The Invisible Tax: Deconstructing the Payment Stack

You swipe for $10,000. The merchant gets $9,700. Where did the $300 go?

When you tap your card to buy a $5 coffee, the experience feels effortless — a quick beep, a confirmation on the terminal, and the transaction disappears into the background. But behind that frictionless moment sits a 50-year-old architecture made of legacy rails, multiple intermediaries, and an invisible layer of fees most businesses never fully understand.

This is the world of traditional payments — and it’s also why stablecoins are starting to reshape how money moves globally.

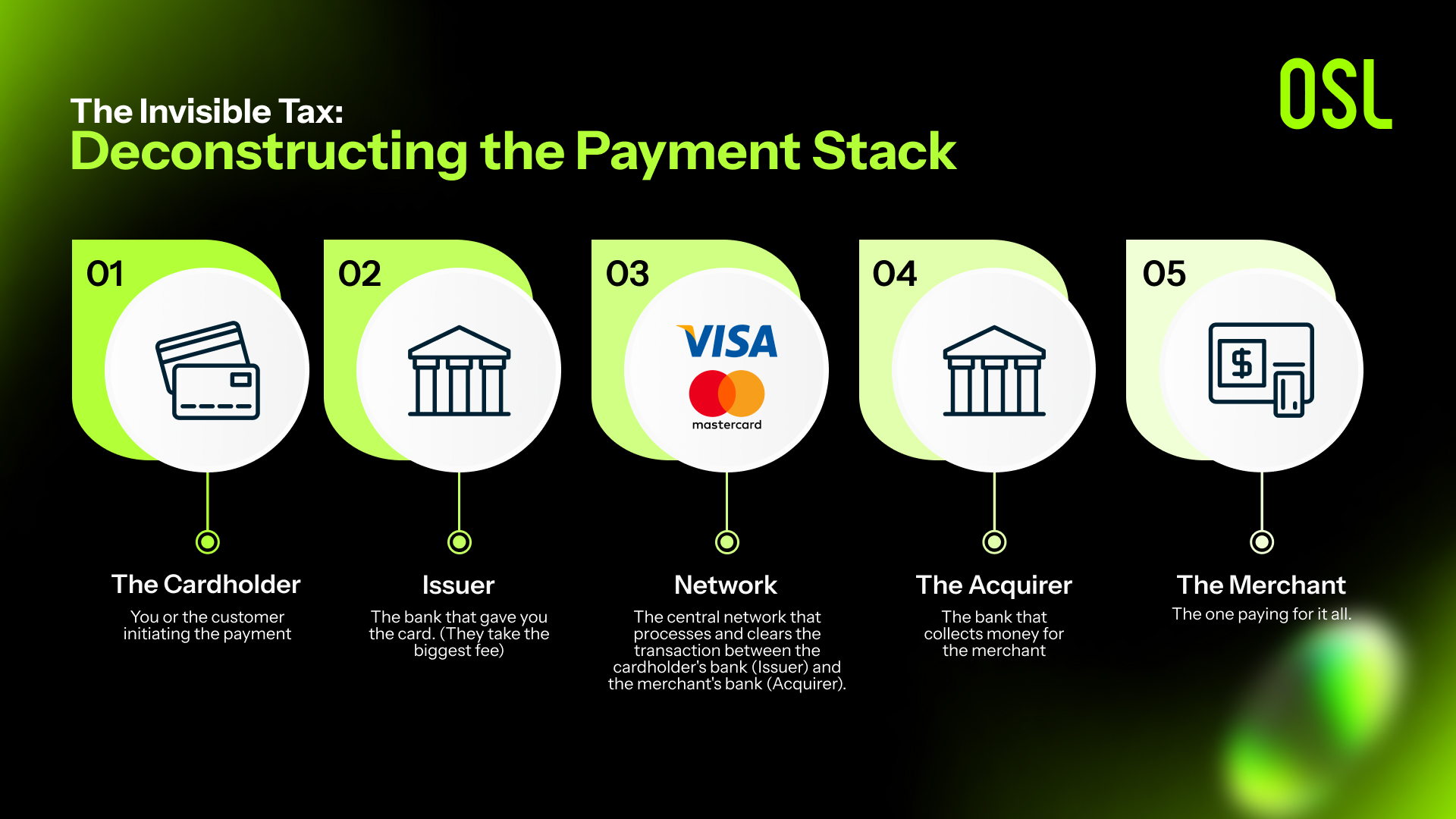

The Hidden Machinery: The Four Corners Model

The backbone of card payments today is the Four Corners Model, a structure designed in the 1970s but still powering trillions of dollars of commerce.

Think of a payment not as a digital message, but as a physical package. Before it reaches its destination, it must pass through four distinct hands:

The Cardholder (You) — the customer initiating the payment

The Issuer (Your Bank) — the bank that issued the card

The Acquirer (The Merchant's Bank) — the bank that processes payments for the merchant

The Merchant (The Shop) — the business selling the goods

Every hand introduces friction. Every hand takes a fee.

This explains a simple but surprising truth: When you spend $10,000, the merchant often receives only $9,700.

Where Did the $300 Go? The Invisible Tax You Never See

Those missing dollars don’t disappear; they’re distributed along the payment chain. But the distribution is far from even.

Interchange (≈1.5%–2.5%) — The Silent Giant

The largest portion goes to the Issuing Bank.

Not the payment processor. Not Visa. Not Mastercard.

Why does the issuer take the biggest slice?

They assume credit risk when they lend you money

They fund your “free” airline miles and cashback

In reality, nearly 2% of every 3% fee funds reward programs for consumers — paid by the merchant.

Scheme Fees (≈0.1%–0.15%) — The Rail Toll

Visa and Mastercard do not issue cards.

They operate the rails.

Every transaction that crosses their network pays a small toll.

Acquirer Fees & Processor Markup (≈0.5%–1%)

This covers:

Payment gateway technology

Fraud screening

Chargeback handling

Security and compliance

All together, this forms the invisible 3% tax embedded into modern commerce.

Cross-Border Payments: A System Torn Between Geography and Legacy

Swipe payments look instant, but cross-border settlements tell the real story.

Sending money internationally today is like sending a parcel through multiple postal services:

Your bank may not connect directly with the overseas bank

Each “hop” requires a correspondent bank

Each correspondent adds time, cost, and risk of failure

This is why cross-border transfers:

Take 2–5 working days

Pause on weekends and holidays

Fail due to compliance mismatches and cut-off times

Cost a multiple of domestic fees

The problem isn’t the money itself. The problem is the infrastructure built for a slower, pre-digital world.

Stablecoins: Not a New Currency — A New Architecture

Stablecoins solve a structural problem, not a monetary one.

Instead of the Four Corners model, stablecoins operate on a Two-Corner or Three-Corner system:

Traditional (4 hops)

Sender → Sender Bank → Network → Receiver Bank → Receiver

Stablecoin Settlement (1–2 hops)

Sender Wallet → (optional payment gateway) → Receiver Wallet

This changes everything.

1. Cost drops

No issuer → no interchange → no rewards funding → no 3% drag Settlement costs fall from 3% → <1%

2. Speed increases

No banking hours

No weekend downtime

No SWIFT queues

No correspondent chain

Global settlement becomes near-instant.

3. Transparency improves

Every hop is visible.

Every movement is traceable.

Compliance becomes programmable.

Stablecoins do not compete with money. They compete with the rails money travels on.

The Key Takeaway: Payments Don’t Need New Money — They Need New Infrastructure

For decades, businesses paid the price for the inefficiencies of the Four Corners system — higher fees, slower settlements, and opaque cross-border processes.

Stablecoins challenge this not by being “crypto,” but by offering a more direct, internet-native architecture for moving value.

The comparison is simple:

Traditional payments: a toll road with four checkpoints

Stablecoins: a direct flight

As global businesses demand faster settlement, lower fees, and real-time treasury visibility, the architecture of money movement is being rewritten — not by banks, card networks, or fintech intermediaries, but by open, programmable, borderless digital rails.

The future of payments is not a debate between crypto and fiat. It is a debate between old infrastructure and new infrastructure.