Why Does Settlement Take So Long?

You send money on Friday, they receive it on Tuesday. What happens in between?

When you transfer $100,000 via a banking app and see the "Transfer Successful" notification, you assume the money has arrived. It hasn’t. That money has merely begun a long, arduous journey—passing through layered legacy systems, hitting weekend closures, crossing time zones, and sitting in compliance queues before it finally "lands." This isn't a technical glitch. It is a feature of traditional financial infrastructure that was born with a "business hours" genetic code. Stablecoins are rewriting that DNA.

The Structural Slowness of Traditional Finance: A Losing Race Against Time

In an era of globalization and the digital economy, business demands have shifted from "Same Day" to "Second-Level Availability." Yet, the settlement speed of the traditional banking system remains stuck in the last century.

While a delay of a few days for a cross-border payment might seem like a minor inconvenience, it creates significant friction: disrupted supply chains, increased interest costs, currency exchange risk exposure, and reduced competitiveness.

This delay is not due to operational errors; it is rooted in four systemic constraints of traditional infrastructure:

Business-Day-Only Core Banking Systems

The vast majority of the world's banks operate on Core Banking Systems designed around the "working day." They typically process full functions only during local legal working hours (e.g., Monday–Friday, 9:00–17:00).

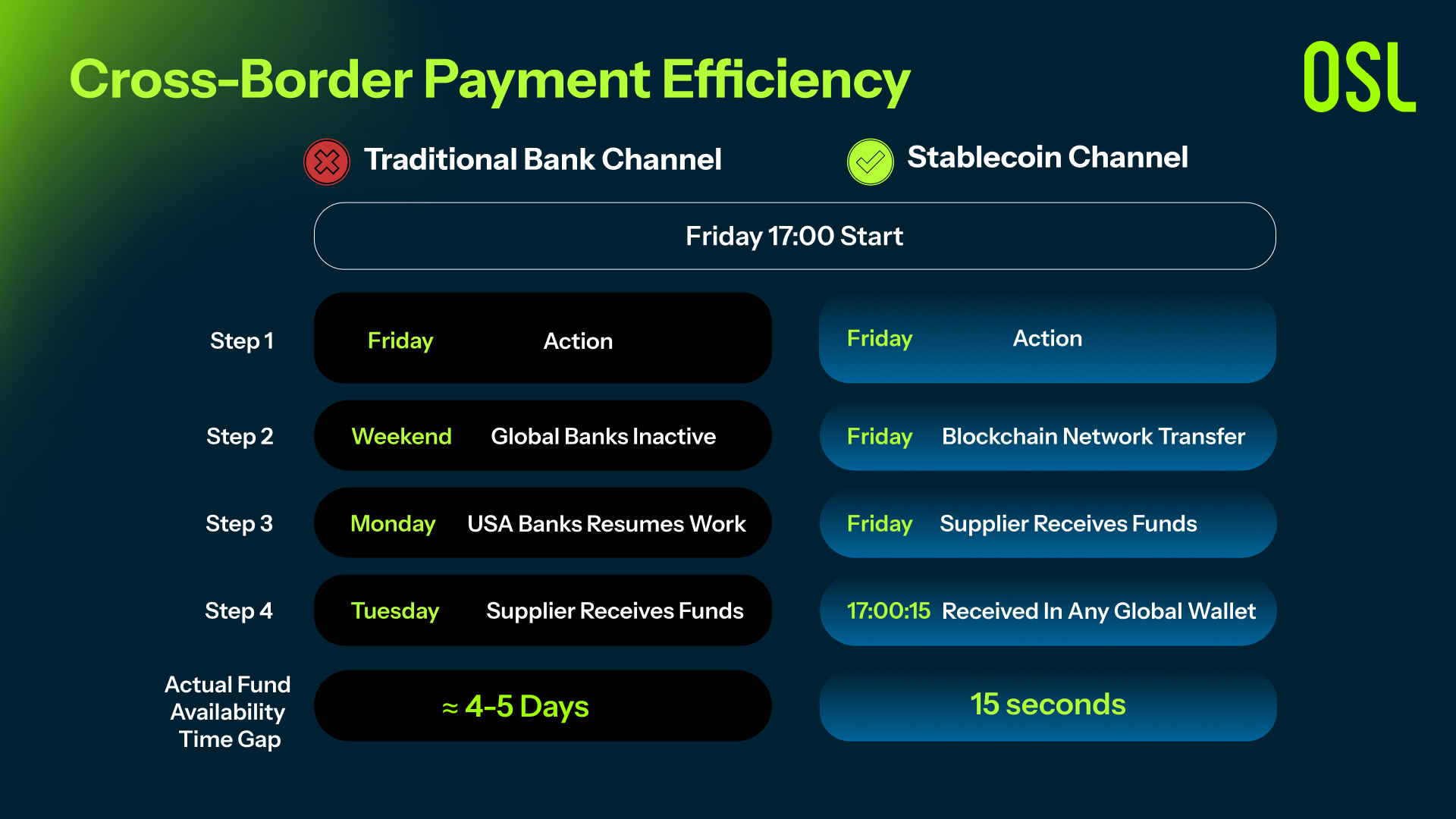

The Result: Any payment instruction issued after the cut-off time on Friday is automatically suspended until the next business day (usually Monday). This creates a recurring "dead zone" of 52–65 hours every week where capital is immobile.

Time-Zone Cascading Delays

The global financial system spans 24 time zones, but major settlement centers (London, New York, Hong Kong, Tokyo) have misaligned operating hours.

The Scenario: A Chinese company initiates a USD payment to a US supplier at 17:00 Beijing time on Friday. In New York, it is 04:00 AM on Thursday—too early for processing. By the time US banks open, the funds may miss the daily cut-off or hit the weekend. A standard B2B payment is thus systemically stretched to 4–5 calendar days.

Batch Netting & Delayed Settlement

Traditional banks rely on Batch Processing and Netting rather than real-time settlement. Payment instructions are collected throughout the day, netted against each other, and executed in a specific clearing window at night or the next day.

The Constraint: While domestic payments may achieve T+0, cross-border payments typically lag at T+1 to T+5. This mechanism, designed in the 1970s to save on computing and telecom costs, is fundamentally incompatible with the 24/7 demands of the modern digital economy.

Manual Compliance & Off-Hour Gaps

Large, cross-border, or flagged transactions often trigger AML (Anti-Money Laundering) or KYC (Know Your Customer) alerts, requiring manual review.

The Bottleneck: During weekends and holidays, financial institutions maintain minimal staffing. Flagged transactions sit in a queue until human compliance officers return on the next business day, adding unpredictable delays to the settlement timeline.

The Stablecoin Advantage: From "Wait a Week" to "Settled in Seconds"

Enter Stablecoins—cryptocurrencies pegged to stable assets like the US Dollar (e.g., USDC or USDT). Unlike volatile crypto assets, they maintain a 1:1 value ratio, making them ideal for payments. Built on blockchain technology, they bypass legacy obstacles entirely:

True 24×7×365 Availability

Blockchain-based distributed ledger networks operate without business hours, unaffected by statutory holidays, weekends, or regional working calendars. The system remains fully functional and online 24 hours a day, 365 days a year. Whether a payment instruction is issued at 23:59 on a Friday or at 00:01 on New Year’s Day, it can be received and executed immediately, with final settlement achieved in no more than a few seconds.

Real-Time Gross Settlement (RTGS)

Unlike the netting and batch processing mechanisms of traditional financial systems, stablecoin transactions adopt a real-time gross settlement approach for each individual transaction. Every transaction achieves irreversible finality within seconds to tens of seconds after being generated. There is no need to wait for overnight batch processing windows or next-day clearing cycles, completely eliminating delays such as T+1 or T+2.

Time-Zone Agnostic Instantaneity

The blockchain ledger serves as a single, globally shared data layer, where transaction confirmation time is independent of the geographic locations of the sender, receiver, or intermediaries. Whether the payer is in Beijing and the recipient is in New York or Dubai, all relevant parties can observe the change in fund status simultaneously at the moment of block confirmation (typically within a <1 second difference). This fully eliminates cross-time-zone waiting due to scenarios such as "the recipient's bank is closed."

Programmable & Automated Compliance

Compliance rules can be pre-embedded into the transaction process in the form of code via smart contracts, enabling fully automated execution throughout the entire process, including but not limited to:

Automatic interception of blacklisted or sanctioned addresses in real time

Automatic freezing or reporting of transactions exceeding regulatory thresholds

Automatic attachment and on-chain recording of information required for taxation and anti-money laundering purposes

Regulators and auditors can access real-time, immutable, and complete data through nodes or authorized interfaces, eliminating the need to rely on financial institutions to manually submit reports during business hours. This significantly enhances regulatory efficiency and transparency.

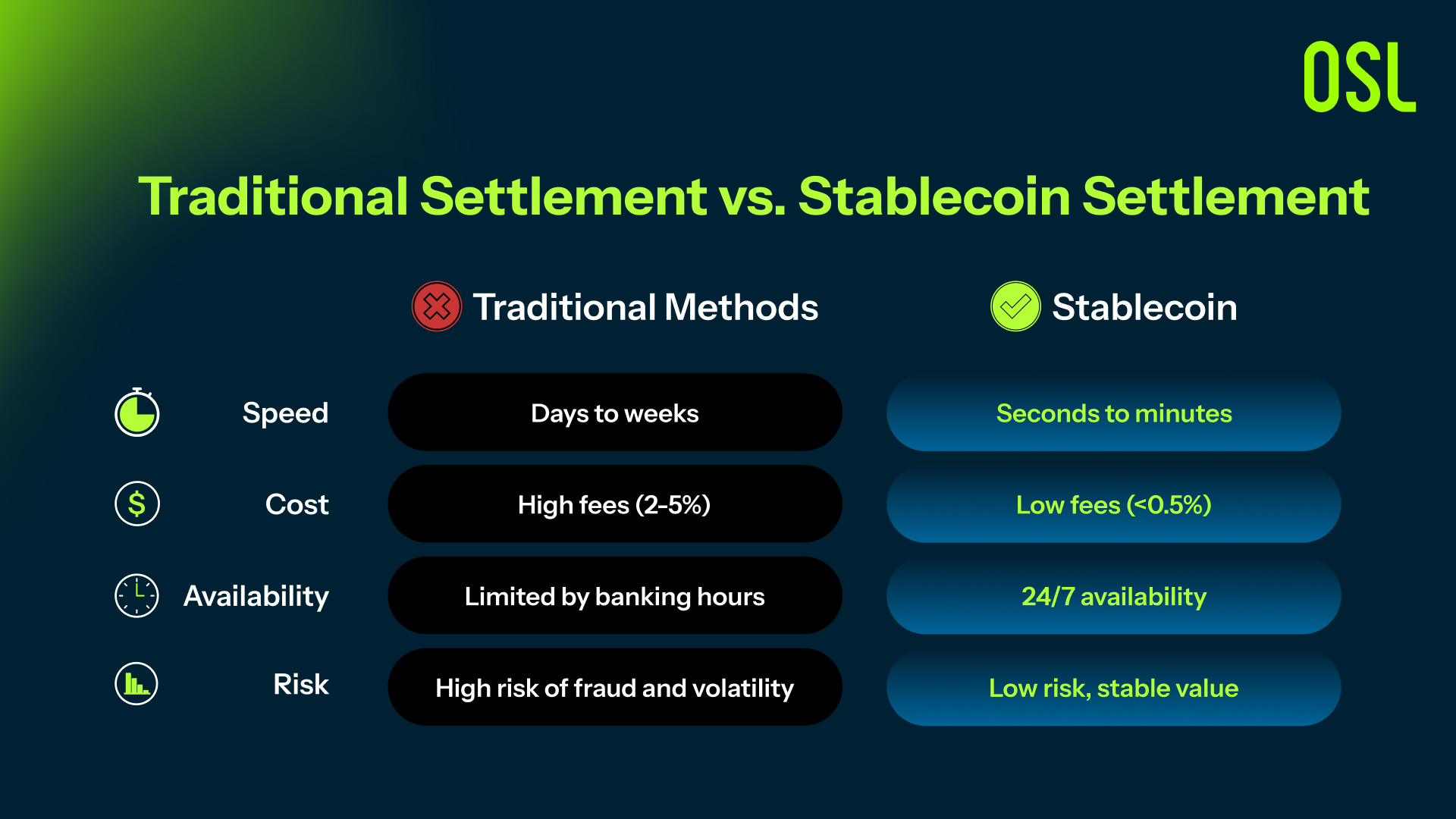

Traditional Settlement vs. Stablecoin Settlement: A Difference of Dimensional Magnitude

When we compare the traditional financial system with blockchain-based settlement using stablecoins, we aren’t looking at a marginal improvement—something that’s “a little faster, a little cheaper.” Instead, what emerges is a structural disruption that feels almost like a dimensional shift: Quantitative Differences:

Speed: Traditional: 4–5 days; Stablecoin: Seconds to minutes.

Cost: Traditional: 2–5% in fees; Stablecoin: Typically below 0.5%.

Availability: Traditional: Business hours only; Stablecoin: 24/7/365.

Risk: Traditional: Higher exposure to delays and errors; Stablecoin: Reduced through smart contracts, albeit with crypto-specific risks such as volatility in non-stable assets.

Traditional finance sells a “funds-moving service” that only operates on weekdays.

Stablecoins sell the actual funds themselves—funds that can move at any given second.

The true disruptive power of stablecoins doesn’t lie solely in the technical detail of “pegging to the US dollar.” It lies in liberating the availability of funds from the “weekday system” and aligning it with “physical time.”

It doesn’t repair the old world—it builds a new one. A world without business hours, without borders, without batches, and without manual waiting.

For global enterprises, this means cash flow can now move at the same speed as information flow—in seconds, even milliseconds.This isn’t the future of payments.

This is the present—it’s just that the traditional system hasn’t fully caught up yet.