「Stablecoin & Payments Weekly Pulse」 Vol.8:On-chain Liquidity Recedes, Payment Infrastructure Accelerates

Master Global Key Changes in "Traditional Payment + Digital Asset Payment" in 10 Minutes

Reference Information and Professional Observations for Industry Participants

This Week's Theme: Stablecoin Supply Faces a "Hard Landing" — Why is Capital Fleeing While Giants Accelerate Construction Beneath the Panic?

Author: OSL Research Chief Analyst Eddie Xin Email: [email protected]

I. This Week's Stablecoin Payment Data

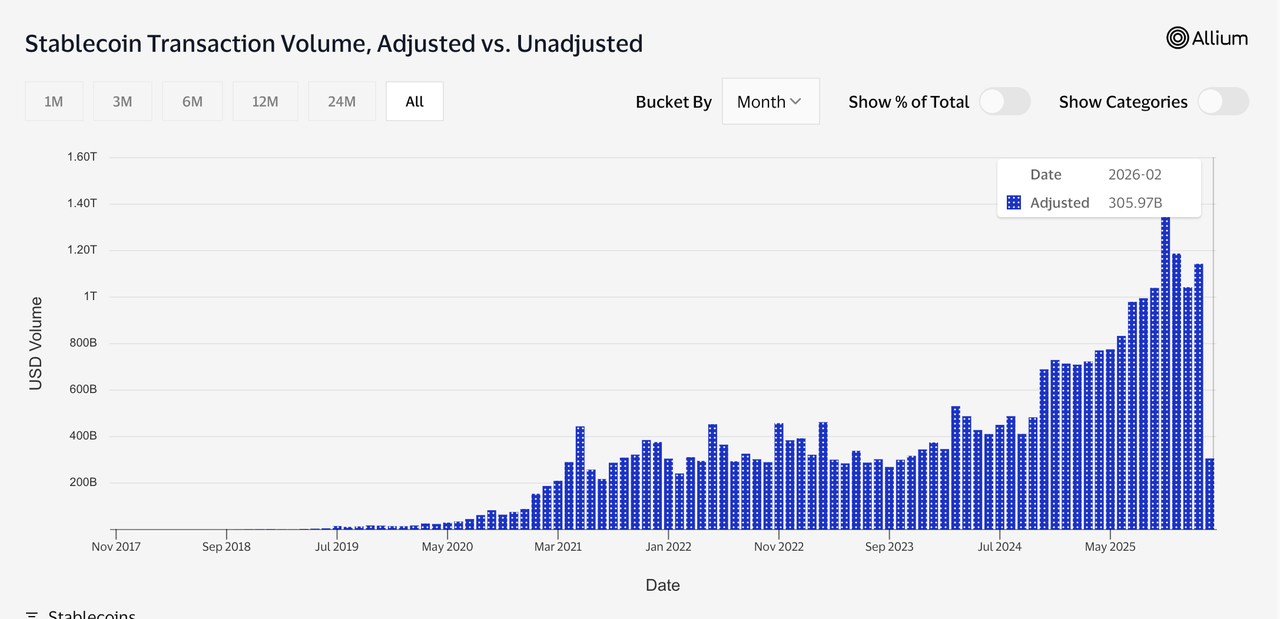

Market Cap Changes: As of February 6, 2026 (7-day rolling basis), the total market capitalization and weekly average supply of stablecoins stood at approximately $267.5 billion (Allium, Visa data), a decrease of about $40.7 billion from the weekly high of $308.2 billion, representing a drop of approximately -13.2%.

Transfer Volume: The total transfer volume over the last 7 days was in the $1.9 trillion range. However, looking at the structure after removing long-term noise, the OSL Research adjusted volume (excluding market making, self-trading, bots, etc.) is approximately in the $421.6 billion range.

Capital Flow: Overall, on-chain USD has decreased significantly over the past week, with redemptions exceeding new issuance. During periods of macroeconomic uncertainty or cooling risk appetite, capital tends to return to the banking system, seeking safer yield cushions like money market funds and short-duration US Treasuries. The overall capital preference is for holding fiat cash, while leverage and arbitrage are decelerating, leading to a phase of net redemption in stablecoin supply.

OSL Research Growth Observations

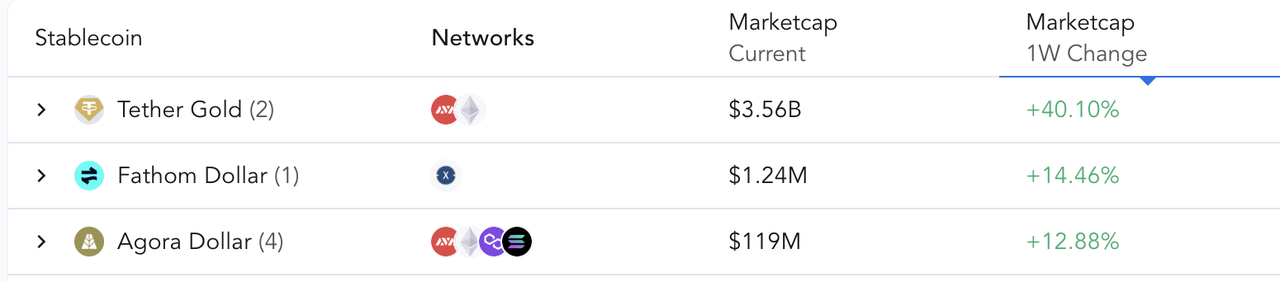

The top three stablecoins (protocols) by market cap growth this week are:

1. Tether Gold(XAU₮,+40.10%)

2. Fathom Dollar(FXD,+14.46% )

3. Agora Dollar(AUSD,+12.88%)

1. Tether Gold (XAU₮, +40.10% | $3.56B | ETH+AVAX)

This round looks more like a "concentrated jump in supply" rather than being driven by the gold price itself: Gold cannot contribute nearly 40% growth in a week. The significant upward shift in market cap aligns more with the characteristics of large-scale weekly issuance and the inclusion of cross-chain issuance volumes in statistics. Towards the end of the year, institutions prefer to turn "safe-haven assets" into settleable

2. Fathom Dollar (FXD, +14.46% | $1.24M | XDC)

Typical "Small Cap Percentage Magnification": With a base of only the million-dollar level, even a few new collateral mints or slight premiums/deviations in secondary market prices are enough to drive double-digit weekly gains. This type of growth resembles a phased fine-tuning of liquidity and supply; its sustainability needs to be judged against net minting and stability over the next two weeks.

3. Agora Dollar (AUSD, +12.88% | $119M | AVAX+ETH+Polygon+Solana)

Driven more by "Channel Distribution + Multi-chain Liquidity Completion": As AUSD covers multiple chains, volume usually stems from new trading pairs, liquidity pools, supplemental market-making depth, and fund consolidation and redistribution via cross-chain migration. A weekly rise of 13% looks less like pure price volatility and more like a fresh wave of capital being guided into usable settlement/collateral scenarios.

II. Weekly Stablecoin Payment & Infrastructure News

1. OSL Global Launches StableHub, Enabling 1:1 Exchange for Mainstream Stablecoins against USD

Source: OSL Group

Observation : The Asian stablecoin trading and payment platform, OSL Group, announced that its international trading platform, OSL Global, launched its stablecoin trading hub, StableHub, on February 6. It supports zero-slippage, 1:1 exchange between multiple mainstream stablecoins and the US Dollar.

The platform will roll out fee waivers and capital incentive programs; the initial phase features a partnership with Ripple offering up to 18% capital rewards for RLUSD. Jason Liu, Head of Global Exchange Business at OSL, stated that StableHub aims to provide one-stop, low-cost cross-stablecoin exchange and fiat on/off-ramp services, solving issues of complex exchange processes, high costs, and fragmented liquidity. The initial launch supports RLUSD, USDGO, USDC, and USDT, with more varieties to be added.

2. OKX Launches Mastercard Payment Card in Europe with Auto-Conversion for Stablecoin Settlement

Source: Yahoo Finance

Observation: This is essentially a defensive strategy for exchanges to prevent capital flight following the implementation of MiCA regulations. By "automatically converting" currency, the investment attributes of crypto assets are seamlessly transformed into consumption attributes, allowing users to cash out without enduring bank risk controls. OKX assumes the role of a compliant back-end exchange provider while utilizing Mastercard to solve acceptance issues. This "seamless front-end, compliant back-end" payment loop will significantly reduce users' willingness to move funds out of the OKX ecosystem, likely becoming standard for compliant European exchanges in 2026.

3. Coinbase Tests Enterprise Custom Stablecoin USDF: leveraging Custom Stablecoins capabilities, backed 1:1 by USDC

Source: Checkout.com Announcement

Observation: Coinbase is shifting its business focus from retail to enterprise-grade white-label services (SaaS). Large enterprises need their own branded settlement tools to ring-fence risks and reinforce branding but are unwilling to bear the compliance burden of being an issuer. USDF’s model—"wrapped in an enterprise shell, backed 1:1 by USDC at the bottom layer"—cleverly unifies liquidity pools at the infrastructure level while satisfying closed-loop settlement needs at the application level, further solidifying USDC’s status as the infrastructure for enterprise-grade "wholesale currency."

4. Fipto Becomes Europe's First "PI (Fiat) + MiCA CASP (Crypto)" Dual-Licensed Stablecoin Payment Institution

Source: Finextra (2026-01-30)

Observation: This is a vertical integration acquisition targeting MiCA provisions. As a payment gateway, Checkout.com was previously constrained by banking partners; acquiring an EMI license qualifies it to directly issue Euro stablecoins and process fiat settlements. This means it has completely eliminated reliance on third-party bank intermediaries, enabling it to offer e-commerce merchants a full-stack service of "stablecoin collection, direct fiat settlement," significantly reducing cross-border payment fees and time friction. It is a prime example of the "de-banking" trend among payment institutions.

III. Weekly Regulatory & Policy Signals

1. Tether Launches US-Compliant Stablecoin USA₮ (USAT), Issued via Anchorage Digital Bank

Source: Tether Announcement

Observation: This is Tether’s "borrowed boat" strategy to navigate the US regulatory siege. Facing an increasingly tightening blockade by the US government against offshore unregulated dollars, Tether cannot obtain a license directly. Instead, it issues USAT through Anchorage, an entity holding a federal banking charter, thereby establishing a firewall. The core logic is to retain the high-profit but regulatory-grey USDT to continue serving the global offshore market, while using the fully compliant USAT to penetrate US institutional clients prohibited from touching USDT, ensuring it is not completely ousted from the world's largest capital market.

2. Standard Chartered Warns: US Banking System May Face ~$500 Billion Deposit Diversion to Stablecoins by 2028

Source: Reuters (2026-01-27); CNA (2026-01-28)

Observation: This forecast confirms that stablecoins have evolved from "crypto trading chips" to direct competitors of commercial bank deposits. When on-chain T-bill-backed stablecoins can frictionlessly pass on 4-5% yields, while commercial banks—constrained by operating costs (branches, personnel)—can only offer minimal interest, the migration of corporate treasury funds is inevitable. This $500 billion-level liquidity extraction will force the banking system to either lobby regulators to increase capital requirements for stablecoin issuers (artificially leveling the spread) or be forced to shift from back-end infrastructure to front-end issuance, entering the "battle for deposit defense" themselves.

3. HKMA: First Batch of Stablecoin Issuer Licenses Targeted for March 2026; 36 Applications Received, Only a Few to be Approved Initially

Source: Reuters (2026-02-02)

Observation: The funnel effect of "36 applications, extremely few approvals" indicates the HKMA’s regulatory approach is "strict entry, risk control," rather than pursuing the appearance of market prosperity. This means regulators prefer to grant passes to the "regular army" with deep traditional finance backgrounds (e.g., banks, large payment institutions) rather than aggressive crypto-native startups. For most applicants, high compliance reserves will become sunk costs. The Hong Kong stablecoin market will present a highly concentrated oligopolistic structure from the start, competing not just on technology, but on who can sustain a long "war of attrition in regulatory approval."

4. Hong Kong "Stablecoin Ordinance" Regulatory Framework Landed and Entered Implementation Phase; Cross-Border Activities Still Anchored to Local Rules

Source: HKMA Press Release (Regulatory Regime Effective 2025-08-01)

Observation: As the ordinance enters the substantive execution phase, the biggest commercial challenge lies in the liquidity fragmentation caused by "regulatory sovereignty." Hong Kong explicitly anchors to local rules, meaning global stablecoins (like USDC) cannot simply introduce their global liquidity into Hong Kong but must establish entities in Hong Kong and meet independent capital adequacy requirements. While this builds a compliance moat, it also forces multinational payment companies to maintain separate "Hong Kong capital pools." This reduction in capital efficiency is the "toll fee" that must be paid for compliance. Future cross-border payments will rely more on back-end swaps between licensed institutions rather than single-currency global fungibility.

IV. Observation: Macro Divergence between Liquidity "Hard Landing" and Infrastructure Fever

Author: Eddie Xin, Chief Analyst at OSL Research ([email protected])

This week's market performance was enough to confuse, if not unsettle, most observers.

We witnessed a typical macro divergence: data on the screen was flashing warnings—stablecoin supply dropped precipitously by $40 billion, crashing secondary market prices and making liquidity look precarious. Yet, off-screen, Fidelity, Tether, and OSL were doing the exact opposite; everyone is accelerating capital expenditure on infrastructure. This contradiction of "capital flight vs. infrastructure fever" is not a signal of industry recession, but a profound liquidity switch. Simply put, we are experiencing the growing pains of transitioning from "leverage-driven" to "compliance-driven."

To understand this missing $40 billion, we must look beyond panic and reconstruct the logic behind it.

For the past two years, a major pillar supporting stablecoin scale was actually "basis arbitrage" funds reliant on high volatility in the crypto market—using stablecoins as margin to earn risk-free funding rates on-chain. But this week's events show that as market efficiency improves and volatility converges, risk-adjusted returns from on-chain arbitrage can no longer outperform traditional risk-free rates—or rather, they break even while carrying risk.

Consequently, we saw algorithm-driven "mechanical unwinding": to close trades, institutions had to sell BTC (held as spot chips) and simultaneously redeem stablecoins, flowing back into the higher-trust traditional fiat system.

The collapse of this micro-mechanism is forcing the entire market to re-examine the value of "shadow dollars." For a long time, offshore stablecoins played the role of "privatized liquidity injection," but in the current macro environment, capital preferences have undergone a qualitative change. Standard Chartered’s warning of a $500 billion "deposit diversion" is essentially capital voting: funds are no longer satisfied holding grey offshore currencies and are moving toward assets with higher security and stronger compliance. It can be said that the scale of traditional offshore stablecoins has hit a utility ceiling, and the market is undergoing a brutal "re-pricing of credibility."

Understanding this explains why compliant institutions are expanding against the trend. They are competing for the "settlement standard" of the next generation of digital dollars. The game is no longer about the shrinking speculative market of today, but the incremental market of the future. When funds withdraw from the chain due to risk concerns, whoever provides a bank-grade compliant safe harbor—and a secure pipeline for future trillion-level RWA (Real World Asset) settlement—seizes the critical direction of industry development.

Therefore, regarding the current liquidity "dry spell," we need not be overly pessimistic. With the complete withdrawal of basis arbitrage capital, the market will likely undergo a period of low-volatility adjustment, but this is precisely the process of clearing out bubbles. The old speculative paradigm is disintegrating, and future incremental funds will not be hot money seeking high leverage, but allocation capital seeking efficient settlement. All of this is waiting for the new infrastructure to be laid down.

Disclaimer and Disclosure

1. Nature of Document This document (the "Document") has been prepared by OSL internal personnel for informational purposes only and does not constitute investment, legal, tax, or any other professional advice, nor should it be relied upon as such. No part of this Document may be reproduced, distributed, or transmitted to any third party in any form without the prior written permission of OSL. This Document does not constitute an offer, solicitation, marketing material, product disclosure statement, or legal document, nor does it form the basis of any binding contract or commitment. This Document is intended solely to present OSL's observations and strategic insights into the industry and does not represent the official position, strategy, or decisions of OSL. The authors are not independent research analysts, and this Document does not constitute "investment research" as defined by applicable laws or regulations. Consequently, this Document has not been prepared in accordance with regulations designed to ensure the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

2. No Reliance The information, opinions, and analyses contained in this Document are based on public information and OSL's internal judgment, without regard to the personal objectives, financial situation, or needs of any recipient. This Document does not constitute a personal recommendation, nor does it constitute an invitation or solicitation to buy, sell, or engage in any financial instrument, product, or service. Recipients should consult their own independent advisors regarding their personal circumstances, objectives, experience, and financial resources before making any investment or other decision. All investments involve risk; values may fluctuate, and investors may recover less than the original investment amount. Past performance is not indicative of future results.

3. Accuracy, Completeness, and Limitations This Document has been prepared based on information OSL believes to be reliable, but OSL has not independently verified its accuracy, completeness, or fairness. Although reasonable care has been taken to ensure the content is not false or misleading, OSL makes no express or implied warranty as to the accuracy, completeness, fairness, or reasonableness of the content. OSL accepts no liability for any errors, omissions, or consequences of reliance caused by third-party information cited in the Document. The performance of any instruments, entities, or strategies mentioned may be significantly affected by market, regulatory, technical, or other factors.

4. Forward-Looking Statements This Document may contain forward-looking statements involving known and unknown risks, uncertainties, and other factors. Actual results, performance, or achievements may differ materially from those expressed or implied by such statements. OSL is under no obligation to update, revise, or withdraw any forward-looking statements.

5. Disclosure of Conflicts of Interest OSL, its affiliates, and employees may hold positions in or participate in transactions related to the assets or entities mentioned in this Document. The authors or related personnel may receive compensation related to OSL's business performance in this regard. OSL has implemented policies and procedures to identify and manage potential conflicts of interest.

6. Intellectual Property and Restrictions on Use This Document is protected by copyright and is for the internal use of the designated recipient only. Recipients may store, display, analyze, modify, reformat, and print this Document for internal purposes, but without OSL's prior written consent, may not:

Resell, redistribute, or use this Document commercially;

Reverse engineer, extract, or create derivative works, including for training or application in machine learning/artificial intelligence systems;

Publish or transmit this Document to third parties.

7. Limitation of Liability To the maximum extent permitted by applicable law, OSL and its affiliates, officers, employees, and agents shall not be liable for any direct, indirect, incidental, consequential, or special damages arising out of or in connection with the use, reliance, or interpretation of this Document, including but not limited to:

Loss of profits;

Business interruption;

Data corruption or loss;

Reputational damage.

8. Global Distribution Note Recipients should ensure compliance with applicable local laws. Distribution of this Document may be restricted in certain jurisdictions. Recipients must ensure this Document is not distributed to any person or entity prohibited by law from receiving it.

More topics

More topics

Latest

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

Explore if stablecoins can lower global remittance costs (currently 6%) and their role in solving financial exclusion in orphaned corridors.

Global Remittance Costs at 6%, Africa at 8%: Can Stablecoins Truly Reduce Costs? BIS Offers a Cautious Response

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

Discover how stablecoins restructure B2B payments, reduce costs by 70%, and solve the $27T trapped liquidity issue in the SWIFT network.

SWIFT Doesn't Actually Move Your Money: How Stablecoins Rebuild B2B Payments

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

Explore the three stages of stablecoin evolution: from exchange trading chips and DeFi liquidity to becoming global compliant payment infrastructure.

From Crypto Chips to Global Money Rails: How Stablecoins Grew Up

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Discover how stablecoins address trapped cash, FX risk, and visibility gaps in corporate treasury through quiet pilots and institutional adoption.

The CFO's Three Problems: How Stablecoins Are Quietly Entering Corporate Treasury

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Discover the significance of Bitcoin's 200-week SMA, historical returns, and how to use technical indicators for long-term crypto investing.

Why is Bitcoin Frequently Mentioned Near the "200-Week Moving Average"? Understanding This Long-Term Indicator

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Analyze Bitcoin market structure using on-chain data. Learn why the recent sell-off's realized loss is half of the previous round.

Is This Panic Selling Only Half as Intense as Before? Analyzing Bitcoin Market Structure via On-chain Data

Recommended for you

More topics

More topics