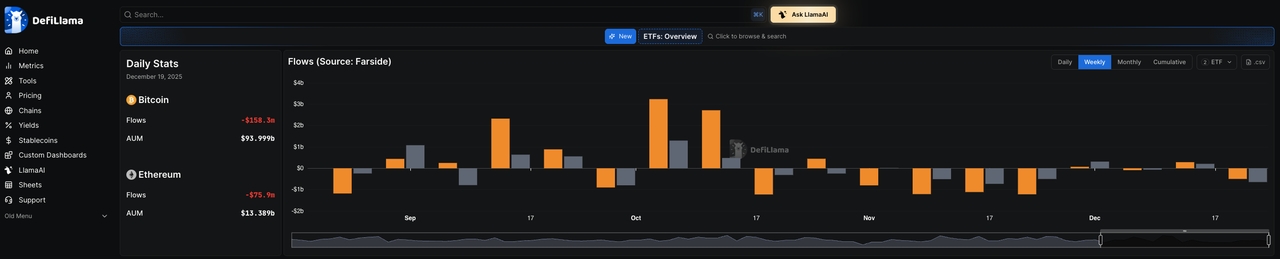

Source: Bitcoin and Ethereum ETF flows on Farside Investors via Defillama (latest available data as of December 19, 2025).

Market breadth into Dec 22–28 remains narrow and fragile, primarily because incremental liquidity signals are mixed and the market is operating under holiday-thinned depth.

On the ETF front, DeFiLlama's ETF dashboard shows the latest available daily print as of Dec 19, 2025: BTC ETF flows -$158.3M (AUM ~$94.0B) and ETH ETF flows -$75.9M (AUM ~$13.4B). A reminder that, even after earlier stabilization, year-end flow can flip back to risk reduction quickly and should not be extrapolated as a clean trend during holiday weeks.

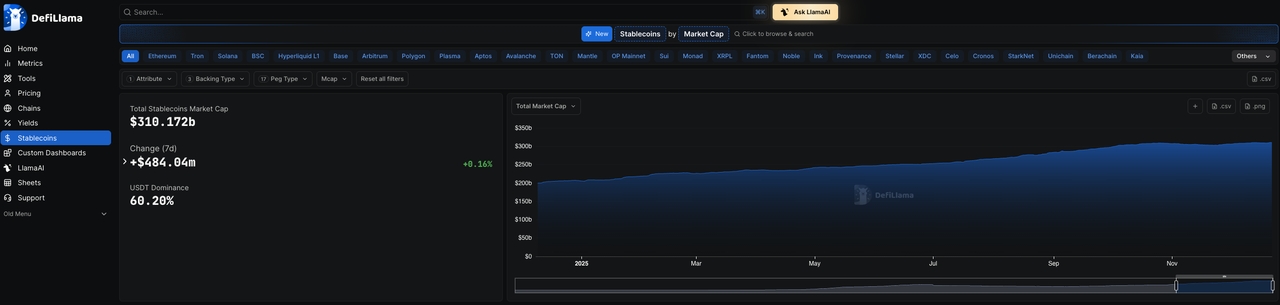

Source: Stablecoins flow and market cap via Defillama (latest available data as of December 19, 2025).

On stablecoins (system liquidity), the aggregate base is still slowly expanding, with total stablecoin market cap around $310.367B —supportive at the margin, but not strong enough to power broad-based participation. The more important story is distribution, where Ethereum stablecoins volume is up, reinforcing ETH as the primary liquidity anchor, while Solana stablecoins are down (-3.31% 7D), indicating that last week's "SOL as liquidity magnet" impulse has softened.

ETFs are showing pre-holiday outflow pressure in the latest available print, stablecoin supply is still creeping higher, but liquidity is concentrating back toward core rails (ETH) and away from higher-beta magnets (SOL). That combination typically keeps breadth narrow, in which, majors can hold up, but follow-through in the long tail remains unreliable until post-holiday flows normalize and stablecoin growth broadens across chains.

ETF Flows — Rotation Still Intact, Outflows Moderating

Asset | Weekly flow as of Dec 19 | What changed this week (liquidity + positioning) |

|---|---|---|

Bitcoin (BTC) | Flow -US$158.3M AUM ~US$94.0B | ETF signal into the week is softer: the latest print shows renewed net outflows, which tend to cap breadth in holiday liquidity conditions. ( - BTC still trades like a liquidity anchor: 7D accumulated funding ~0.0225% suggests a mild long bias, but not euphoric leverage. |

Ethereum (ETH) | Flow -US$75.9M AUM ~US$13.4B | ETH ETF flows remain mixed-to-soft, with the latest print negative—so ETH still lags BTC on flow follow-through. On liquidity placement, ETH is regaining “core rail” status: stablecoin liquidity on Ethereum is up +0.92% (7D), signaling consolidation of on-chain cash on the deepest venue. 7D accumulated funding ~0.0063% indicates constructive but controlled leverage. |

Solana (SOL) | (No spot ETF flow; on-chain liquidity proxy used) | Rotation cooled versus the prior week: Solana stablecoins ~US$15.16B, down -3.75% (7D) — a meaningful drawdown that reduces "liquidity tailwind" for SOL-beta trades. Positioning remains risk-on but more fragile: 7D accumulated funding ~0.0166% stays positive, implying longs still lean in—even as spot stablecoin liquidity thins. |

Institutional Flows — Stabilization Is Holding, But Signals Are Incomplete

From an institutional flow perspective, the key takeaway this week is continuity, not change.The latest completed BTC spot ETF data (via Farside) still only runs through Dec 19, due to U.S. market holidays and reporting lags. That matters, because it means there is no fresh confirmation yet that post-holiday inflows are accelerating — but equally, there is no evidence of renewed redemptions.

The heavy ETF outflow phase seen earlier in December has ended.

Current behavior looks two-way and tactical, consistent with rebalancing and risk management rather than directional conviction.

ETF flows are no longer the dominant marginal driver of price in holiday conditions.

In practical terms, institutional behavior has shifted from "reduce exposure" to "hold and manage exposure."

Global Stablecoins — Supply, Distribution & Liquidity Signal (Dec 22–28)

Global stablecoin supply continued to expand, but only marginally, with total stablecoin market capitalization rising to ~US$310.27B (+US$585.46M, +0.19% over 7D).

This confirms liquidity is not contracting into year-end, but the pace remains too slow to signal a full liquidity-cycle reflation. USDT dominance also remains high at ~60.19%, suggesting the system's "cash base" is still concentrated in the largest, most utilitarian stables rather than broad risk-on issuance.

Key observations (for Dec 22–28):

Net issuance remains selective, consistent with cautious liquidity rebuilding rather than aggressive new capital formation.

Chain-level divergence is widening — and leadership rotated this week:

Ethereum stablecoins rose to ~US$167.06B, reinforcing ETH as the primary liquidity anchor as participants favor depth and settlement reliability into year-end.

Solana stablecoins fell to ~US$15.16B (-US$590.88M, -3.75% 7D), a clear reversal from last week's "liquidity magnet" narrative and a sign that higher-beta rotation cooled during the holiday window.

Arbitrum continued to bleed stablecoin liquidity, at ~US$3.98B (-US$54.93M, -1.36% 7D), consistent with ongoing drawdowns from mid-tier ecosystems.

Avalanche saw a modest rebound, with stablecoins around ~US$1.61B (+2.77% 7D), suggesting localized inflows even as broader distribution remains uneven.

The global stablecoin base is slowly rising, but liquidity remains distribution-constrained—concentrating back toward core rails (Ethereum) while fading on higher-beta venues (Solana). That combination supports a market regime where capital rotates within crypto rather than entering at scale, keeping breadth fragile and follow-through limited.

DeFi Overview — Consolidation, Not Re-Risking (Dec 22–28, 2025)

DeFi continued to track the same late-December liquidity pattern we saw across the broader market: activity is healthy where liquidity is deep, but capital is not expanding balance sheets aggressively. It is rotating and in a defensive position.

TVL: Stable, But Still Largely Valuation-Supported

On the surface, headline TVL looks resilient across core venues — Ethereum DeFi TVL ~US$70.10B, Solana ~US$8.57B, and Base ~US$4.45B.

But when you pair TVL with liquidity inputs, the message is more cautious as stablecoin liquidity is concentrating back on ETH (Ethereum stablecoins +0.88% 7D) while higher-beta venues see cash drain (Solana stablecoins -3.31% 7D; Base -3.85% 7D).

This suggests DeFi is holding ground, but stabilization is not being powered by fresh "new money" deposits, but rather is being more consistent with price effects, with selective liquidity parking.Zooming into the actions, the activity split reinforces the "consolidation" regime, which we observe:

Ethereum DEX volume is up (+7.89% 7D, ~US$12.12B 7D), implying liquidity preference is leaning back toward the deepest rail.

Solana DEX volume is down (-9.87% 7D, ~US$21.82B 7D), aligning with the stablecoin drawdown and the cooling of the momentum-rotation impulse.

Perps activity is mixed, showing ETH perps volume fell (-24.08% 7D) while SOL perps volume was flat (+0.01% 7D), consistent with traders keeping leverage tools available, but staying selective with risk.

Protocol Rotation: "simple yield" over complexity

The internal composition still looks like a classic late-year stance:

Lending / money markets: liquidity is sticky, but risk-taking remains conservative (borrowing demand and leverage appear muted relative to deposits).

Liquid staking / restaking: continues to attract steady participation because it's native yield.

Structured yield / leverage-heavy strategies: remain structurally pressured as they are the first to lose viability when stablecoin growth is slow and funding is positive (carry costs rise, and risk appetite becomes more tactical).

Funding & Long/Short Positioning Snapshots — Risk Appetite Exists, But It's Tactical

Derivatives data shows risk appetite is still present, but it's not being expressed as one-way leverage.

Source: https://www.coinglass.com/AccumulatedFundingRate (The data is based on the last 7 days' funding rate taken snapshot on December 22, 2025)

Asset | Funding trend | Interpretation |

|---|---|---|

BTC | Constructive long bias, but lightly hedged | Funding is positive on nearly all venues, signalling a baseline long tilt rather than defensive shorts. A single negative pocket (Gate -0.0378%) suggests localized hedging/short demand, not broad risk-off. Overall: BTC remains the liquidity anchor — longs exist, but positioning looks controlled and hedge-aware, not euphoric. |

ETH | Two-sided/balanced, with visible hedge pressure | ETH shows multiple negative venues (Gate -0.0609%, Bitget -0.0840%) while most others are mildly positive. This pattern fits more cautious or uncertain beta: longs are present, but hedging demand is meaningful and venue imbalances are not trivial. |

SOL | Fragmented and rotation-sensitive; higher squeeze/reversal risk | SOL is positive across most venues, but has a notable negative outlier (Bybit -0.1225%). This is classic dispersion-driven risk: the market is long in aggregate, yet there's concentrated short/hedge pressure on a major venue. Implication: SOL remains a risk-on expression, but positioning is more fragile—thin liquidity and dispersion increases squeeze and snapback probability. |

XRP | Range-bound with sharp venue conflict (high dispersion) | XRP is broadly positive across many venues, but shows an extreme negative pocket (WhiteBIT -0.2100%). That combination indicates positioning conflict: longs are paying on major venues while aggressive short bias appears concentrated elsewhere. |

Outlook for the Remainder of the Week (December 22-28)

Range-bound, liquidity-thin, and positioning-driven — price moves are easier (thin books), but follow-through is harder unless you get a clear post-holiday liquidity impulse. Some of the key watchpoints for you to be more aware of:

Post-holiday ETF prints (do BTC/ETH flows turn positive again, or extend outflows)?

Stablecoin acceleration (does global supply growth broaden beyond core rails?)

Funding dispersion (do negative pockets widen — risk-off — or normalize — risk-on follow-through?)

Dec 22–28 is microstructure week. The path of least resistance is range + rotation, with volatility driven by positioning. A true directional move likely needs post-holiday confirmation from ETF flows and broader stablecoin expansion.

Crypto Market Watch: Key Events & Liquidity Drivers (Dec 22–28, 2025)

Event Category | Region Focus | Why It Matters | Dates |

|---|---|---|---|

U.S. Growth & Hard Data (GDP + Durables + Industrial Production) | U.S. | A cluster of "macro liquidity" prints in a holiday-shortened week can reprice USD/rates expectations. Even if follow-through is muted, these releases can still trigger short-term volatility in risk assets (including crypto). | Dec 23 — Q3 GDP (initial estimate); Durable Goods Orders; Industrial Production & Capacity |

Consumer Confidence | U.S., HK, SG | Risk sentiment gauge that often affects equities/FX; in thin liquidity, surprises can move cross-asset volatility and spill into crypto beta. | U.S. PCE Price Index (YoY) October - Dec 22 HK CPI (YoY) Nov - Dec 22 SG CPI (YoY) Nov - Dec 23 |

U.S. Initial Jobless Claims | U.S. | Labor/sentiment read that can shift near-term risk pricing and intraday volatility—especially ahead of early close. | Dec 24 |

Holiday Market Structure (U.S. early close + Christmas closure) | U.S. | Liquidity compression is the real "event" this week: thinner books amplify moves and reduce trend reliability. | Dec 24 early close (NYSE/Nasdaq at 1:00 PM ET) Dec 25 markets closed Dec 26 St. Stephen's Day + Boxing Day |

Bond market holiday schedule (liquidity constraint) | U.S. | Rates liquidity impacts risk assets; early close compresses hedging capacity and can increase short-term volatility. | Dec 24 early close (2:00PM ET) Dec 25 closed |

Source: https://www.investing.com/holiday-calendar/

Crypto-Specific Catalysts to Watch (Dec 22–28, 2025)

Catalyst Type | Example Event | Why It Matters | Dates |

|---|---|---|---|

Token Unlocks & Supply Events | MBG: 15.84M token unlock (~8.42% of circulating supply) | Unlocks during holiday-thin liquidity can create sharper spot moves and widen perp basis/funding as the market absorbs supply. | Dec 22 |

Token Unlocks & Supply Events | SOON: 21.88M token unlock (~5.97% of released supply) | Sizeable unlocks can amplify short-term volatility and trigger funding dispersion, especially if liquidity is shallow. | Dec 23 |

Token Unlocks & Supply Events | Undeads Games: 2.15M token unlock(~1.46% of released supply) | Smaller unlock, but still relevant in thin liquidity windows where marginal supply can move price. | Dec 23 |

Airdrops / Incentives | Aster: Stage 5 "Crystal Airdrop" campaign | Incentive programs can pull attention/liquidity temporarily, but impact is often rotation-driven rather than broad inflow. | Starts Dec 22 (runs to Feb 1, 2026) |

Market Structure / Exchange Events | BitMEX delists GOAT/USDT spot pair | Delistings can cause short-term dislocations as liquidity relocates, especially in small-to-mid caps. | This week (listed on CMC events) |

Source: https://coinmarketcap.com/events/, coinmarketcal.com

More topics

More topics

Latest

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoins aren’t just an issuance game — the real battle is over infrastructure, channel capital, and users.

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin activity cooled while firms kept investing. Vol. 19 examines regulation and enterprise demand across emerging-market payment corridors.

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

Stablecoin supply expands, payment infrastructure investment accelerates, and USDGO crosses US$1 billion in Stablecoin Weekly Pulse Vol. 18.

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

BlackRock's iShares Bitcoin Trust accounted for roughly 90% of a $225 million spot Bitcoin ETF outflow on July 23, raising questions about whether headline flow figures reflect sector sentiment or one fund's...

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

The CLARITY Act's removal from the Senate schedule with 72 hours before recess eliminates near-term procedural certainty, shifting analytical weight toward jurisdictions where licensing frameworks are already...

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

Recommended for you

More topics

More topics