Year-Turn Calm, Positioning Resets Ahead of January Liquidity

As crypto transitions from the final days of 2025 into the first trading week of 2026, the market moves out of pure holiday thinness and into a year-turn reset regime. Liquidity conditions are still constrained, but the character is changing: desks are reopening, books are being rebuilt, and positioning is starting to matter again — even if conviction remains limited.

This transition was briefly interrupted by a sharp liquidity impulse on December 29. More than US$80B in aggregate crypto market capitalization was added within roughly eight hours, pushing Bitcoin back above the US$90,000 level. The move was fast, headline-grabbing, and positioning-sensitive — occurring before full institutional participation had returned.

Importantly, the speed of the move says more about thin year-turn liquidity and positioning gaps than about a confirmed inflow regime. It highlights how fragile depth still is: when liquidity is light, relatively modest flow imbalances can translate into outsized price responses.

This week, therefore, is less about trend confirmation and more about re-anchoring exposure after volatility. Institutional participants are no longer in year-end preservation mode and capital is being selectively redeployed, hedges are being adjusted, and risk is being reintroduced cautiously as January liquidity gradually returns.

The result is a market that looks calmer after the initial spike — but is structurally more reactive underneath.

Key Market Review: Why Price Is Calmer — But More Reactive

Market Breadth — Narrow, Year-Turn Transitional, and Flow-Dependent

Source: Bitcoin and Ethereum ETF flows on Farside Investors via DeFiLlama (latest available data reflects late-December reporting, December 29, 2025.)

Market breadth this week remains selective rather than expansive, as we observed a record of $782 million outflow in Bitcoin ETFs in combined withdrawals during Christmas week, extending a six-day outflow streak as seasonal factors impacted institutional positioning. While the extreme holiday thinness of Christmas week has passed, liquidity depth is still rebuilding unevenly. Early-January price action is increasingly influenced by position re-establishment, not new capital inflows.

This matters because it reinforces the same regime signal we’ve been tracking: price can move sharply on thin liquidity and positioning resets (e.g., the Dec 29 market-cap impulse), but the durability of those moves still depends on whether ETF flows flip back to sustained inflows as January liquidity normalizes.

The most recent fully reported ETF data (late December) still shows:

BTC ETF flows: net negative on the margin

ETH ETF flows: mixed-to-soft, with no clear re-acceleration yet

This matters because early January often creates false directional signals — positioning shifts before real liquidity confirms them. Moves can look "clean," but lack durability without follow-through from flows.

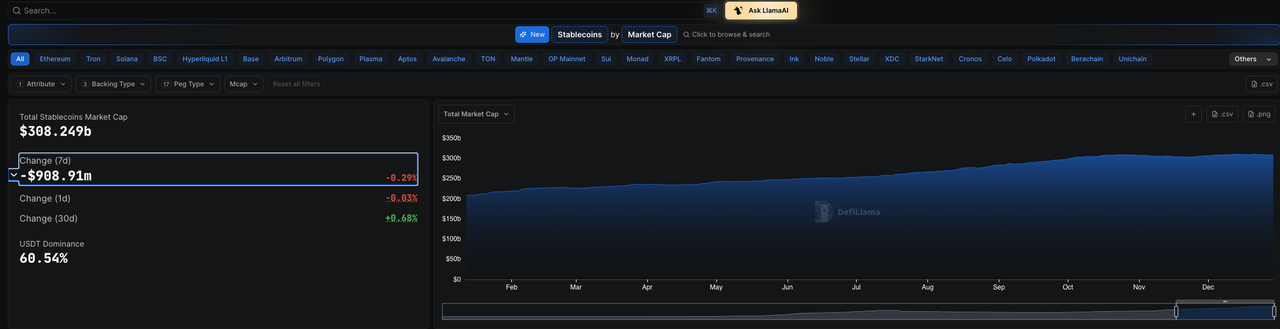

System Liquidity — Stablecoins Expanding Slowly, Distribution Still Concentrated

Source: Stablecoin flows and market cap via DeFiLlama

At the system level, stablecoin supply continues to creep higher, with total market capitalization holding just above ~US$310B. This confirms that liquidity is not contracting into year-end, but the pace of expansion remains too slow to fuel broad risk-on participation.

The more important signal remains distribution:

Ethereum continues to absorb incremental stablecoin growth, reinforcing its role as the primary liquidity rail.

Solana stablecoin balances remain below late-December highs, suggesting that last year's momentum-driven liquidity rotation has not yet resumed.

This configuration typically supports range-bound majors while keeping beta-heavy assets more sensitive to positioning swings.

ETF Flows — Stabilization Holds, January Confirmation Still Pending

Asset | Latest ETF Flow (Dec 26) | AUM | What Changed This Week (Liquidity + Positioning) |

|---|---|---|---|

Bitcoin (BTC) | -US$275.9M | ~US$92.86B | The latest print shows renewed net outflows into year-end, reinforcing that BTC's reclaim of 90k is primarily positioning- and liquidity-gap driven. BTC still behaves as the system's liquidity anchor, but ETF confirmation is required for sustained upside. |

Ethereum (ETH) | -US$38.7M | ~US$12.97B | ETH ETF flows remain mixed-to-soft, keeping ETH in a secondary beta role versus BTC. Liquidity preference continues to favor ETH on-chain, even as ETF participation lags. |

Solana (SOL) | N/A (on-chain proxy) | — | SOL remains more sensitive to stablecoin distribution and derivatives positioning. The absence of renewed stablecoin inflows keeps SOL beta fragile despite positive funding. |

ETF behavior continues to signal maintenance, not expansion, of institutional exposure. Until ETF flows flip decisively positive, large price moves (like Dec 29) should be treated as liquidity shocks rather than confirmed trend breaks.

Institutional Flows — From Year-End Defense to January Re-Engagement

From an institutional flow perspective, the message remains measured continuously:

The heavy ETF outflow phase earlier in December has not re-accelerated, but neither has it reversed

The latest Dec 26 prints confirm two-way, tactical flow behavior rather than conviction buying

ETF flows are no longer the dominant marginal driver during the year-turn window

This makes the Dec 29 market-cap expansion especially instructive: it demonstrates how price can travel faster than capital when liquidity is thin — a classic early-January microstructure feature.

Institutions have shifted from "reduce exposure" → "hold and recalibrate exposure."

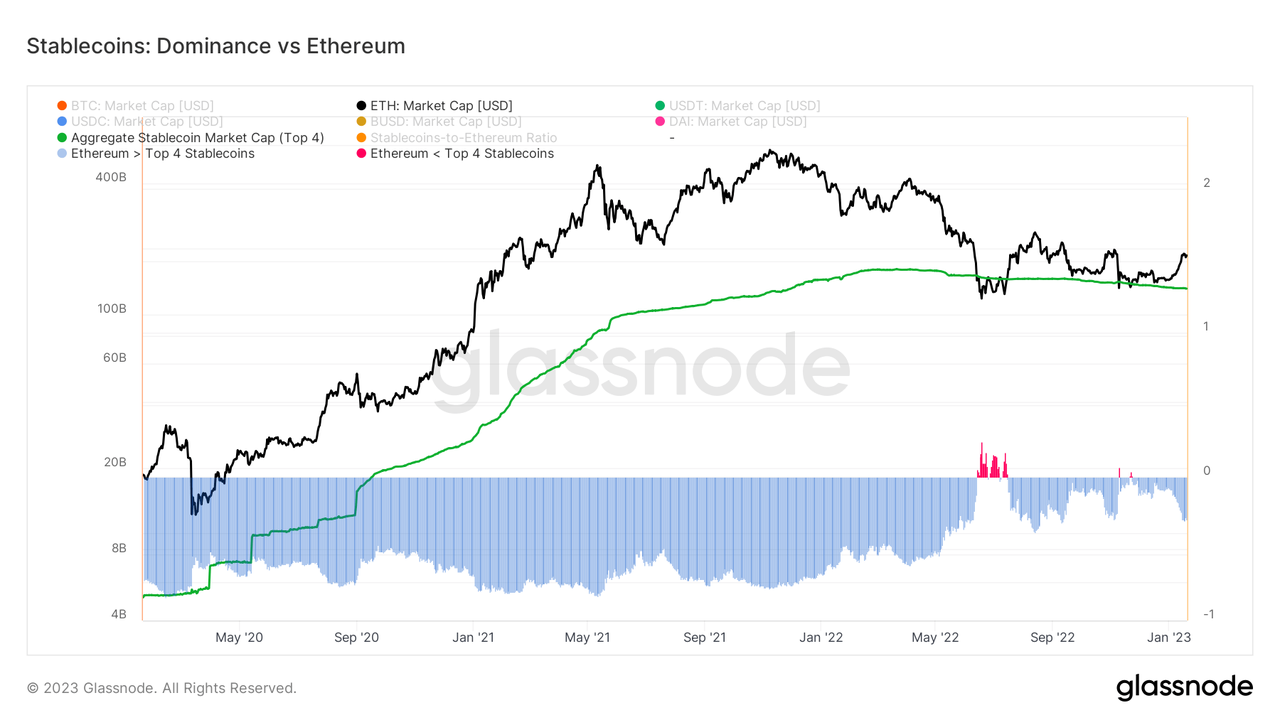

Global Stablecoins — Supply, Distribution & Liquidity Signal (Dec 29–Jan 4)

Source: https://studio.glassnode.com/charts/usd-eth-stable-dominance

Global stablecoin supply remains modestly expansionary, but the signal continues to point toward controlled liquidity rebuilding rather than reflation. Importantly, the Dec 29 market-cap surge was not accompanied by an immediate, broad-based jump in stablecoin issuance, reinforcing the view that the move was positioning- and liquidity-gap driven, not fueled by fresh system-wide capital.

Key observations into the year-turn:

The stablecoin issuance remains selective, consistent with desks reactivating capital rather than deploying new balance sheets. USDT dominance remains elevated, reinforcing a cash-management and settlement-first mindset. Chain-level divergence persists, with liquidity concentrating rather than dispersing.

Distribution snapshot (directional):

Ethereum: Stablecoin balances continue to trend higher, reinforcing ETH as the preferred settlement rail as liquidity returns cautiously

Solana: Still below recent highs, indicating that rotation appetite has not yet followed price back up after the Dec 29 impulse

Mid-tier L2s: Ongoing gradual drawdowns, consistent with capital consolidation toward depth and reliability

This configuration supports a regime where capital rotates within crypto rather than entering at scale — allowing for sharp price moves, but keeping breadth fragile and follow-through conditional until stablecoin growth broadens meaningfully.

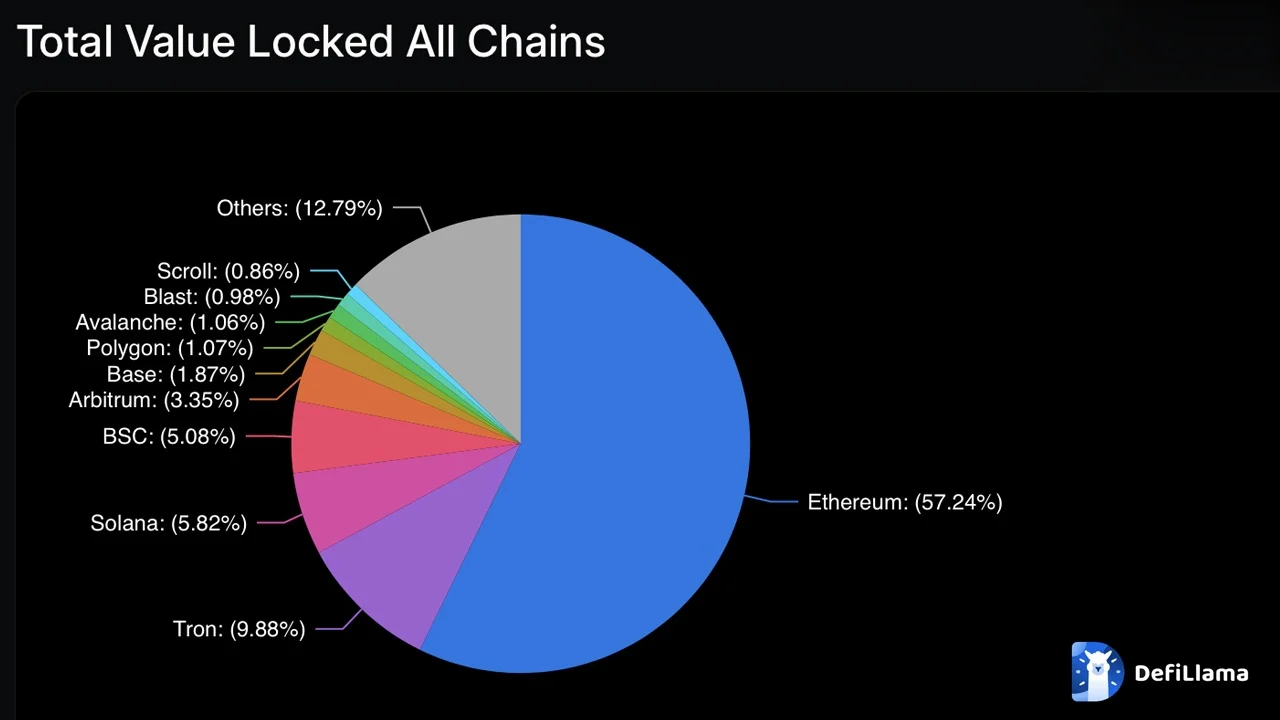

DeFi Overview — Capital Is Parking, Not Chasing (Year-Turn Regime on Dec 29 to Jan 4)

TVL: Holding Up, But Still Liquidity-Dependent

Headline DeFi TVL across core venues remains resilient, reflecting strong underlying infrastructure and price support, with Ethereum's DeFi TVL remains elevated while Solana and Base are stable, but lack clear signs of fresh liquidity acceleration.However, when paired with stablecoin distribution, TVL strength still appears valuation-supported rather than deposit-driven. This suggests stability via consolidation, not renewed risk-taking.

Activity Split Confirms the Regime

Ethereum DEX volumes: Stabilizing as liquidity re-concentrates on the deepest, most trusted rail.

Solana DEX volumes: Softer than mid-December, aligning with the absence of renewed stablecoin inflows despite higher spot prices.

Perpetuals: Active but selective — leverage is being deployed tactically, not aggressively.

Protocol Rotation: "Carry & Simplicity" Still Dominates

Internal composition continues to reflect a late-cycle / early-reset posture:

Lending & money markets: Liquidity remains sticky, but borrowing demand is muted.

Liquid staking: Steady participation due to native, low-complexity yield.

Complex structured strategies: Remain pressured in slow-growth liquidity environments, where carry costs matter and conviction is limited.

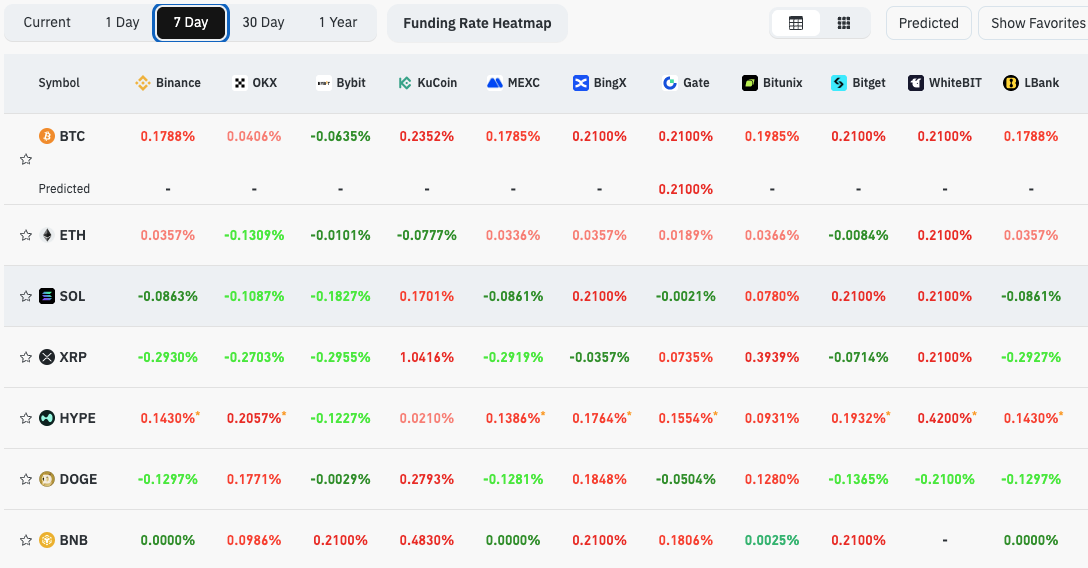

Funding & Positioning — Risk Appetite Exists, But Expression Is Controlled

Source: https://www.coinglass.com/AccumulatedFundingRate (The data is based on the last 7 days' funding rate taken snapshot on December 29, 2025)

Asset | Funding Character | Interpretation |

|---|---|---|

BTC | Mildly positive, low dispersion | Baseline long bias with disciplined leverage; BTC continues to act as the liquidity anchor |

ETH | Two-sided hedge pockets | Constructive but cautious beta expression; hedging demand remains visible |

SOL | Positive but fragmented | Risk-on expression, but more sensitive to reversals without stablecoin follow-through |

XRP | High dispersion | Positioning conflict dominates; range-bound behavior is more likely |

This pattern is typical of late December and early-January reset weeks where risk appetite is present, but conviction remains provisional, and positioning is still being recalibrated after year-end.

Outlook for the Week (Dec 29 – Jan 4): Reset First, Trend Later

Base case: Range and rotation. Liquidity is returning, but conviction isn't fully rebuilt yet.

Here's what to expect:

BTC leads, while altcoins follow selectively. The Dec 29 push back above $90k was positioning-driven; durability needs flow confirmation.

Without broader stablecoin distribution and positive ETF follow-through, rallies stay concentrated in majors.

Quick moves, limited follow-through. Rebuilding books means price reacts fast, but trends fade without confirmation.

Key watchpoints

January ETF prints: sustained inflows = confirmation; renewed outflows = fade risk.

Stablecoin breadth: expansion beyond core rails = risk-on; further concentration = "parking."

Funding dispersion: narrowing = healthier trend; widening = whipsaws.

This week is a rather crucial confirmation week with price sensitivity being relatively high, but a durable trend needs ETF and stablecoin follow-through.

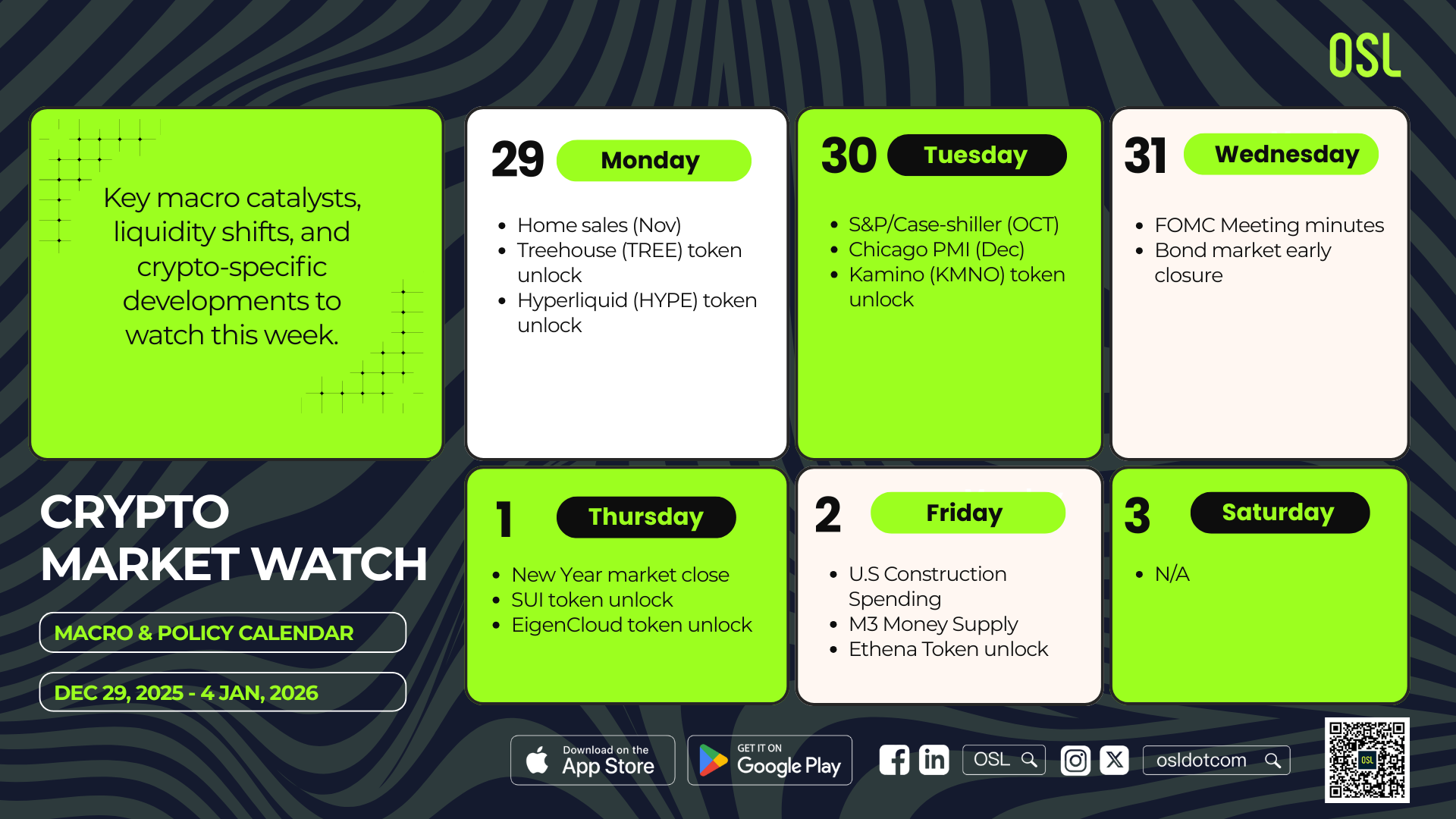

Crypto Market Watch: Key Events & Liquidity Drivers (Dec 29, 2025 – Jan 4, 2026)

Event Category | Region Focus | Why It Matters | Dates |

|---|---|---|---|

U.S. Housing / Demand Pulse | U.S. | Year-end housing/activity prints can nudge USD/rates expectations in thin liquidity, affecting crypto beta. | Dec 29: Pending Home Sales (Nov) |

U.S. Activity / Sentiment Cluster | U.S. | Macro “soft/hard data” helps shape early-January risk tone; surprises can spill into crypto in shallow depth. | Dec 30 S&P/Case-Shiller (Oct) Chicago PMI (Dec) |

Fed Signal (Policy Communication) | U.S. | FOMC Minutes can reprice front-end rates and volatility expectations—especially at year-turn when positioning is being rebuilt. | Dec 31: FOMC Meeting Minutes |

Market Structure: New Year’s Trading Hours | U.S. | Liquidity is the “event”: NYSE/Nasdaq closed Jan 1; rates/bond market early close on Dec 31 compresses hedging capacity. | Dec 31: Bond market closes early (2:00PM ET) Jan 1: New Year markets close |

First Full Trading Day After Holiday | U.S., EU | Jan 2 is the first full post-holiday session → better depth, clearer signals for whether Dec 29 impulse sustains. | Jan 2: U.S. Construction Spending (Nov) Jan 2: M3 Money Supply (YoY) |

Crypto-Specific Catalysts to Watch (Dec 29, 2025 – Jan 4, 2026)

Catalyst Type | Example Event | Why It Matters | Dates |

|---|---|---|---|

Token Unlocks & Supply Events | Treehouse (TREE): 11.25MM unlock (~5.45% of released supply) | Supply hitting the market during the year-turn can amplify spot swings + funding/basis dispersion. | Dec 29 |

Token Unlocks & Supply Events | Hyperliquid (HYPE): 9.92M unlock (reported) | Large unlock headlines can become a liquidity focal point; can widen perp basis and trigger rotation. | Dec 29 |

Token Unlocks & Supply Events | Kamino (KMNO): 229.17MM unlock (~5.35% of released supply) | Sizeable unlock → potential localized sell pressure and higher short-term volatility. | Dec 30 |

Token Unlocks & Supply Events | Sui (SUI): 43.69MM unlock (~1.17% of released supply) | Medium unlock; matters more if liquidity is thin or sentiment is fragile into Jan 1 closure. | Jan 1 |

Token Unlocks & Supply Events | EigenCloud: 36.82MM unlock (~9.74% of released supply) | Higher % unlocks can create sharper dislocations even if absolute value is smaller. | Jan 1 |

Token Unlocks & Supply Events | Ethena (ENA): 40.63MM unlock (~0.56% of released supply) | Smaller % unlock = usually modest impact, but can still drive short-term volatility in thin books. | Jan 2 |

bits.moreAboutTopics

bits.moreAboutTopics

bits.home.latest

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoins aren’t just an issuance game — the real battle is over infrastructure, channel capital, and users.

Stablecoin Weekly Pulse | Vol. 20: The Stablecoin Express: Next Stop, Card

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin activity cooled while firms kept investing. Vol. 19 examines regulation and enterprise demand across emerging-market payment corridors.

Stablecoin Weekly Pulse | Vol. 19: The Market Potential for Compliant, Enterprise-Grade Stablecoins

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

Stablecoin supply expands, payment infrastructure investment accelerates, and USDGO crosses US$1 billion in Stablecoin Weekly Pulse Vol. 18.

Stablecoin Weekly Pulse | Vol. 18: USDGO at US$1 Billion — The Story Behind

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

BlackRock's iShares Bitcoin Trust accounted for roughly 90% of a $225 million spot Bitcoin ETF outflow on July 23, raising questions about whether headline flow figures reflect sector sentiment or one fund's...

IBIT's $202M Exit Dwarfs ETF Field: Conviction or Rebalancing?

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

The CLARITY Act's removal from the Senate schedule with 72 hours before recess eliminates near-term procedural certainty, shifting analytical weight toward jurisdictions where licensing frameworks are already...

72 Hours to Recess: A Crypto Bill Vanishes From the Floor

bits.recommend.name

bits.moreAboutTopics

bits.moreAboutTopics